{kind=link}

In the Monetary Policy Statement, RBA revised down GDP projections for 2021, projecting a slower recovery. There were also upward revisions in unemployment rate forecasts and downward in inflation forecasts. The central bank also reiterated that currency intervention and negative rates no appropriate for the moment.

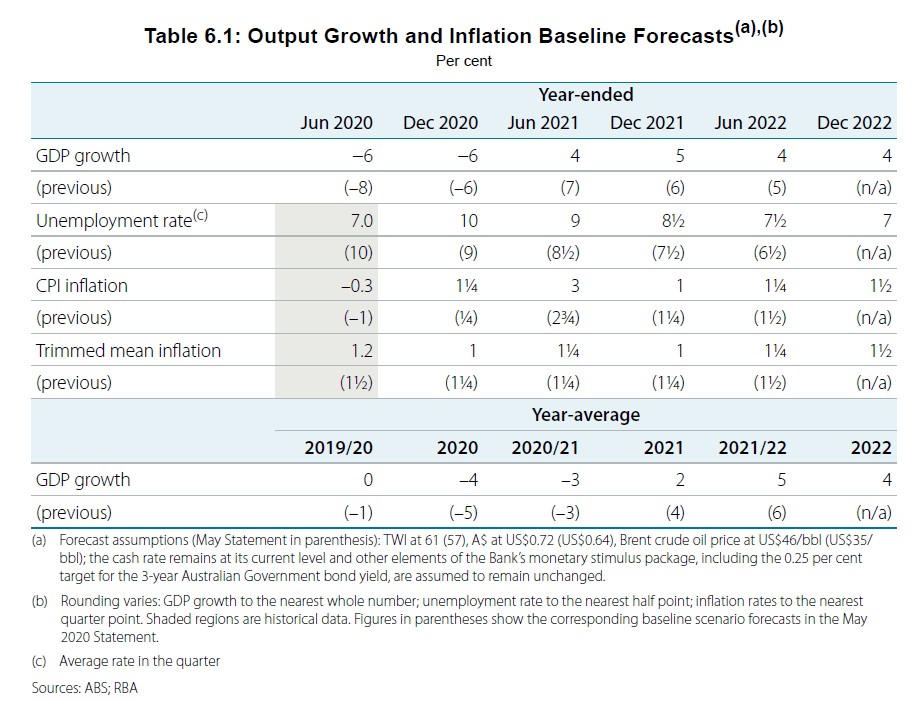

GDP contraction for year ending December 2020 was maintained at -6%. But a slower recovery is projected, at 5% for year ending December 2021, revised down from 6%. Growth is expected to slow further to 4% in the year ending December 2022.

Unemployment rate is projected be at 10% (revised from 9%) by 2020 end, then drop to 8.5% (revised up from 7.5%) in 2021 end, then to 7% in 2022 end. Trimmed mean inflation projections were also revised down to 1.00% (from 1.25%) in 2020 end, then 1.00% (from 1.25%) in 2021 end, and crawl back to 1.50% in 2020 end.

RBA said: “At a time when the value of the Australian dollar is broadly in line with its fundamentals and the market was working well, there was not a case for intervention in the foreign exchange market. Intervention in such circumstances is likely to have limited effectiveness.”

“The Board continues to view negative interest rates as being extraordinary unlikely in Australia. The main potential benefit is downward pressure on the exchange rate. But negative rates come with costs too. They can cause stresses in the financial system that are harmful to the supply of credit, and they can encourage people to save rather than spend.”