{kind=link}

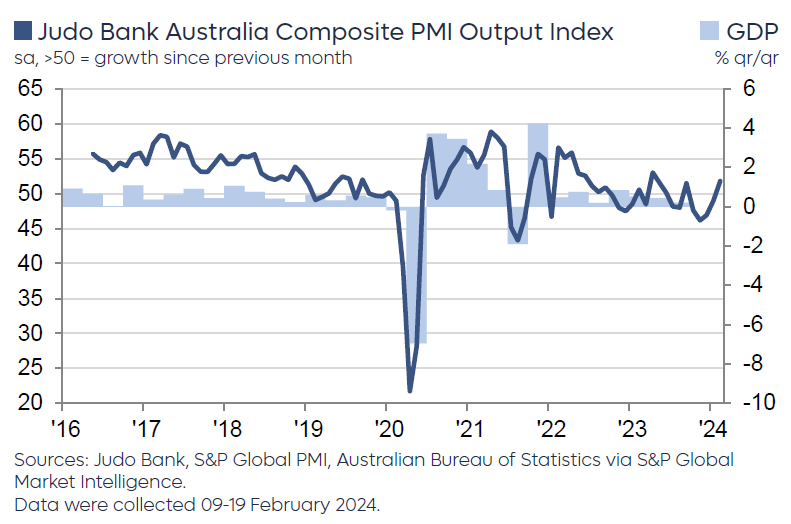

Australia’s PMI Manufacturing fell sharply from 50.1 to 47.7 in February, with Manufacturing Output marking a 45-month low at 45.0. In stark contrast, PMI Services surged to a 10-month high of 52.8, propelling Composite PMI to 51.8, the first time it has breached the 50-mark threshold since last June.

Warren Hogan, Chief Economic Advisor at Judo Bank, said the PMI results “weaken the case for monetary policy easing any time soon”. Improvement in activity indicators and modest rise in price indexes suggest that “risks to monetary policy remain even balanced”.

Hogan’s analysis also points to an economy that is gaining momentum, expanding at more vigorous pace in 2024 compared to the latter half of 2023. He posits that continuous improvements could herald stronger economic growth this year than the last, hinting that “soft landing is behind us”.

Furthermore, Composite Employment Index reached its highest level since last September, indicating “rising labour demand and employment growth” in the overall economy. This is accompanied by intensifying price pressures, with Composite Output Price Index’s climb to its highest point since last September 2023, indicating that domestic inflation could be hovering between 4% and 5%. Hogan cautions that the recent trend of disinflation “may well have run its course.”