{kind=link}

- Current bout of risk-off behaviour has triggered an underperformance of higher beta risk-sensitive currencies such as the AUD.

- China Premier Li Qiang’s speech in Davos has signalled “a lesser need” for China to enact massive stimulus measures which in turn may see lesser industrial commodities exports from Australia in the near term.

- AUD’s weakness has led to a short-term uptrend unfolding in the EUR/AUD cross pair.

The risk-off behaviour has continued to spill over to today’s 17 January Asian session where the US dollar has continued to strengthen after it hit a 1-month high and benchmark Asian stock indices have recorded intraday losses across the board led by the underperformers (China & Hong Kong); CSI 300 (-0.84%), Hang Seng Index (-3%), Hang Seng TECH Index (-4.10%), and Hang Seng China Enterprise Index (-3.14%). Even the recent outperformer, Japan’s Nikkei 225 is not spared from today’s bearish onslaught with an intraday loss of -0.40%.

The current bout of risk-off negative feedback loop has been triggered by a rising geopolitical risk premium arising from the hostilities in the Middle East region and the Red Sea shipping route.

In addition, Fed Speak from Federal Reserve Governor Christopher Waller (voting FOMC member) poured cold water on the expected Fed’s dovish pivot narrative by stating that the Fed may not need to cut as quickly as in the past which suggests potential guidance that tries to push back the current dovish expectations of six cuts in 2024 on the Fed funds rate as priced by in the interest rates futures market.

AUD & NZD worst performers

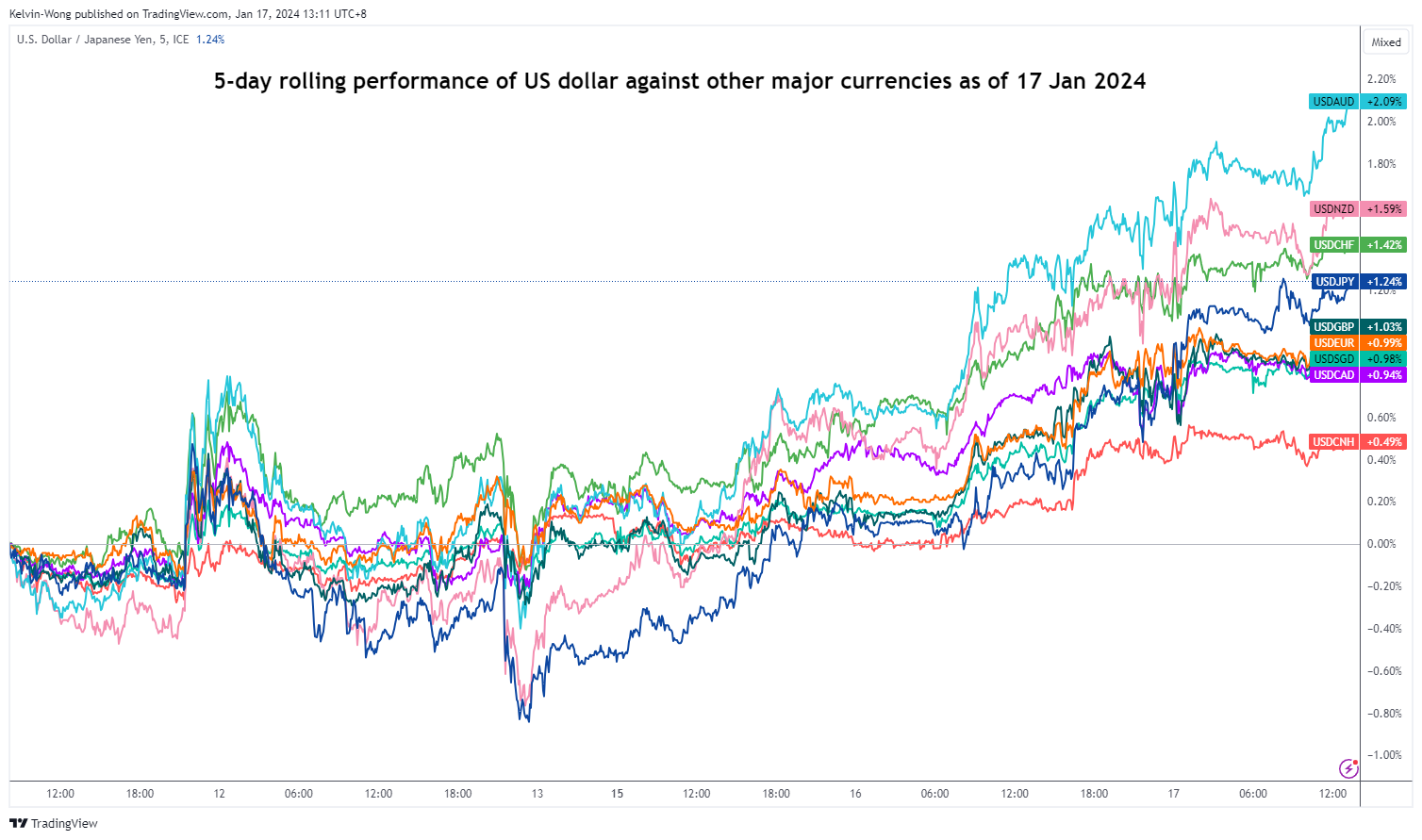

Fig 1: 5-day rolling performances of US dollar against other currencies as of 17 Jan 2024 (Source: TradingView, click to enlarge chart)

The net effect so far in the foreign exchange market is the significant underperformance of the higher beta risk-sensitive currencies; AUD and NZD where it shed -2.10% and -1.60% respectively against the US dollar based on a 5-day rolling basis at this time of the writing.

The AUD also took a double whammy from a China-related news flow via a commodities export perspective. China’s Premier Li Qiang said in Davos, during one of the sessions of the ongoing World Economic Forum that China has managed to achieve an annualized GDP growth of 5.2% in 2023 without resorting to massive stimulus measures.

This remark has implied that China’s top policymakers are comfortable with the current pace of growth trajectory in China which in turn has dampened hopes of more forceful fiscal and monetary stimulus measures in 2024. Hence, China may not need to import massive amounts of industrial commodities such as copper which Australia is a major exporter to China.

EUR/AUD short-term bullish trend is taking shape

Fig 2: EUR/AUD medium-term trend as of 17 Jan 2024 (Source: TradingView, click to enlarge chart)

Fig 3: EUR/AUD minor short-term trend as of 17 Jan 2024 (Source: TradingView, click to enlarge chart)

The EUR’s intraday weakness seen in the past two days is not as pronounced as the AUD which in turn gives an opportunity for the EUR/AUD cross pair to evolve into a short-term bullish trend in place since the start of this year; it has rallied by +440 pips/+2.7% from its 2 January low of 1.6129 to current intraday high of 1.6570 at this time of the writing.

Medium and short-term momentum readings as indicated by the daily and hourly RSI are still showing bullish momentum conditions which may support a further potential upmove in price actions that have also just surpassed the 200-day moving average.

Watch the 1.6450 short-term pivotal support (also the 50-day moving average) with the next intermediate resistances coming in at 1.6655 and 1.6720.

On the other hand, failure to hold at 1.6450 negates the bullish tone to expose the next intermediate support at 1.6300 (also the 20-day moving average & 61.8% Fibonacci retracement of the ongoing minor rally from the 2 January 2023 low to today’s current intraday high).