{kind=link}

- The VIX (the implied volatility of the S&P 500) has inched higher above the 20 level in the pastour sessions.

- The VVIX/VIX ratio has moved lower since 16 September, and past data suggests a potential short to medium-term corrective decline in the S&P 500.

- Watch the key intermediate support of 5,675 on the S&P 500.

Since our last publication, the S&P 500 has continued to languish as it failed to recapture its gapped down formed last Thursday, 31 October, and its 20-day moving average, both acting as an intermediate resistance at 5,810.

The movement of the S&P 500 is now being bombarded with macro factors (the upcoming FOMC meeting on 7 November), firm-based risks (ongoing US Q3 earnings session), and political events (the outcome of the US presidential election and the balance of power status in Congress).

Hence, market participants are cautiously hedging on potential negative tail-risk scenarios that could occur in the US stock market, triggered by these factors; either individually or by a concoction of it.

These downside tail-risk protection strategies can be structured via options and or futures markets on stock market implied volatility instruments such as the VIX or the VVIX (implied volatility on the VIX aka VIX of the VIX).

Also, such hedging activities are likely to create a potential reflexive feedback loop into the US stock market which in turn may impact the price actions of the major US stock indices negatively.

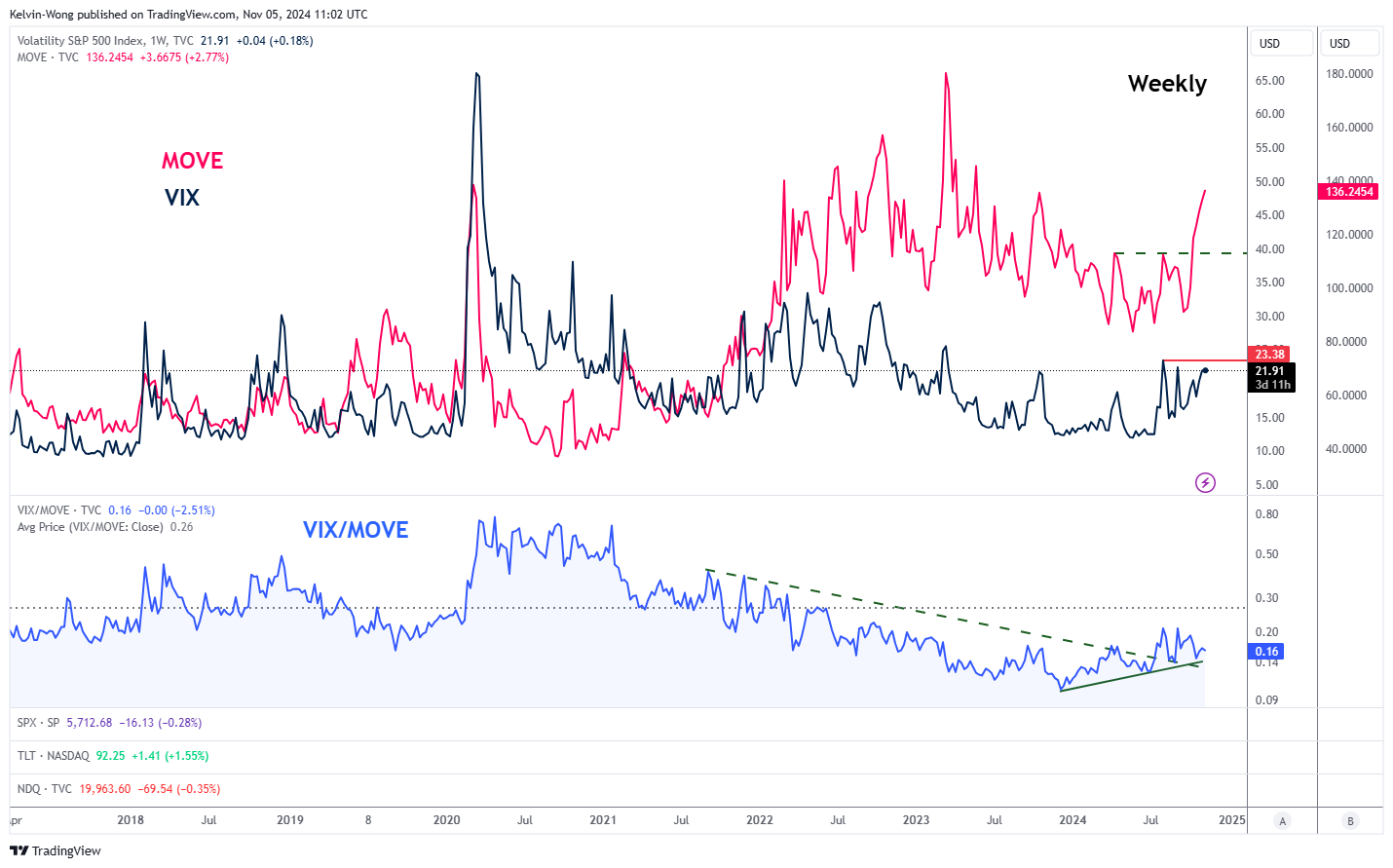

VIX has remained above 20 and the VIX/MOVE ratio is still above support

Fig 1: Major trends of MOVE Index, VIX & VIX/MOVE ratio as of 5 Nov 2024 (Source: TradingView, click to enlarge chart)

Since the week of 16 September 2024, the leading Merrill Lynch Option Volatility Estimate (MOVE) Index that reflects the level of volatility in U.S. Treasury futures has surged upwards significantly and cleared above a key medium-term resistance of 112.80.

The VIX (the implied volatility of the S&P 500) has lagged but still tagged along the movement of the MOVE Index and in the past four sessions inched higher above 20 where it recorded a closing level of 21.95 as of Monday, 4 November (see Fig 1).

In addition, the VIX/MOVE ratio has continued to print a series of “higher lows” and remained supported by an ascending trendline since July 2024 which suggests a potential looming outperformance of the lagging VIX over the MOVE Index.

Hence, a breakout above VIX key intermediate resistance of 23.38 may trigger a negative feedback loop into the S&P 500 at least on a short to medium-term time horizon.

The current VVIX value suggests a potential higher VIX

Fig 2: Medium-term trends of S&P 500 & VVIX/VIX ratio as of 5 Nov 2024 (Source: TradingView, click to enlarge chart)

The VIX is calculated from S&P 500 options, and the VVIX is calculated from VIX options. Therefore, a higher movement of VVIX suggests the VIX might be more volatile in the future, which in turn can indicate a market belief that the S&P 500 might also be more volatile.

If we take the relative movement of the VVIX against the VIX by plotting the ratio of VVIX/VIX along the movement of the S&P 500, we can see there are several past occasions since July 2023 that when the ratio of VVIX/VIX inched downwards (VVIX has a relatively higher value than the VIX), the S&P 500 staged a corrective decline of at least 6% thereafter during the periods of 27 July 2023 to 27 October 2023, 1 April 2024 to 19 April 2024, and 16 July 2024 to 5 August 2024.

Also, after these prior three periods of corrective decline sequences occurred on the S&P 500, it managed to stage bullish reversals when the VVIX/VIX ratio declined further to hit a level of 4.83 (see Fig 2).

In recent weeks, the VVIX/VIX ratio has steadily inched downwards since 16 September 2024 and as of 4 November, it has a value of 5.56 (still has room before hitting 4.83) which suggests the S&P 500 may stage a corrective decline towards the medium-term support of 5,390 (also the 200-day moving average) if the key intermediate support of 5,675 (also the 50-day moving average) is broken down.