{kind=link}

New Zealand CPI rose 0.6% qoq 1.7% yoy in Q2, matched expectations. The annual rate accelerated from 1.5% yoy in Q1. However, the rise in headline inflation was largely due to the 5.8% quarter increase in petrol price, which contributed 0.25% to the 0.6% qoq figure. That suggests the pick-up could be temporary only, not to mention that annual CPI remains firmly below 2% mid-point of RBNZ’s 1-3% target range.

Stronger monetary stimulus and economic growth is required to lift inflation sustainably back to the 2% target. Yet, domestic and global headwinds remain. Thus, more OCR cuts are still expected for RBNZ. August could be the month to deliver even though it’s not totally certain yet.

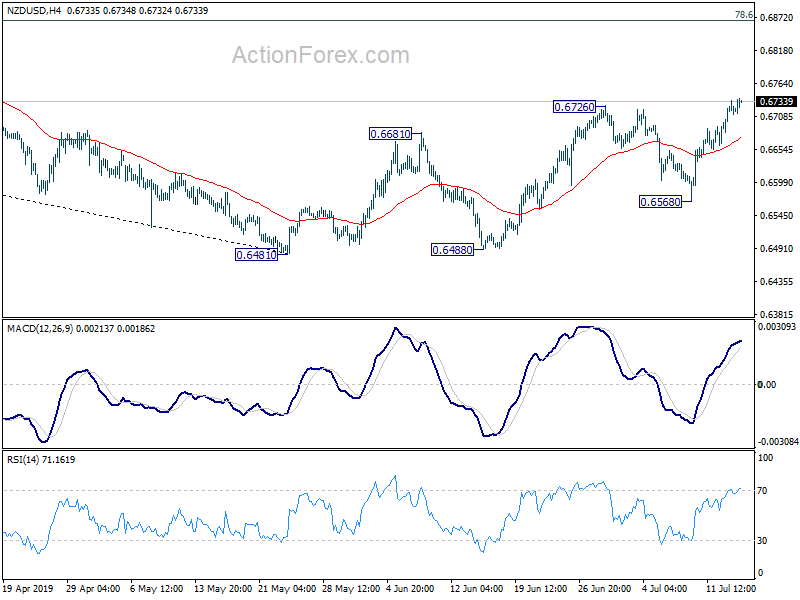

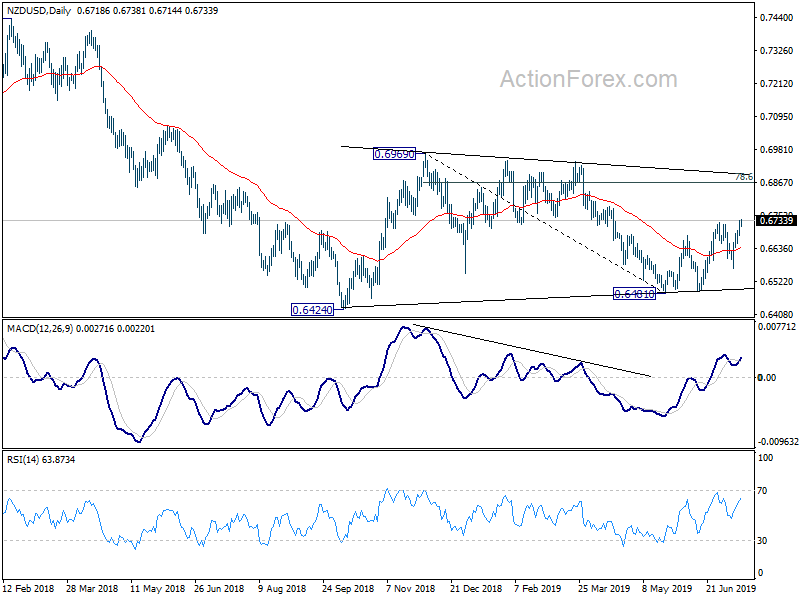

NZD/USD’s choppy rebound from 0.6481 resumed this week by taking out 0.6726 resistance. Such rise is seen as part of the sideway pattern from 0.6424. It should now be heading to 78.6% retracement of 0.6969 to 0.6481 at 0.6865. But upside should be limited below 0.6969 resistance to bring near term reversal.