{kind=link}

Oil prices shot up in response to an announcement from Saudi Arabia, the world’s leading exporter, to slash production by an additional 1 million barrels per day starting in July. This voluntary reduction from the Saudis comes on the heels of an agreement by OPEC and their allies, including Russia, to curtail supply into 2024.

Collectively referred to as OPEC+, this group accounts for approximately 40% of the world’s crude oil production. The group currently has cuts of 3.66 million barrels per day in place, which translates to about 3.6% of global demand.

The latest move by Saudi Arabia may take many by surprise, given that the most recent adjustments to quotas were implemented just a month ago. Consequently, the oil market is poised to tighten even further in the second half of 2023.

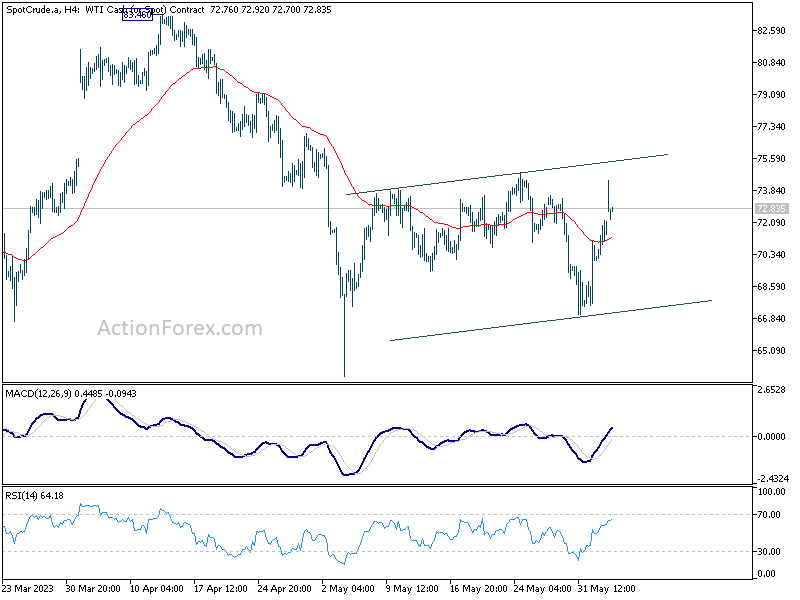

Technically speaking, however, WTI crude oil is just extending near term range trading. It’s currently struggling to break through 55 D EMA decisively. Rejection by 55 D EMA would set the stage for another fall through 64.19 low to resume the medium term down trend sooner rather than later. Even though sustained break of 55 D EMA could bring stronger rebound, 83.46 will still represent a significant medium term resistance to overcome.