and the timing of the first rate cut.){kind=link}

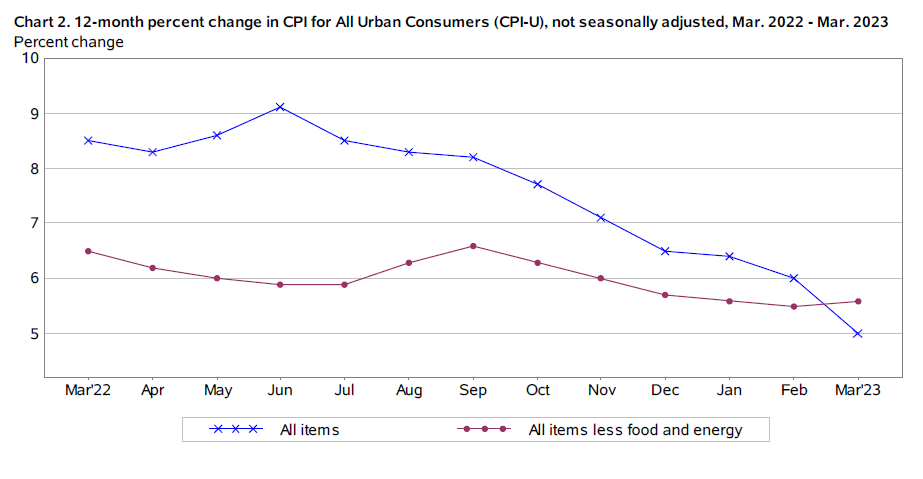

Today’s spotlight is on US consumer inflation data, which is expected to show that headline CPI remained unchanged at 5.0% yoy in April, after falling for nine straight months. Core CPI, which excludes volatile food and energy prices, is predicted to slightly drop from 5.6% yoy to 5.5% yoy. Both the trajectory of inflation and unfolding regional bank issues in the US will play a critical role in Fed decision-making about the peak interest rate in the current cycle (if it hasn’t been reached yet) and the timing of the first rate cut.

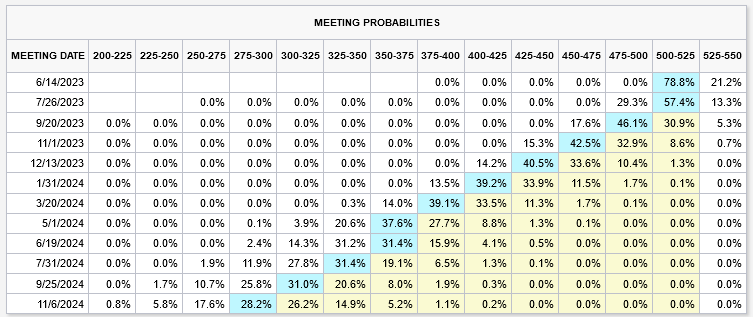

Current fed funds futures data suggests a 78.8% probability that Fed will maintain interest rate at 5.00-5.25% following FOMC meeting on June 14. There’s a 21.2% chance of an additional 25bps hike to 5.25-5.50%. Notably, there’s a 63.8% likelihood of a rate cut beginning in September, marking the start of a potential loosening cycle.

Despite these uncertainties, investor sentiment remains relatively resilient, with major stock indexes preserving their near-term bullish trajectories. NASDAQ, for instance, is expected to continue rallying as long as 11798.77 support level holds. The key test, however, will be 8.2% retracement of 16212.22 to 10088.82 at 12436.48. Decisive break above this level could trigger further rallies towards 13181.08 cluster resistance level (50% retracement at 13157.41) and possibly beyond.

Conversely, if NASDAQ breaks below 11798.77 support level, it would suggest a rejection by 12436.48 Fibonacci resistance level, possibly triggering a deeper decline towards 10982.80 and potentially retesting 10088.82 low.

As always, these movements in risk sentiment will likely have a correlated impact on currency market trends.