{kind=link}

Pound dips mildly after disappoint inflation data but loss is limited. In particular, headline CPI slowed to 2.7% yoy in February, down from 3.0% yoy and missed expectation of 2.8% yoy. The reading doesn’t give any added pressure for BoE to rate interest rate in May. Nonetheless, CPI stays above the mid-point of 2-3% target range. BoE board members should still view the Brexit transition deal as a relief to businesses. And investments could come back with, at least, part of the uncertainties cleared. Know hawks like Michael Saunders and Ian McCafferty could still start pushing for rate hike during this week’s meeting. Hence, there is no sustainable selloff in the pound, just mild retreat.

Here is the list of inflation data:

- CPI Feb: 0.4% mom vs exp 0.5% mom vs prior -0.5% mom

- CPI Feb: 2.7% yoy vs exp 2.8% yoy vsprior 3.0% yoy

- CPI Core Feb: 2.4% yoy vs exp 2.5% yoy vs prior 2.7% yoy

- RPI Feb: 0.8% mom vs exp 0.8% mom vs prior -0.8% mom

- PPI Input Feb: -1.1% mom vs exp -0.9% vs prior 0.7% mom

- PPI Input Feb: 3.4% yoy vs exp 3.8% yoy vs prior 4.7% yoy

- PPI Output Feb: 0.0% mom vs exp 0.1% mom vs prior 0.1% mom

- PPI Output Feb: 2.6% yoy vs exp 2.7% yoy vs prior 2.8% yoy

- PPI Output Core Feb: 0.2% mom vs exp 0.2% mom vs prior 0.3% mom

- PPI Output Core Feb: 2.4% vs exp 2.4% yoy vs prior 2.2% yoy

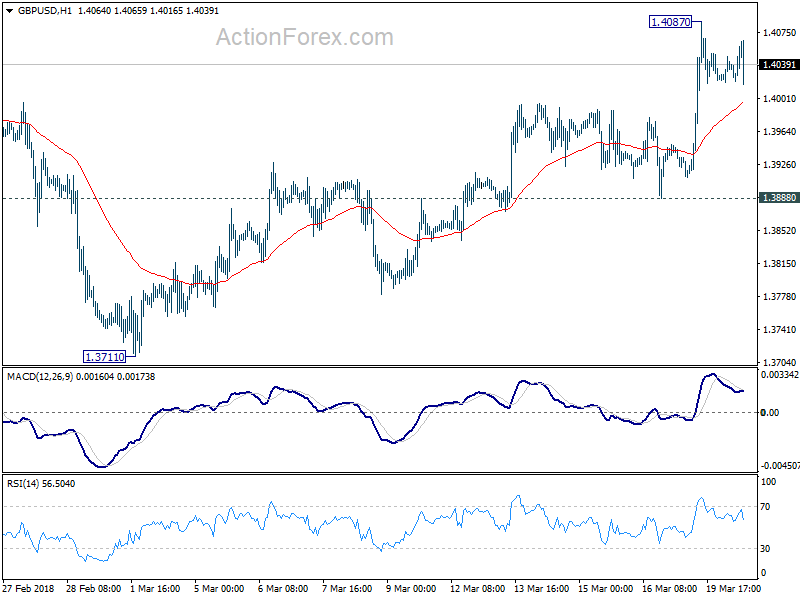

GBP/USD is staying comfortably above 55H EMA despite the post CPI dip. Recent rise is still on course through 1.4087 to 1.4144 resistance.