.){kind=link}

The price actions of the USD/JPY have reacted negatively right below the 150.70 key resistance as highlighted in our previous analysis and shed -435 pips/-2.9% to print a recent intraday low of 146.48 on 8 March.

Thereafter, the USD/JPY has drifted higher to trade back above the 148.00 psychological level in light of the “not so soft” US inflation data (CPI & PCE) for February that increases the odds that the US Federal Reserve is in no rush to cut its Fed funds rate in March and even during May’s FOMC meeting; that’s pushing backward the highly anticipated first rate cut down the calendar.

Interestingly, the Japanese side of the equation has failed to spur a renewed leg of JPY strength. Last Friday, Rengo, Japan’s largest trade union federation announced that it has secured a stronger-than-expected average employee wage increase of 5.28% in the preliminary wage negotiations result for FY 2024/2025, above last year’s increase of 3.58%, and its largest wage hike since 1991.

In recent months, Bank of Japan Governor Ueda has heavily emphasized that a sustainable wage increase is a key deciding factor for BoJ to normalize its current ultra-accommodative monetary policy.

Given the latest big jump in Japanese employees’ wages, local press Kyodo and Nikkei reported that BoJ will raise the short-term interest rate to the 0% to 0.1% range tomorrow, 19 March, at the end of its two-day monetary policy meeting, citing sources close to BoJ. The Nikkei stated that BoJ could go the extra mile tomorrow by scrapping the Yield Curve Control (YCC) program on the 10-year Japanese Government Bond (JGB) yield, that’s total removal of the limits where the 1% upper limit is being used as a “reference level” for now.

