{kind=link}

The dollar index holds in red but within a narrow range in early Wednesday, as traders reduce speed ahead of today’s key events, US labor data and the speech of Fed Chair Powell.

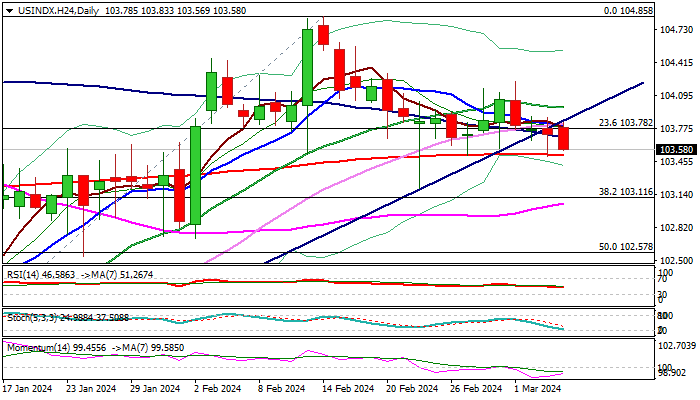

Weaker than expected US services PMI in February, released on Tuesday, added to negative sentiment, though dips were again contained by 200DMA (103.52) which keeps the downside protected for the third straight week.

Conflicting daily studies (momentum is negative, MA’s in mixed setup) lack clearer direction signal, suggesting that fundamentals will be key market drivers today.

Fed Chair Powell, in his testimony before Congress, is expected to reiterate the stance that the central bank will wait for more data before making decision to start easing monetary policy, as core inflation remains elevated, though this is unlikely to impact wide expectations for the first rate cut in June (current bets stand at 60%).

Releases of US Feb ADP private sector payrolls (149K f/c vs 107K Jan) and US JOLTS job openings report for January (8.8M f/c vs 9.02M in Dec) will provide more details about the condition in the US labor sector and contribute to Fed’s rate outlook.

Expect initial bearish signal on firm break of 200DMA, which would look for confirmation on extension and close below pivots at 103.11/05 (Fibo 38.2% of 100.29/104.85 rally/55DMA).

Conversely, bounce and close above 103.80 zone (broken bull-trendline/10DMA) would ease downside pressure, with lift and close above 104.00/20 zone (20DMA / Mar 1 lower top) to bring bulls back to play.

Res: 103.80; 104.02; 104.22; 104.56.

Sup: 103.52; 103.19; 103.05; 102.73.