{kind=link}

New Zealand Dollar is having completely different fortunate comparing to Australian Dollar, even though the country is a step in the lockdown exit. Divergence on RBA and RBNZ policy expectations is a key driver in the comparative moves. Westpac said in a report last week that RBA target cash rate would stay at currently 0.25% level until end of 2023. On the other hand, Westpac said in another report today that RBNZ could cut interest rate to -0.50% by November.

Westpac expects a deeper decline in Q2 GDP by -16%, then followed by a stronger rebound of 13% in Q3. However, it said, “beyond the initial bounce we now expect the recovery phase will be slower, as it will take longer to overcome the damage done by unemployment and business failures”. Unemployment rate will peak at 9.5% followed by a “slow return” to below 5%.

It emphasized that “monetary policy not only needs to come to the party, it needs to spike the punch”. RBNZ is expected to double its QE to NZD 60B in May. OCR would be cut from current 0.25% to -0.50% in November. but the timing is uncertain.

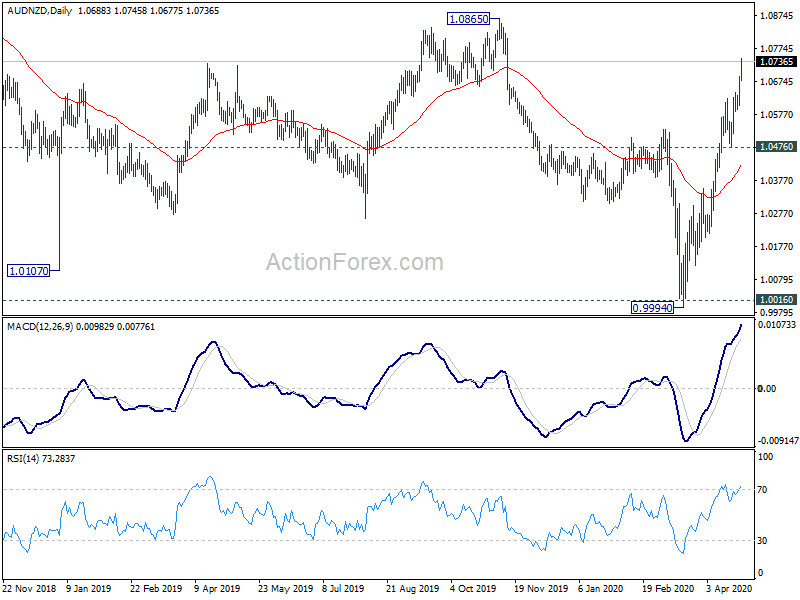

AUD/NZD hits as high as 1.0745 so far as rebound from 0.9994 extends. Current rise is seen as the third leg of the long term sideway pattern from 1.0016. Further rise could be seen to 1.0865 resistance. Real test is from trend line resistance (now at 1.0894). Sustained break there would pave the way to 1.1676 key long term resistance. And in any case, near term outlook will stay bullish as long as 1.0476 support holds, in case of pull back.