No JPY strength resurgence so far despite supporting fundamentals & news flow

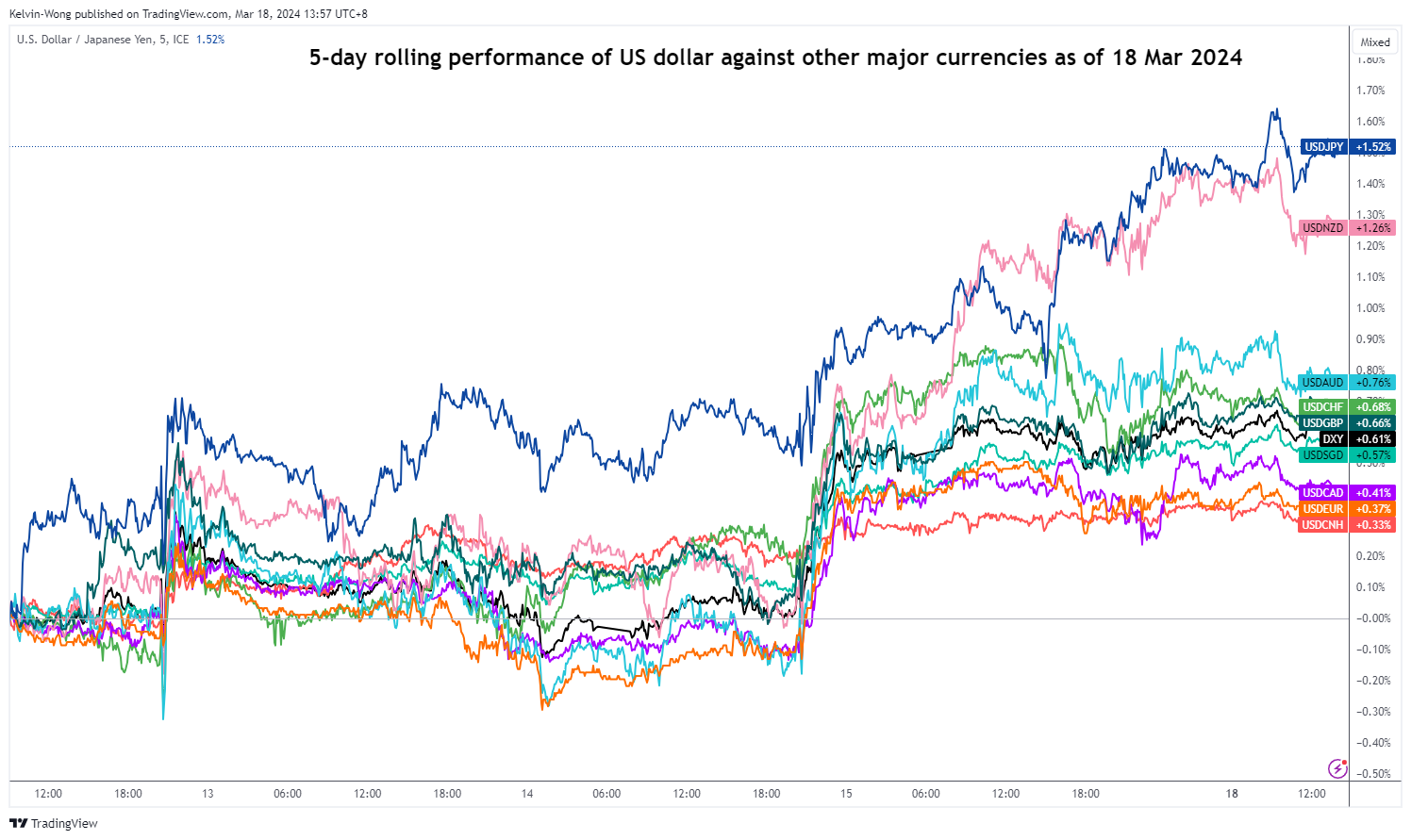

Fig 1: 5-day rolling performance of USD against other major currencies as of 18 Mar 2024 (Source: TradingView, click to enlarge chart)

However, the current price action movements of USD/JPY do not seem to reflect such positive fundamentals and news flows that are supportive of JPY strength; instead, the USD/JPY has continued to extend its rally last Friday, ex-post Rengo’s wage hike results, and added +131 pips/+0.9% to print a current intraday high of 149.33 at this time of the writing.

Based on a 5-day rolling performance of the US dollar against other major currencies, the USD/JPY pair is the top performer so far with a gain of +1.5% (see Fig 1).

