{kind=link}

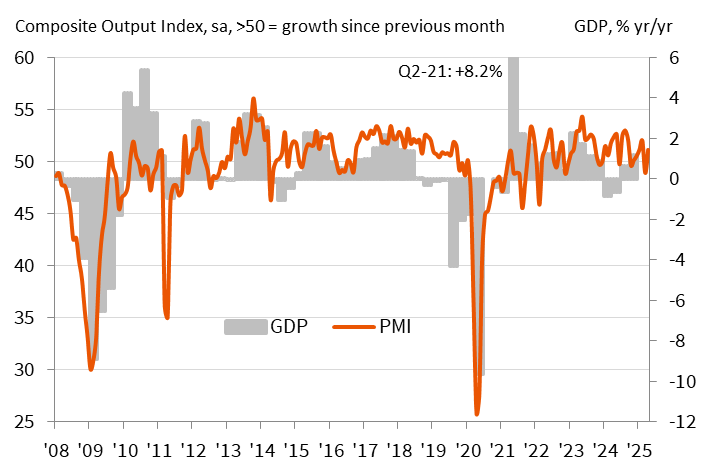

Japan’s flash PMI data for April signaled a return to growth in the private sector, with Composite PMI rising from 48.9 to 51.1. The recovery was driven primarily by a rebound in the services sector, where activity rose to 52.2 from 50.0. Meanwhile, manufacturing remained in contraction, though the pace of decline eased slightly, with the PMI inching up from 48.4 to 48.5.

According to S&P Global’s Annabel Fiddes, the divergence between sectors reflected subdued factory output versus strengthening service demand.

A closer look at new business trends revealed further divergence. Manufacturers reported the sharpest drop in new orders in over a year, driven by falling foreign demand and persistent concerns over tariffs and client spending. In contrast, service providers saw their strongest rise in new work since January.

Still, inflationary pressures were strong across the board, with input costs rising at the fastest pace in two years, prompting firms to pass on those costs to customers via higher selling prices.

Overall optimism for output over the next year fell to its lowest level since August 2020, during the early phase of the COVID-19 crisis.