{kind=link}

- The BoE meets on Thursday; no interest rate change is expected

- Quarterly projections could support market expectations for rate cuts

- Pound in need of a boost against the euro

Decision time for the BoE

The Bank of England will hold its third gathering for 2024 on Thursday. The press statement, the meeting’s minutes and the Monetary Policy Report will be published at 11:00 GMT, with the important press conference following 30 minutes later.

The market expects no change at the current bank rate of 5.25% with the focus being on three factors: the inflation projections in the Monetary Policy Report, the voting pattern, and the overall rhetoric at the press conference.

What changed in the economy since the last meeting?

Since the BoE’s March 21 meeting, data has been mostly mixed. The economy appears to have returned to growth during the first quarter of 2024, as made evident by the PMI surveys. Similarly, the housing sector is showing signs of life despite the higher interest rates.

Inflation though remains the BoE’s main problem. With the labour market not yet falling off a cliff and retail sales showing some leftover consumer appetite, inflation is still elevated with the core CPI indicator remaining above 4% for the 28th consecutive month. In addition, average earnings continue to grow at a high pace with the MPC member Greene recently pointing out that “wage growth in services price inflation is not consistent with this sustainable return to 2% inflation”.

Quarterly forecasts to hit the newswires at 11:00 GMT

The February Monetary Policy Report showed headline inflation dropping to 2.3% by the end of 2026. An upwards revision of the inflation outlook would probably deliver a strong blow to the current market expectations and possibly raise the bar for any imminent rate cuts. On the other hand, a drop below the 2% threshold for the 2026 figure could go a long way towards cementing a rate cut over the next few meetings.

Could the hawks vote for a rate hike again?

BoE members Mann, Haskel and Greene voted consistently for rate hikes since the August 2023 meeting. However, the gradual easing in inflation since the start of the year forced them to side with the majority once again. They will most likely stick with the majority camp at this gathering as well, even though they acknowledge that more progress is needed on the inflation front.

Another uneventful meeting?

On the back of the latest economic developments and Wednesday’s Fed meeting most likely keeping the door shut to rate cuts over the summer, the BoE does not appear ready for a dovish shift. The markets are currently fully pricing in a 25bps rate cut by September, but inflation remains a thorn in the BoE’s side.

Provided that the quarterly forecasts do not point to a significant easing of inflation in the forecast period, Governor Bailey is expected to maintain the current somewhat dovish stance at the press conference and keep his cards close to the chest. Developments in the Middle East, with its likely implications on oil prices, China, and the Fed’s refusal to signal rate cuts do not leave much more for complacency.

However, there will be lots of talk about the April inflation figure. Due to energy prices being much lower this time around compared to April 2023, inflation could drop to just above the 2% level. Bailey et al could brand this move as monetary policy victory but the hawks have already expressed their view that inflation will gradually pick up, closing the door to hasty decisions.

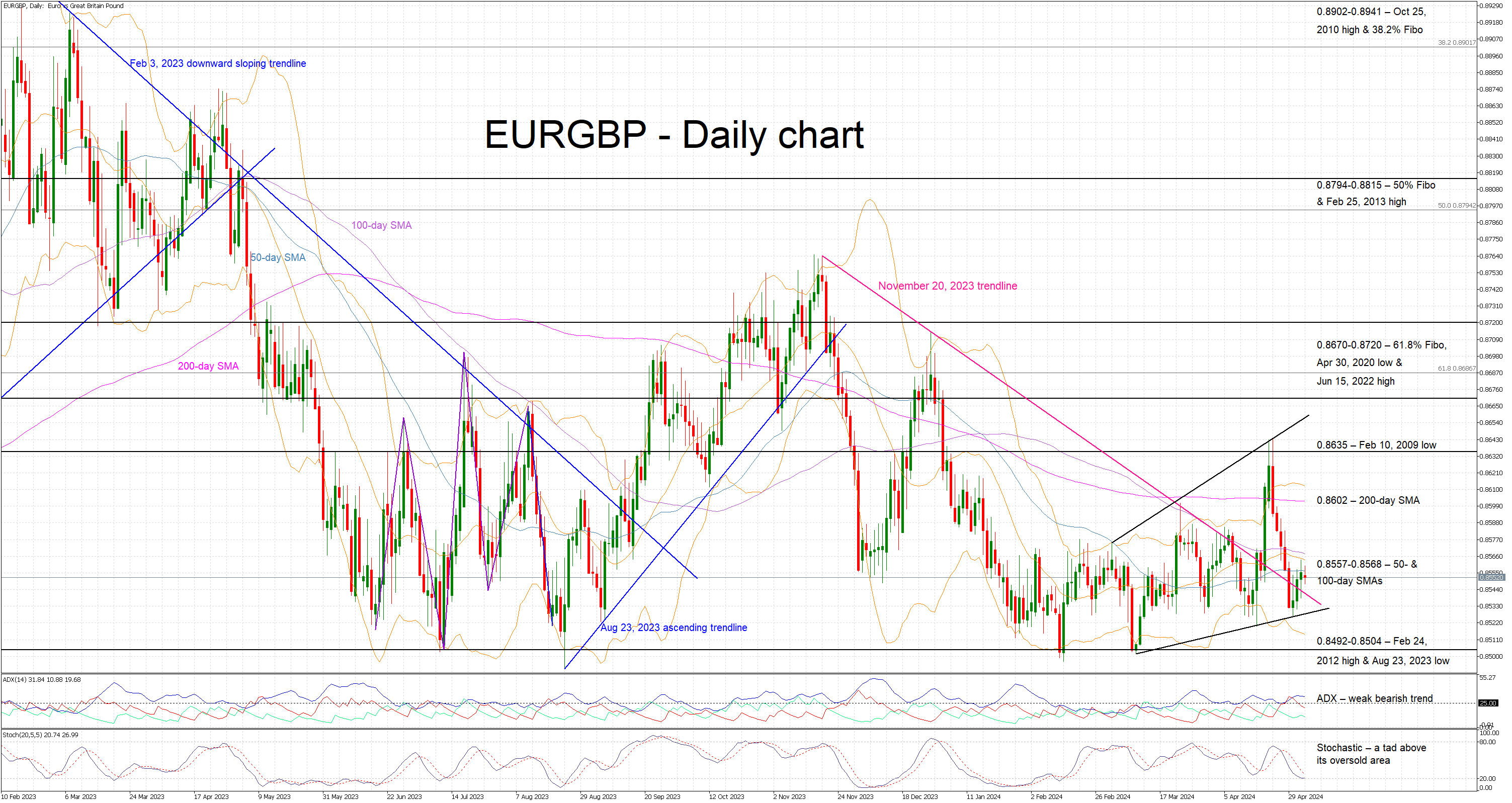

The pound’s fate is at the hands of the BoE

Market analysts are currently split for a June rate cut. A BoE gathering pre-committing to a June rate cut, could leave the pound unsupported with the euro/pound pair possibly rallying towards the 200-day SMA and potentially threatening the April 2024 highs.

On the flip side, another uneventful meeting could cause this pair to bounce lower towards the early March lows at the 0.8492-0.8505 area.