The current bout of JPY weakness may be mispriced

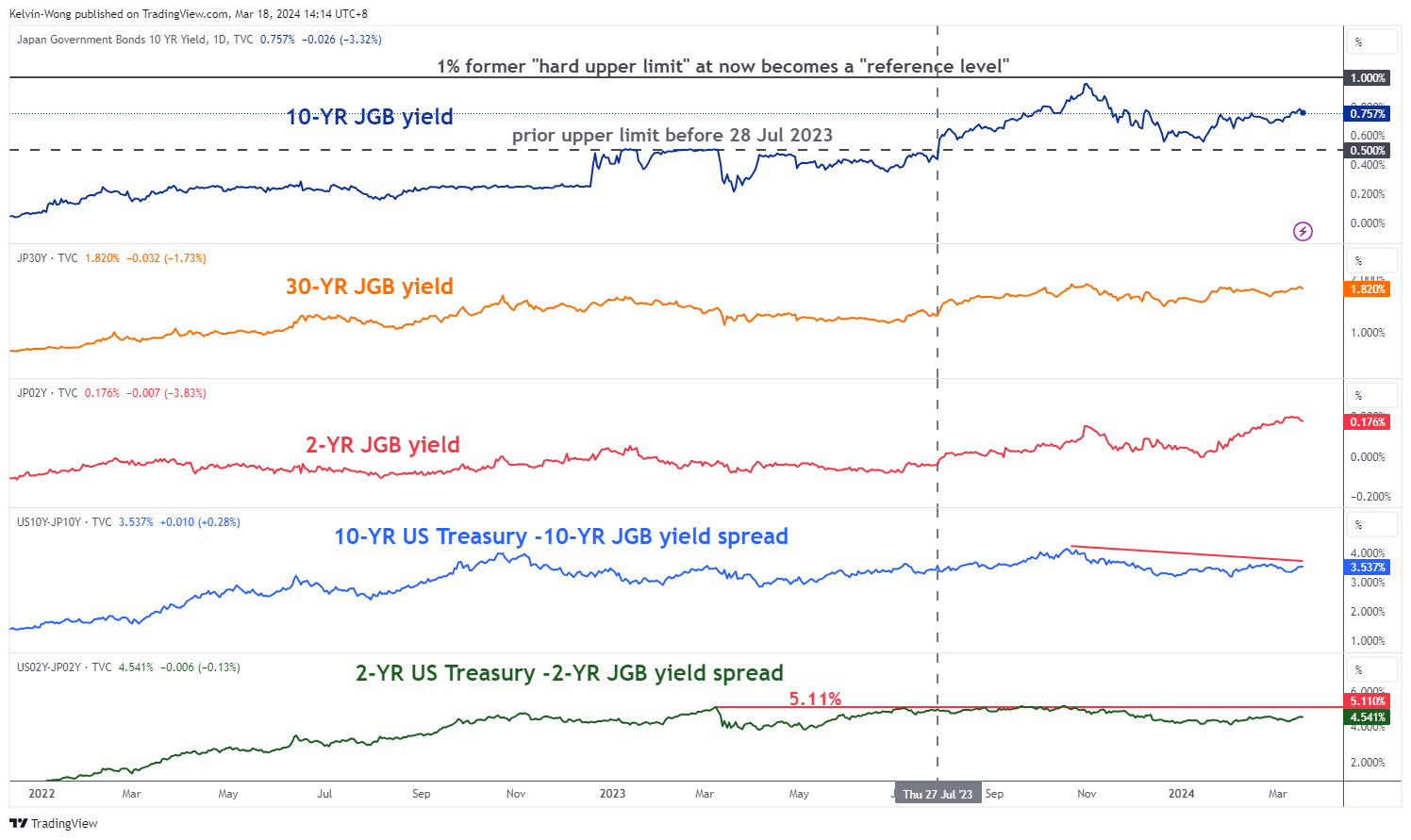

Fig 2: JGB yield curve spread major trends as of 18 Mar 2024 (Source: TradingView, click to enlarge chart)

Fig 3: US Treasuries/JGB yield spread medium-term trends as of 18 Mar 2024 (Source: TradingView, click to enlarge chart)

The current bear-steepening trajectory of the JGB yield curve for both the 10-year/2-year spread and 30-year/2-year spread in place since late June 2022 and most recently, both of the yield curve spreads have managed to stage a rebound from their respective ascending channel supports at 0.54% (10-year/2-year) and 1.60% (30-year/2-year) (see Fig 2).

A bear-steepening yield curve movement is being driven by the longer-end (10-year and 30-year JGB yields) that are rising at a faster pace than the lower-end (2-year JGB yield) suggests that the Japanese economy is showing no clear signs of reverting to a deflationary environment which in turn allow BoJ more room to kickstart the normalization of its ultra-accommodative monetary policy soon.

Secondly, both the long and short-end yield spread between the US Treasuries and JGBs are still capped below their respective key resistance levels; 3.8% (10-year) and 5.11% (2-year) (see Fig 3).

Watch the 20-day moving average of the USD/JPY

Fig 4: USD/JPY short-term trend as of 18 Mar 2024 (Source: TradingView, click to enlarge chart)

The recent two weeks of rally seen in USD/JPY from its 8 March low of 146.48 has now reached a key inflection level of 149.50 that is coincided by the 20-day moving average acting as a resistance, upper boundary of its minor ascending channel in place 8 March low, former minor swing lows of 15 February/29 February, and close to the 76.4% Fibonacci retracement of the prior minor decline from 27 February high to 8 March low (see Fig 4).

In addition, the hourly RSI momentum indicator has flashed a bearish divergence condition at its overbought region which suggests a potential easing of the recent upside momentum of USD/JPY.

If the 149.50 key short-term pivotal resistance is not surpassed to the upside, the USD/JPY may stage a potential bearish reaction to expose the near-term supports of 148.80/60 and 147.95 in the first step.

On the other hand, a clearance above 149.50 invalidates the bearish bias for a squeeze up for the next near-term resistance to come in at 150.15, and above it exposes the lower limit of a major resistance zone at 150.65/85.