{kind=link}

Today’s US non-farm payrolls report comes as the markets are already reeling from this week’s tariff shock. With consensus expecting a 128k rise in jobs for March and the unemployment rate holding steady at 4.1%, the print itself may not do much to lift sentiment or Dollar, even if it exceeds expectations.

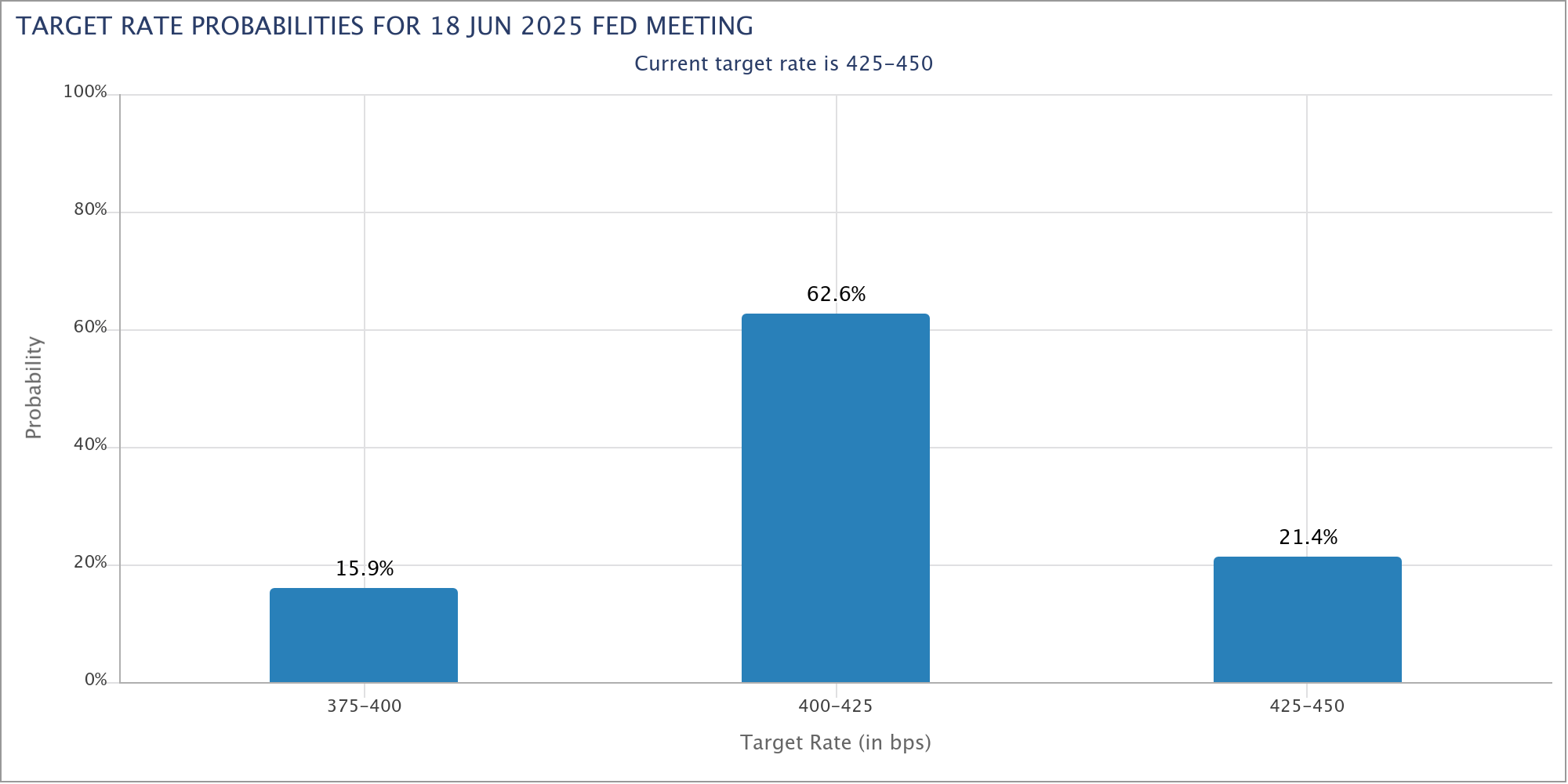

On the other hand, a downside surprise could further shift the odds in favor of a Fed rate cut in Q2. Currently, fed funds futures suggest nearly an 80% probability of a 25bps reduction in June.

While Fed has signaled patience, deteriorating jobs data may leave policymakers with little choice but to move sooner rather than later. Such development would in turn apply further pressure on Dollar.

Recent data paints a murky picture: the employment components in both ISM manufacturing (44.7) and services (46.2) surveys fell deep into contraction in March. ADP report came in at a modest 155k growth.

Whether today’s NFP captures the full extent of that weakness as indicated by ISM data remains to be seen, but the underlying trend is clearly deteriorating.