{kind=link}

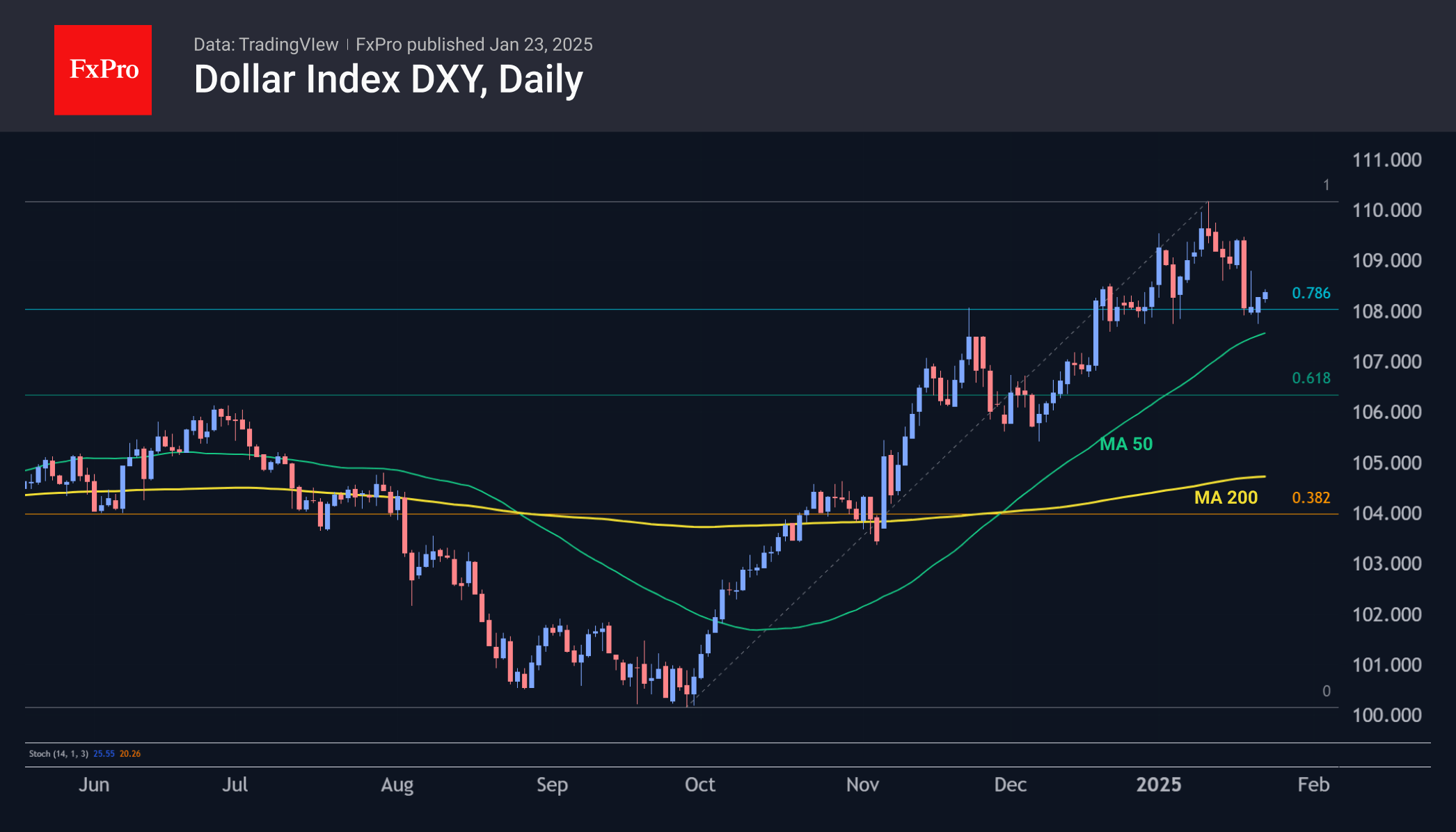

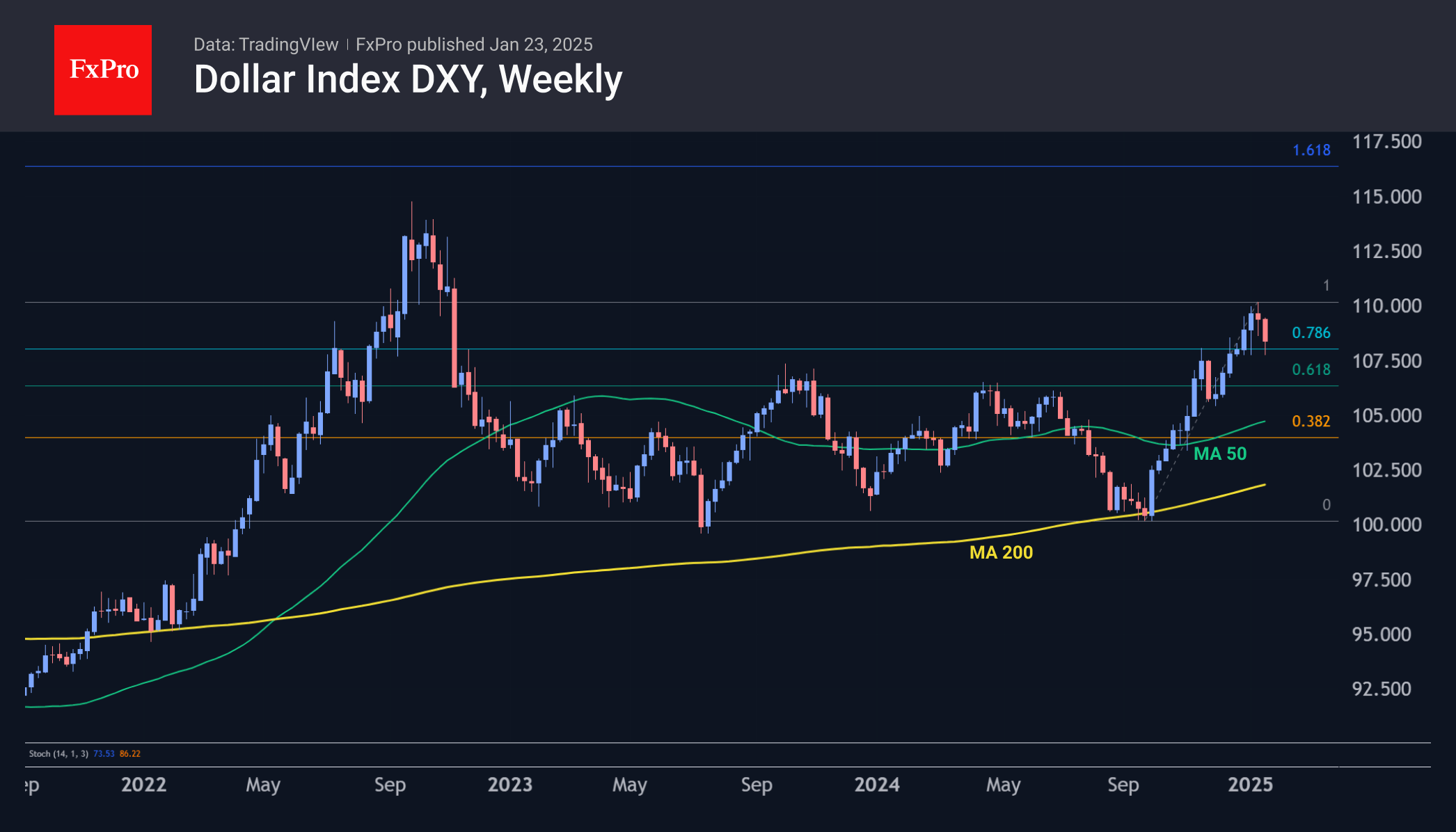

The US dollar accelerated its decline against its major peers, losing almost 2% to 107.1 this week before trimming some losses. Fundamentally, behind the dollar’s corrective pullback is the resurgence of expectations that the Fed will cut its key rate once or twice later this year. We recall that in early January, markets were pricing in a 30% chance of no rate change.

On the tech analysis side, the DXY pullback from 110 to 108 is within the scope of a typical correction. Also in favour of a corrective scenario is that the dollar got support this week on the decline to the 50-day moving average, near the November peaks. A test of this could be repeated next week. A close of the week under 107.40 (50-day MA) would force a deeper decline to 106 or potentially even 105. The ability to quickly return to the 110 area would make the 115-116 area the next bullish target.

