{kind=link}

Pound was knocked down after another data miss. Headline CPI slowed for the third month in a row to 2.4% yoy in April, down from 2.5% yoy and missed expectation of 2.5% yoy. Core CPI also slowed to 2.1% yoy, down from 2.3% yoy and missed expectation of 2.2.% yoy.

The Office of National Statistics noted that air fares made the largest downward contribution to the change in CPI. It noted that “the timing of Easter in the middle of April 2017 contributed to air fares rising by 18.6% on the month whereas this year, Easter fell at the beginning of April before the price collection period and there was no price rise. Instead, fares fell slightly, by 0.2%, between March and April.

Poor weather was blamed for weak Q1 GDP. Timing of Easter is now blamed for CPI slowdown. But whether they’re true or now, the chance of an August BoE hike looks slimmer after the release.

Also from UK, RPI accelerated to 3.4% yoy in April, up from 3.3% yoy, met expectation. PPI input rose to 5.3% Yoy, PPI output was unchanged at 2.7% yoy, PPI output core slowed to 2.4% Yoy. House price index was unchanged at 4.2% yoy in March.

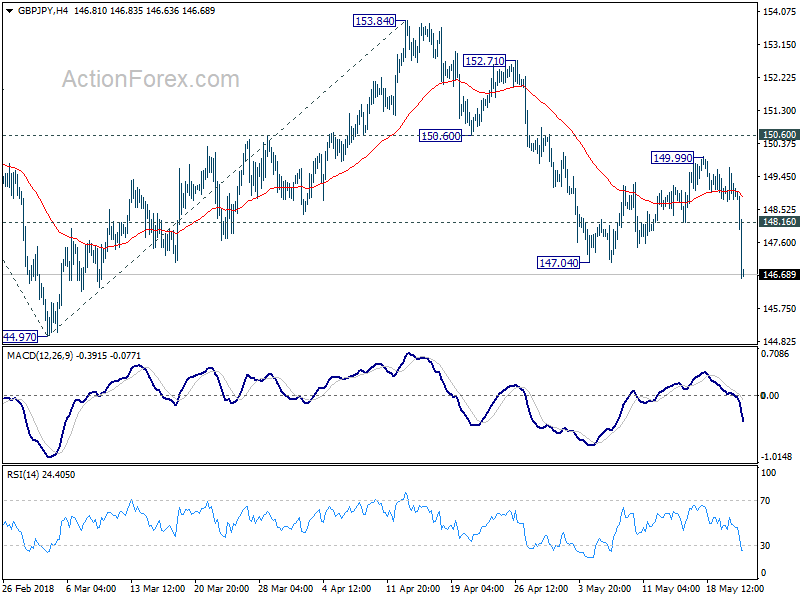

GBP/JPY responds to the release by diving through 147.04 support, confirming resumption of recent decline from 153.84. 144.97 is the next target.

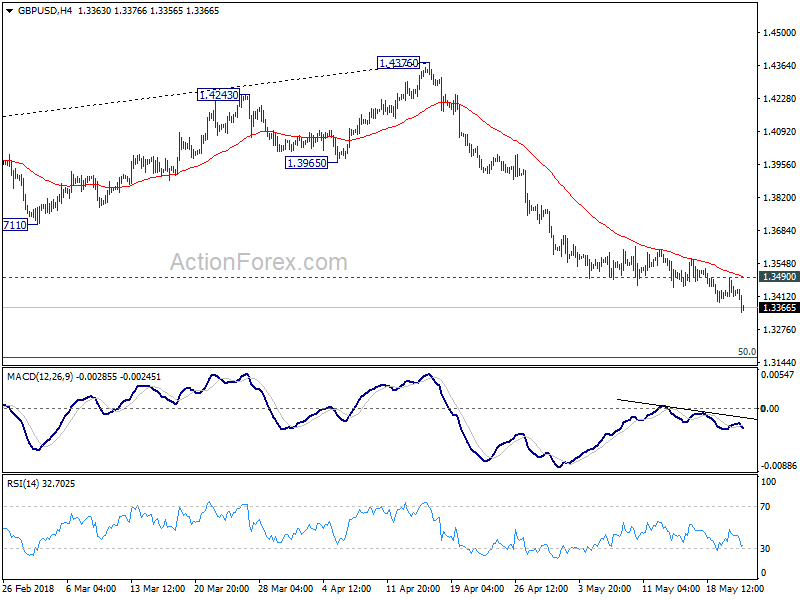

GBP/USD drops to further to 1.3345 and is on course for 1.3161 fibonacci level.

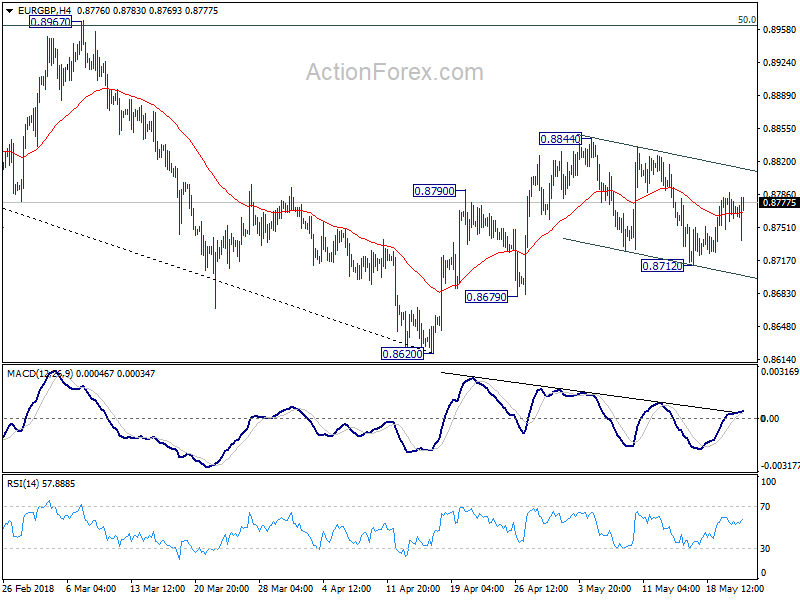

EUR/GBP is stay in range, because Euro is weighed down by its own weaker than expected PMI data.