{kind=link}

BoE stands pat as widely expected. And just as we anticipated, Ian McCafferty and Michael Saunders come back with votes for rate hike. This feels like the irresistable nature of hawks.

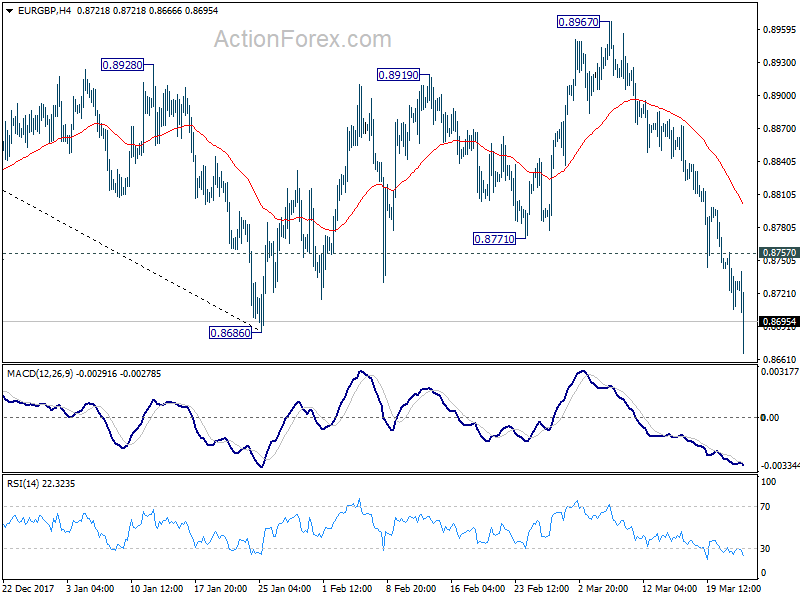

Sterling spikes higher broadly after the release. And EUR/GBP dives through key support level at 0.8686 to as low as 0.8666. Now, let’s see if it can sustain below this key support level.

Below is BoE’s full statement.

Below is BoE’s full statement.

Bank Rate Maintained at 0.50%

Our Monetary Policy Committee has voted by a majority of 7-2 to maintain Bank Rate at 0.50%. The committee also voted unanimously to maintain the stock of corporate bond purchases and UK government bond purchases.

The Bank of England’s Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 21 March 2018, the MPC voted by a majority of 7-2 to maintain Bank Rate at 0.5%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee also voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion.

In the MPC’s most recent projections, set out in the February Inflation Report, GDP was expected to grow by around 1¾% per year on average over the forecast period. While modest by historical standards, that growth rate was expected to exceed the diminished rate of supply growth of the economy, which was projected to be around 1½% per year. As a result, a small margin of excess demand was projected to emerge by early 2020 and build thereafter. That pushed up on domestic costs, although CPI inflation fell back gradually as the effects of sterling’s past depreciation faded. Inflation remained above the 2% target in the second and third years of the MPC’s central projection.

Recent data releases are broadly consistent with the MPC’s view of the medium-term outlook as set out in the February Report. The prospects for global GDP growth remain strong, and financial conditions continue to be accommodative, with little persistent effect from the recent financial market volatility. UK GDP growth in the fourth quarter was revised down slightly, to 0.4%, with the composition of demand implying less rotation towards net trade and business investment than anticipated at the time of the February Report. However, early estimates of the expenditure components of GDP are prone to revision, and other indicators of exports and investment point to a stronger picture. The latest activity indicators suggest that the underlying pace of GDP growth in the first quarter of 2018 remains similar to that in the final quarter of 2017.

CPI inflation fell from 3.0% in January to 2.7% in February. Inflation is expected to ease further in the short term although to remain above the 2% target. Pay growth continued to pick up. The unemployment rate remained low in the three months to January. The firming of shorter-term measures of wage growth in recent quarters and a range of survey indicators suggest pay growth will rise further in response to the tightening labour market. This provides increasing confidence that growth in wages and unit labour costs will pick up to target-consistent rates.

Developments regarding the United Kingdom’s withdrawal from the European Union – and in particular the reaction of households, businesses and asset prices to them – remain the most significant influence on, and source of uncertainty about, the economic outlook. In such exceptional circumstances, the MPC’s remit specifies that the Committee must balance any significant trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity. The steady absorption of slack has reduced the degree to which it is appropriate for the MPC to accommodate an extended period of inflation above the target.

As in February, the best collective judgement of the MPC remains that, given the prospect of excess demand over the forecast period, an ongoing tightening of monetary policy over the forecast period will be appropriate to return inflation sustainably to its target at a more conventional horizon. All members agree that any future increases in Bank Rate are likely to be at a gradual pace and to a limited extent. In light of these considerations, seven members thought that the current policy stance remained appropriate to balance the demands of the MPC’s remit.