{kind=link}

BoC is widely anticipated to lower its overnight rate by another 50bps at today’s meeting, reducing the policy rate to 3.25%. This follows a similar move in October, aimed at addressing a cooling economy where inflation has been at or below 2% for three months already, and core measures remain slightly above target. Last week’s data showing unemployment rate jumping to 6.8% from 6.5% solidified expectations of a significant rate reduction.

A recent Reuters poll highlighted this expectation, with 21 of 27 respondents predicting a 50bps cut and the remainder forecasting a more modest 25bps reduction. The primary argument for aggressive easing centers on the need to return interest rates to a neutral range, estimated between 2.25% and 3.25%. Following today’s expected cut, rates would align with the upper bound of neutral, still potentially exerting a mildly restrictive effect on the economy.

However, there is an opposing view that recent resilience in consumer spending, inflation, and labor market data could justify a slower pace of easing. This argument suggests that BoC could take a more measured approach, affording time to assess the economy’s response to October’s 50bps cut before making further moves.

Regardless, the debate now shifts to determining the eventual terminal rate, with clarity likely, hopefully, to emerge only in January’s Monetary Policy Report.

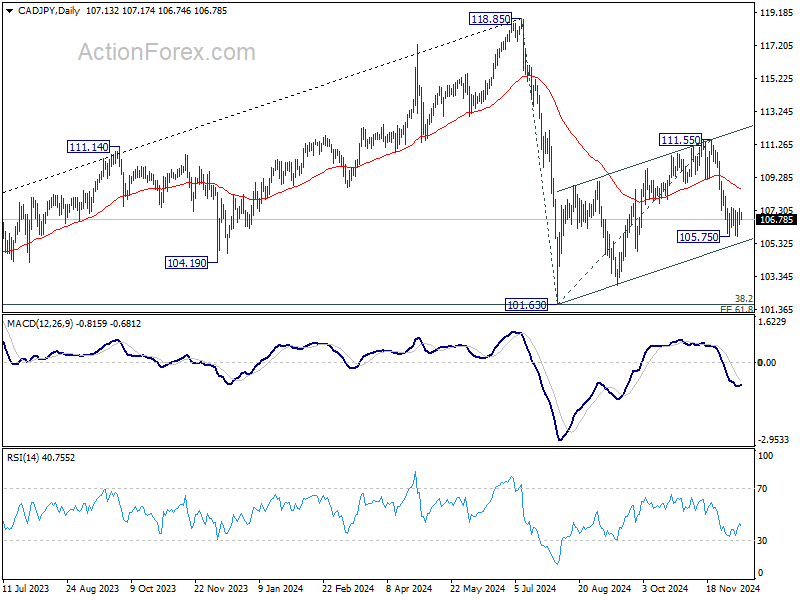

Technically, similar to other Yen crosses, CAD/JPY’s corrective rebound from 101.63 should have completed with three waves up to 111.55. Further decline is expected as long as 55 D EMA (now at 108.65) holds. Break of last week’s low at 105.75 will resume the fall from 111.55 towards 101.63 low, and possibly through it to resume the larger decline from 118.85. However, the speed of the decline could more hinge on the development in Yen than Loonie.