{kind=link}

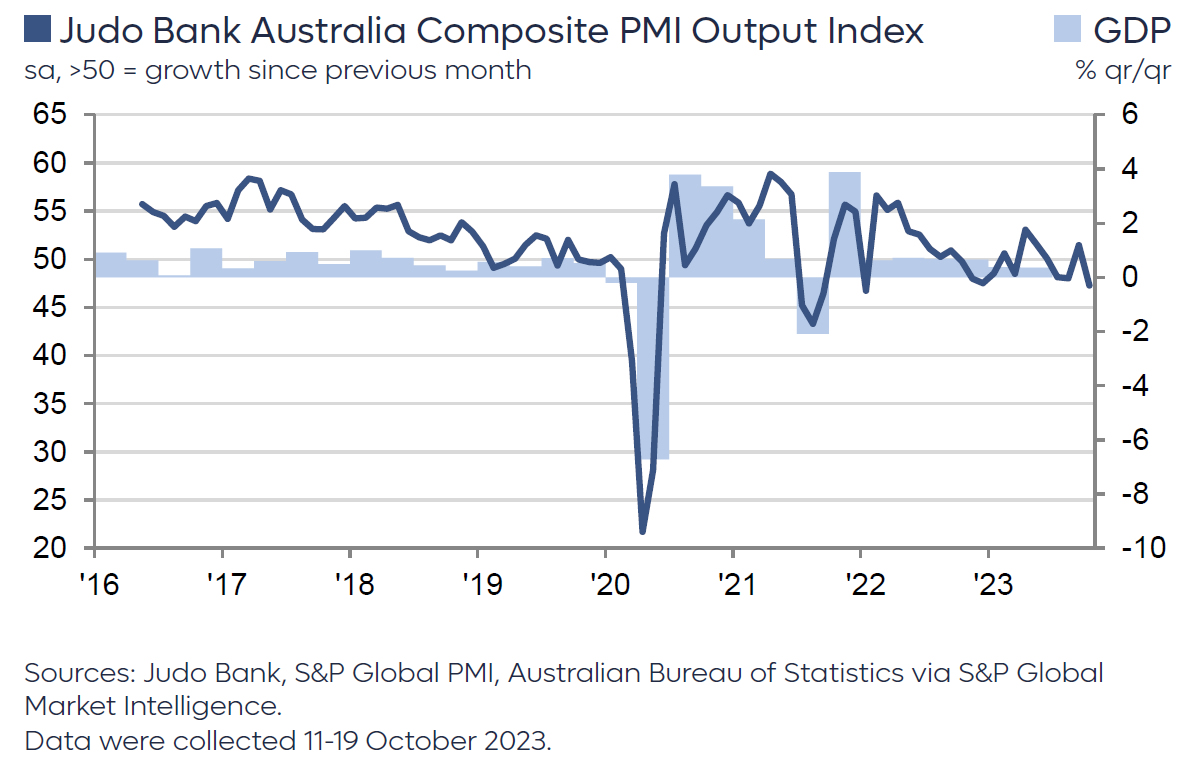

Australia’s economic indicators from October paint a worrisome picture, as PMI Manufacturing dipped to a six-month low at 48.0, down from 48.7. More significantly, PMI Services plunged to a 10-month trough, dropping from 51.8 to 47.6. PMI Composite, which combines both manufacturing and services, dropped to a concerning 21-month low of 47.3 from 51.5.

Weighing in on these figures, Warren Hogan, Chief Economic Advisor at Judo Bank, mentioned PMI output index reverting to cyclical lows around 47 after a brief rise above the neutral 50 mark in September. These PMI indicators resonate with the ongoing narrative that Australia’s economic momentum has decelerated in 2023, aligning with the anticipated gentle slowdown most economists had projected.

A silver lining, however, emerges from the employment index, which remains steadfastly above the 50-mark. Hogan interprets this as a sign that the deceleration in business activities hasn’t notably dampened hiring trends.

However, a significant area of concern highlighted by Hogan is the enduring nature of inflation pressures, which he refers to as “stickiness”. Both input and output price indexes remain elevated, not hinting at an imminent return of inflation to RBA’s target.

As RBA prepares for its board meeting, set to coincide with Melbourne Cup day, the latest PMI readings, especially concerning inflation, are unlikely to drastically influence the interest rate decision. Hogan articulated, “A strong case exists for a further modest upward adjustment to the Australian cash rate target, to ensure the economy remains on the so-called ‘narrow path’. If we are to avoid recession, Australia will need an extended period of below-trend growth to ensure inflation returns to target by 2025.”