{kind=link}

SNB left sight deposit rate unchanged at -0.75% as widely expected. The central bank “remains will to intervene more strongly in the foreign exchange market”. The overall expansionary monetary policy “remains necessary”.

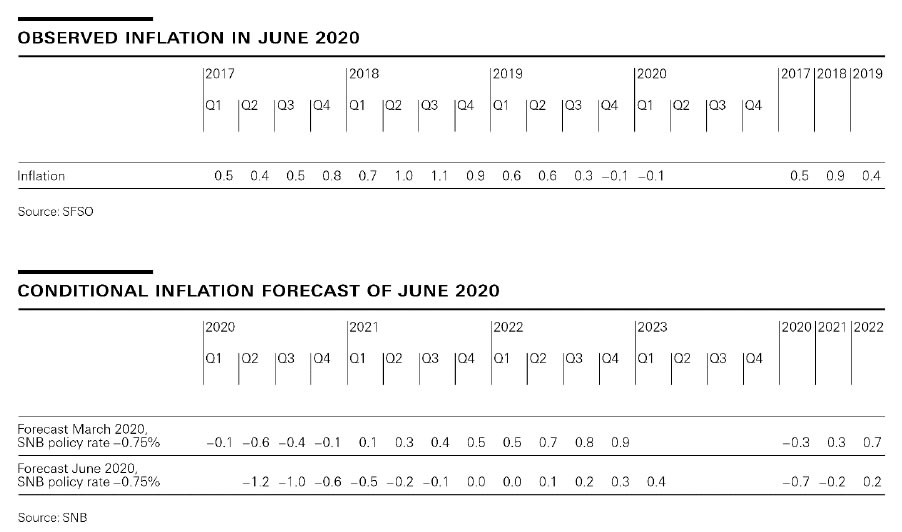

Inflation forecast is revised sharply lower. SNB projects inflation to bottom at -1.2% in Q2 2020, and stay negative with gradually improvement till Q2 2021. Inflation is not expected to turn positive until Q2 2022. The downward revision was primarily due to “significantly weaker growth prospects and lower oil prices”. The conditional inflation forecast is based on assumption that the policy rate remains at -0.75% over the horizon.

On Swiss economy, SNB expects the low points in term of activity came in April, and GDP decline is likely to be stronger in Q2 than in Q1’s -2.6%. Despite positive developments since May, SNB anticipates “there will be only a partial recovery” for the time being. GDP “will not return quickly to its pre-crisis level”. GDP is likely to contract by -6% in 2020, worst since oil crisis in 1970s.

In SNB’s baseline scenario for the global economy, further waves of coronavirus infections will be “successfully prevented”. But consumption, investment and demand is “likely to remain moderate for the time being”. Production capacity will be “underutilised for some time yet”. Inflation is likely to “remain modest” in most countries.