Indices

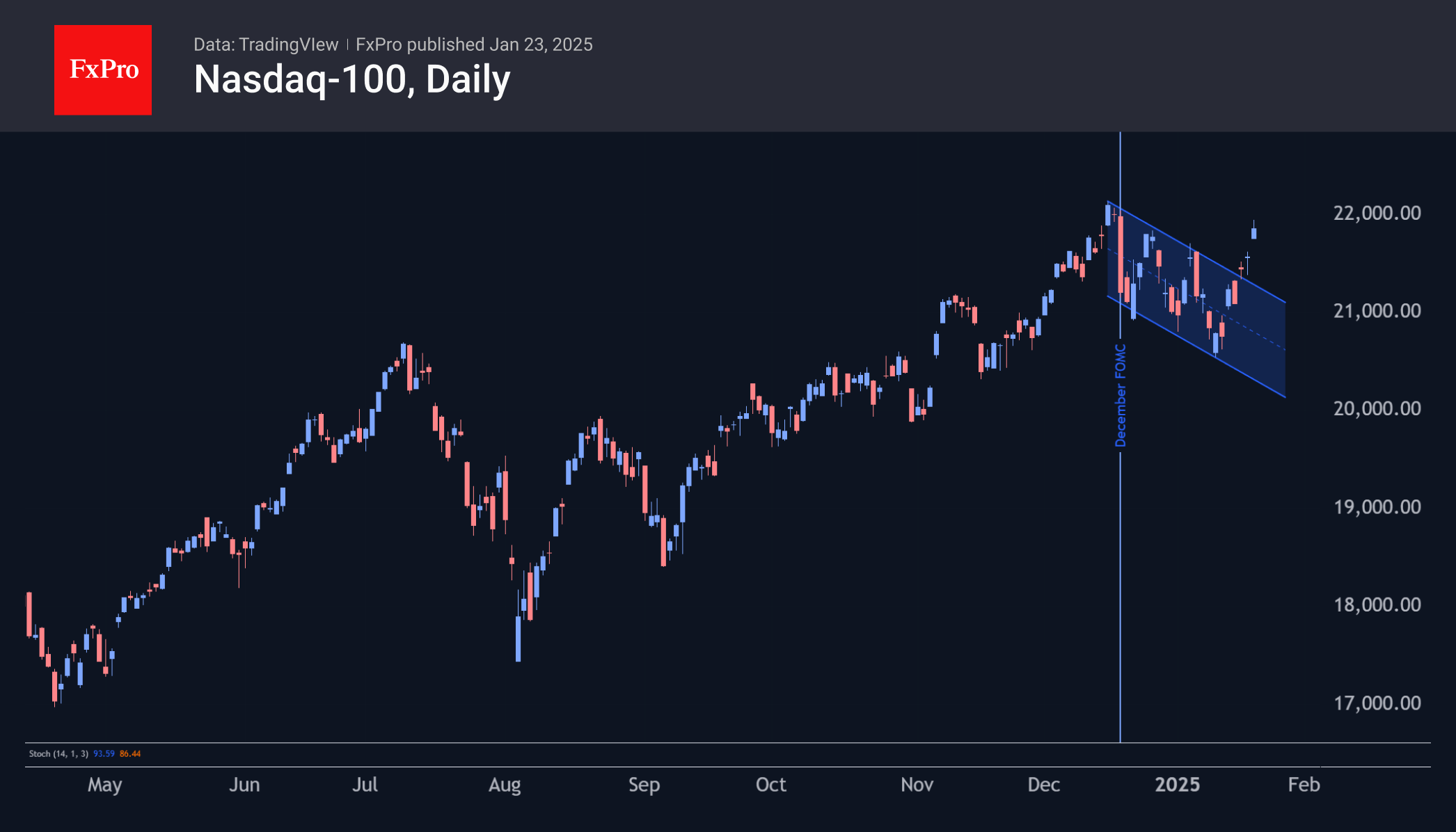

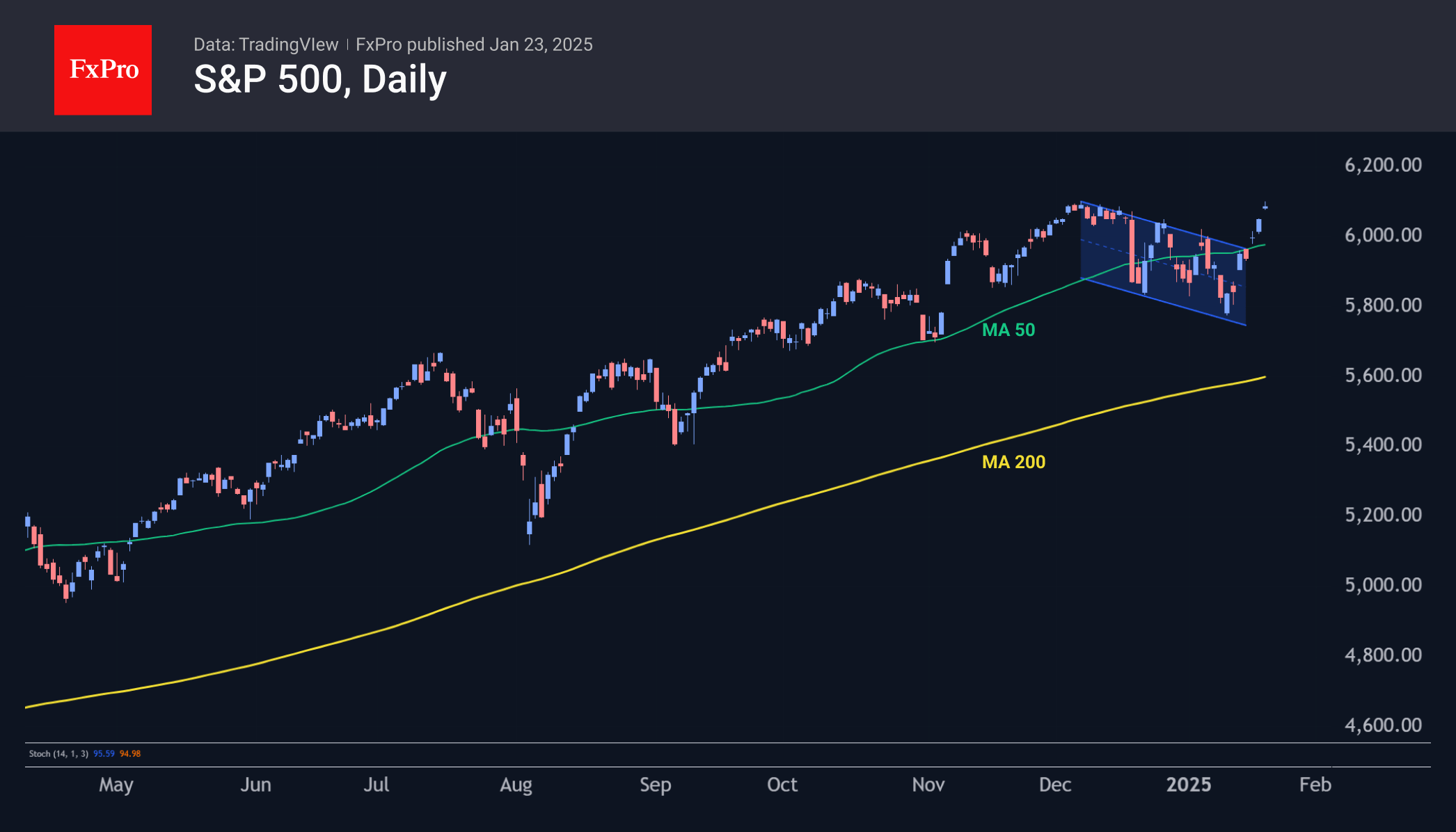

US indices maintained a positive trend for the second week in a row, with the S&P 500 setting a new all-time high above 6100. The Nasdaq100 and Dow Jones are about 1.5% below their records but have broken the downtrend that has been building since the second half of December.

Next week’s central event will be the Fed meeting. In December, the central bank’s tough tone took about 4% off each of the key US stock indices. The markets managed to recover these losses due to strong macroeconomics and company reports. Nevertheless, there are still some concerns that the Fed’s stance may once again deliver an unpleasant surprise.