{kind=link}

Risk sentiment showed signs of stabilization in the US overnight, with S&P 500 and NASDAQ posting gains. However, stocks are merely digesting recent steep losses rather than having a decisive turnaround.

The reaction to lower-than-expected US consumer inflation data was relatively muted. The market’s cautious interpretation of the data is justified, as the latest CPI figures do not yet capture the full effects of tariff-related price pressures. There is still a lack clarity on how inflation will evolve under the new tariff regime, particularly when reciprocal tariffs come into play on April 2. Nevertheless, for the moment at least, disinflationary momentum is leaning in the Fed’s favor.

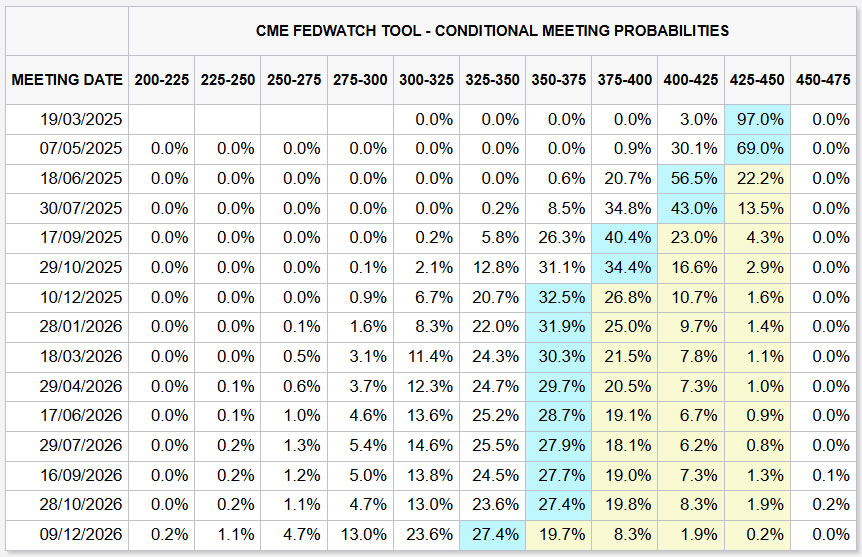

Interestingly, market pricing has shifted the expected timing of Fed’s next rate cut back from May to June. Futures now show just 31% probability of a 25bps cut in May, while the odds for a June cut have climbed to 78%.

Traders appear to believe Fed will need additional time to assess the economic impact of tariffs before making a policy move. From a timing perspective, June would align better with Fed’s next round of economic projections, allowing policymakers to incorporate more data into their decision-making.

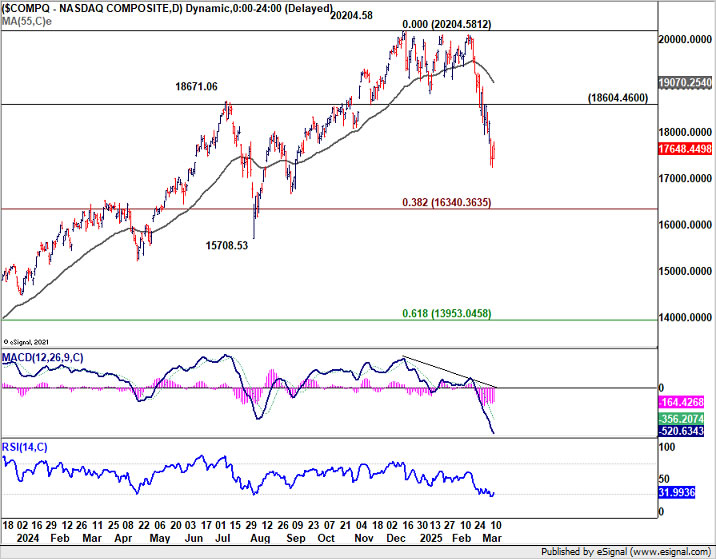

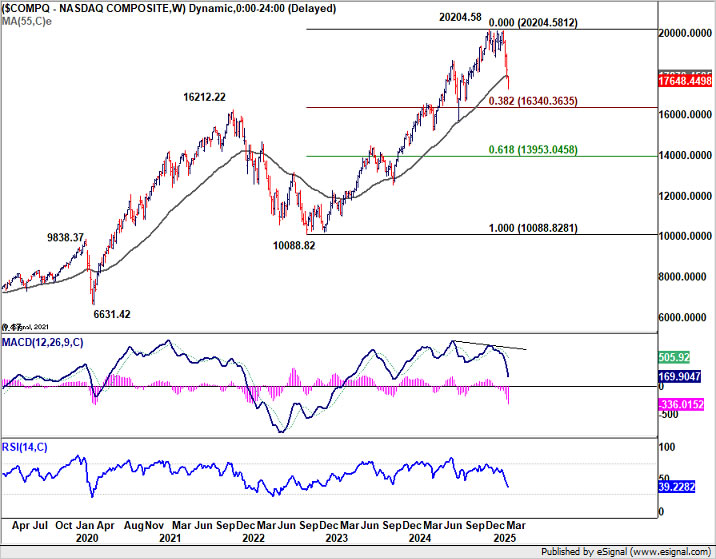

As for NASDAQ, oversold condition as seen in D RSI could start to slow downside momentum, and some near term consolidations cannot be ruled out. But risk will stay on the downside as long as 18604.46 resistance holds. Fall from 20204.58 is seen as a correction to the whole up trend from 10088.82 (2022 low) at least. It should extend to 38.2% retracement of 10088.82 to 20204.58 at 16340.36 before bottoming.