{kind=link}

Attention will turn to New Zealand’s Q1 in the upcoming session. Consensus expectations suggest that CPI will slow from Q4’s 7.2% yoy, with the majority of forecasts range from 6.9% to 7.1% yoy. Realizing such figures would present a downside surprise for RBNZ, which had projected a Q1 inflation rate of 7.3% yoy. With further slowing expected in subsequent quarters, the case for the RBNZ to pause at a terminate rate of 5.50% rate after another 25bps hike in May would strengthen if inflation indeed begins to cool.

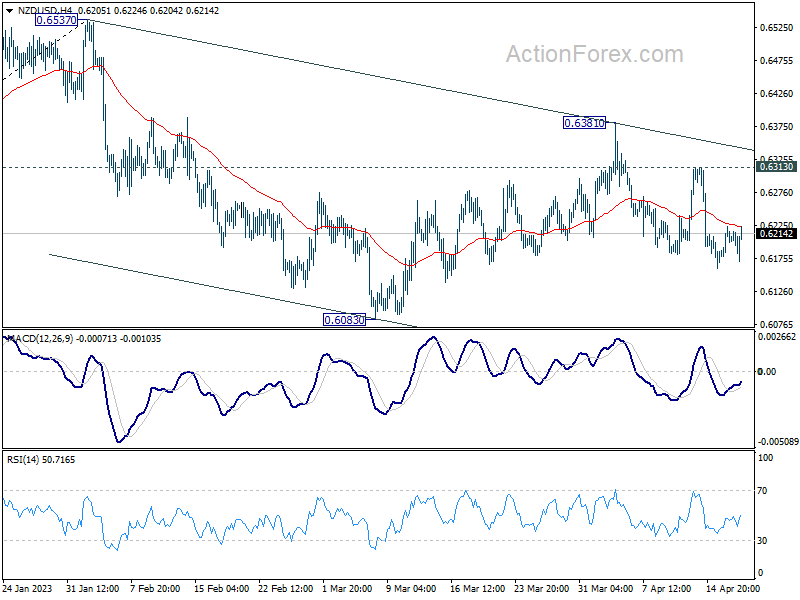

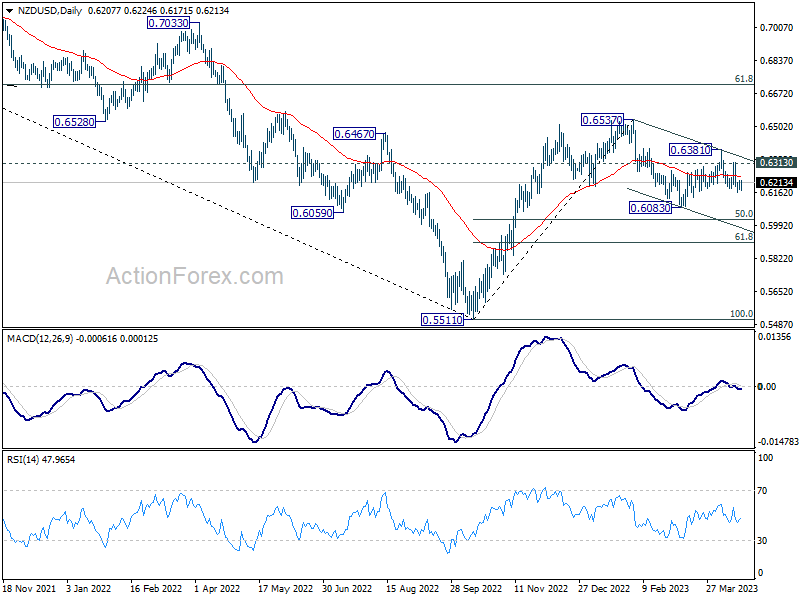

From a technical perspective, NZD/USD’s decline from its February high of 0.6537 is viewed as a correction to the uptrend originating from the 2022 low of 0.5511. The corrective structure of the bounce from 0.6083 to 0.6381 suggests the decline isn’t over yet. As long as the 0.6313 resistance holds, a deeper fall remains favored.

However, it’s worth noting that downside momentum has been relatively weak thus far. Consequently, even if the rate dips below 0.6083, strong support could emerge around 50% retracement of 0.5511 to 0.6537 at 0.6024, potentially completing the correction and forming a base.