{kind=link}

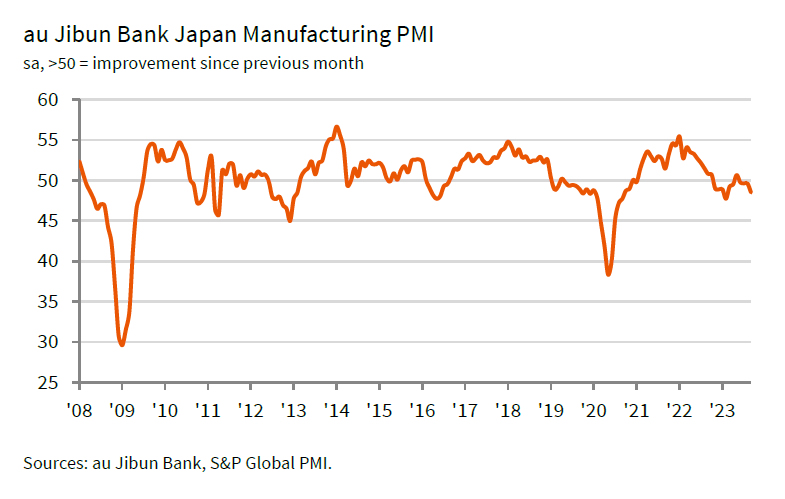

Japanese manufacturing sector is facing challenges as evidenced by the drop in PMI Manufacturing to 48.5 in September, down from August’s 49.6, the lowest level since February. Additionally, the average reading for Q3 stands at 49.3, a reduction from 50.0 in Q2.

According to key findings by S&P Global, the sector experienced faster falls in production and incoming new work. Alarmingly, backlogs declined at the strongest rate since April. A specific area of concern is the accelerated rate of input price inflation, reaching a four-month high, fueled by increasing costs of raw materials, oil, freight, and energy.

Usamah Bhatti at S&P Global Market Intelligence, conveyed a sombre view of the situation. He noted, “Depressed economic conditions domestically and globally weighed heavily on the sector, as both output and new orders were scaled back further. The decline in the latter was notably sharp, and the strongest seen for seven months.” The future outlook is also tinged with apprehension, as manufacturers signaled the most significant depletion in outstanding business in five months.

The inflationary aspect further complicates the picture. Bhatti highlighted, “The rate of input price inflation accelerated for the second month running to a four-month high.” Reports indicated that the sustained weakness of the yen is exacerbating the situation, elevating prices for inputs from abroad and placing an additional strain on firms.