{kind=link}

Two major central banks will announce their monetary policy decisions today, with SNB leading, followed by BoE.

SNB is widely expected to lower its policy rate by 25bps to 0.25%. With inflation at just 0.3% in February, well below the mid-point of target range, there is both room and necessity for further easing to keep medium-term inflation expectations anchored closer to 1%.

However, the urgency for additional policy support appears to be diminishing, especially with growing optimism around Eurozone economy. Stronger Eurozone growth, driven by major fiscal expansion plans, is expected to lift Euro and boost demand for Swiss exports, which could help mitigate recession and deflation risks in Switzerland.

A Reuters poll of economists showed that most expect rates to remain at 0.25% by year-end, while 10 foresee a move to 0%, and only three expect SNB to maintain the current 0.50% level.

Meanwhile, BoE is widely expected to hold its Bank Rate steady at 4.5%, with little change to its cautious forward guidance. A Reuters poll of 61 economists showed unanimous expectations for a rate hold today, with the next cuts projected for May, August, and November.

The key focus for markets will be whether any additional Monetary Policy Committee members join Catherine Mann and Swati Dhingra in voting for an immediate rate cut, which could signal a shift toward a more dovish stance in the coming months.

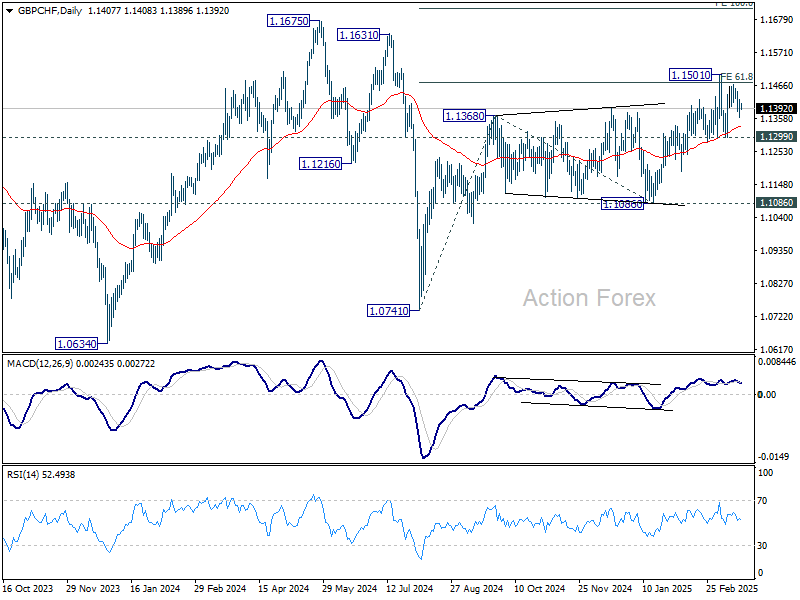

Technically, while GBP/CHF extended the rally from 1.1086, it has clearly struggled to find convincing momentum. It’s plausible that this rise is the third leg of the corrective rebound from 1.0741, which has already completed after meeting 61.8% projection of 1.0741 to 1.1368 from 1.1086 at 11437. Break of 1.1299 support will solidify this bearish case and bring deeper fall back to 1.1086 support. Nevertheless firm break of 1.1501 will pave the way to 1.1675 resistance next.