{kind=link}

The US dollar remains at the back foot and extends weakness in European trading on Tuesday, ahead of key event – US inflation report for January.

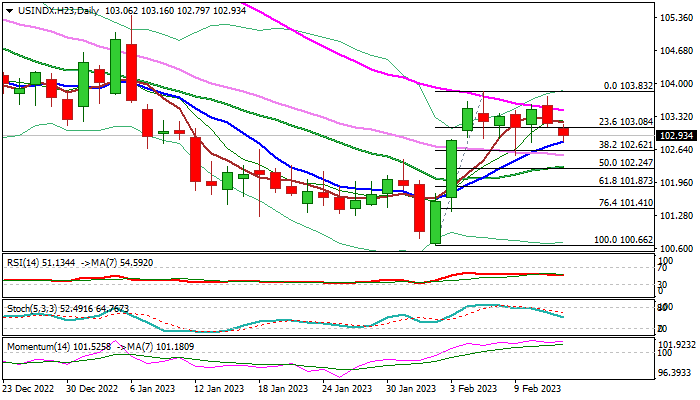

Fresh bears are in control for the second consecutive day following repeated failure at pivotal barriers at 103.43/58 (55DMA / Fibo 61.8% of 105.39/100.66 bear-leg) and test initial support at 102.79 (rising 10DMA) which also marks the floor of seven-day range.

Potential break lower would increase downside risk on formation of a double-top pattern on daily chart and add to signals that short correction from 100.66 (Feb 2 low) might be over.

Daily indicators are heading south and contribute to negative near-term outlook, as the action is heavily weighed by thick falling daily Ichimoku cloud (base of the cloud lays at 104.12).

The greenback is in defensive ahead of key US data, with annualized inflation expected to ease to 6.2% in Feb from 6.5% in Jan, but monthly figure is expected to jump by 0.5% following 0.1% increase previous month.

Although the core inflation (excluding volatile food and energy components) is also forecasted to ease to 5.5% in Feb from 5.7% in Jan, economists remain concerned as core inflation’s values of nearly three times above Fed’s 2% target, warn that price pressure is still strong and imply that the US central bank may opt for extended tightening period in efforts to bring inflation under control and push it towards 2% target.

Expectations for annualized CPI range from 6.1% to 6.7%, with release above consensus to offer fresh boost to the dollar, as rising inflationary pressure would add to the scenario of hiking interest rates above expected targets, while lower figures in Feb to boost optimism that inflation have peaked and increase pressure on dollar.

Res: 103.43; 103.83; 104.14; 104.28.

Sup: 102.79; 102.50; 101.87; 101.41.