{kind=link}

Market attention today is on US non-farm payroll data, with headline job growth anticipated to slow to 181k in April. Unemployment rate is predicted to remain steady at 3.5%, while average hourly earnings are expected to maintain a 0.3% mom pace.

Recent related data releases include a sharp rise in ISM manufacturing employment from 46.9 to 50.2 in April and a slight drop in ISM services employment from 51.3 to 50.8. Additionally, ADP private jobs saw a robust growth of 296k. But four-week moving average of initial jobless claims rose significantly from 198k to 239k.

Reactions to today’s non-farm payroll data may be complex, as investors will likely want to see job market loosening up with a cooldown in wage growth. However, concerns surrounding banks and Dollar’s reaction to Fed expectations, risk sentiment, and treasury yields also need to be considered.

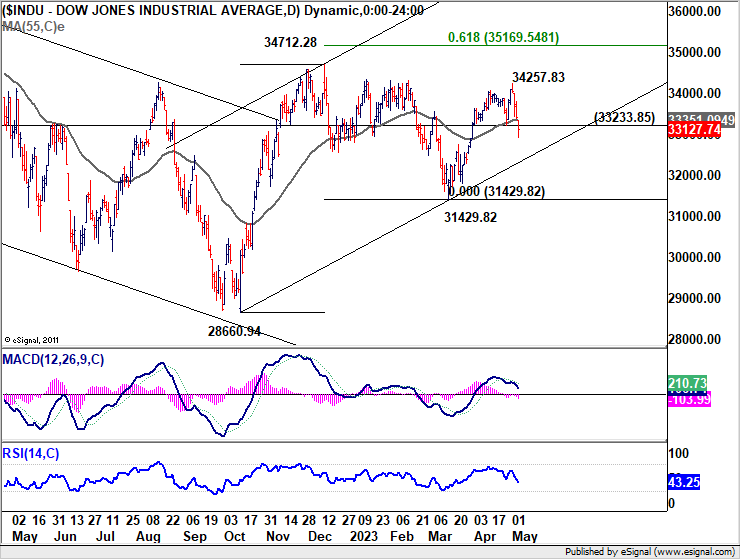

Following DOW’s strong break of 55 D EMA (now at 33351.09) and 33233.85 support overnight, rebound from 31429.82 appears to have completed at 34257.83. Whether the fall from there represents a correction to rise from 31429.82 or a falling leg of the pattern from 37412.28 remains to be seen. But a deeper fall is expected in the near term.

First line of defense will be trend line support at around 32350. The second line is 31429.82. Nevertheless a close above 55 D EMA for the week would revive near term bullishness.