{kind=link}

With the preliminary fourth-quarter GDP print on Friday saving the UK from declaring two consecutive quarters of negative growth, the focus turns to Tuesday’s inflation numbers. The calendar is filled with economic data releases including labour market statistics on Tuesday, but the market seems to care primarily about the CPI prints. Could we finally see the much-awaited dip in inflationary pressures or will the Bank of England remain under pressure to adopt a more aggressive strategy?

Sticky inflation, many reasons

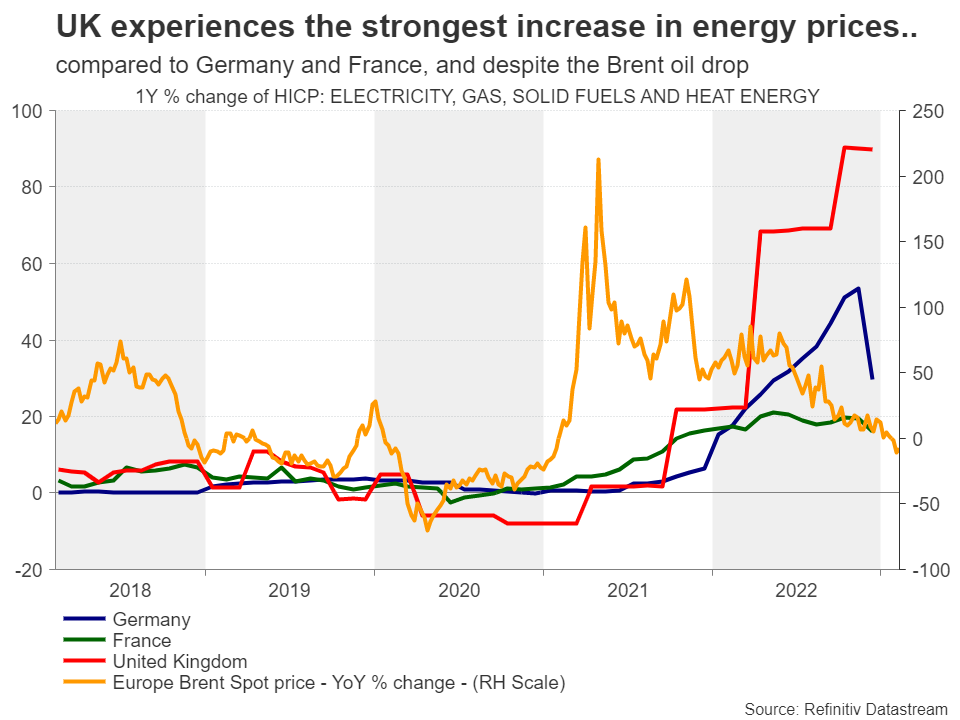

The repeatedly positive news on the employment front has been set aside as the focus rests on the elevated inflation rates. Particularly in the case of the UK, the CPI year-on-year change remains in double digits for the past four months, despite the decent deceleration seen elsewhere. Interestingly, the electricity, gas and other fuels subcomponent of the CPI continues to fuel the elevated UK inflation prints amidst a continued drop in oil and gas prices in Europe. One of the main reasons for this condition could potentially be the lower energy support programmes offered by the UK government compared to the other two heavyweight countries in Europe, Germany and France. Critically, the UK government’s Energy Price Guarantee is changing from April 2023 and another rise in energy costs for households is on the cards, which could potentially mean that the much-wanted dip in CPI might be pushed even further out.

Pressure on the BoE to increase?

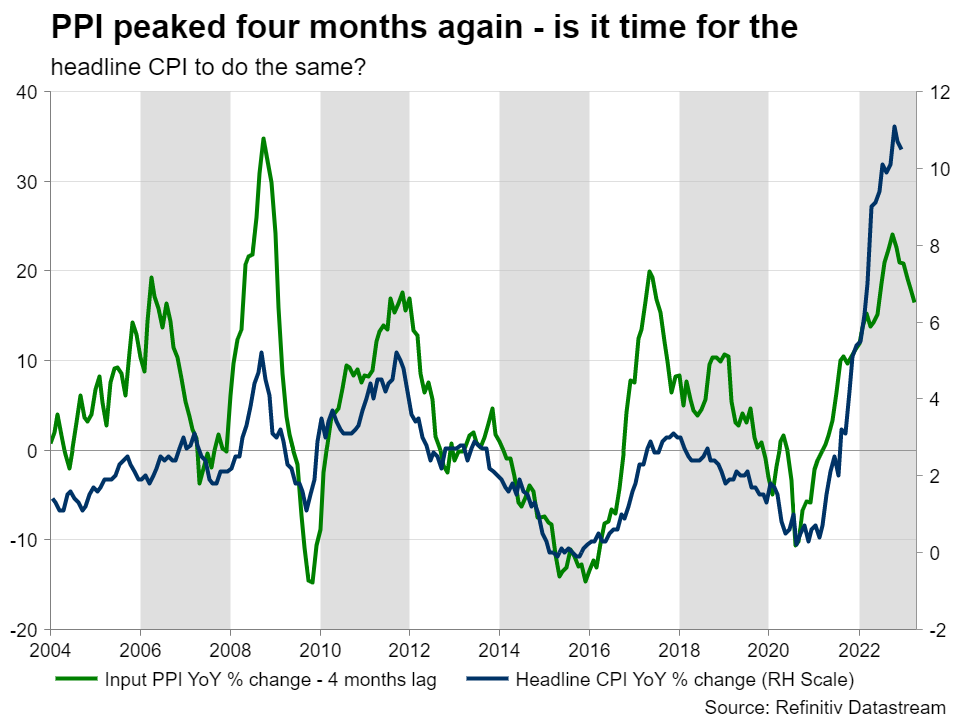

Amidst these developments, the December unemployment rate is seen stable at 3.7% with a monthly employment change of 40k. Additionally, the January CPI print is forecast by the Reuters poll to show a 10.2% year-on-year increase, just a tad lower than the 10.5% change in December. Similarly, the core component of the CPI is seen increasing by 6.2% year-on-year, down from 6.3% in the previous month. These figures are not going to be a pleasant reading for the BoE. Governor Bailey appeared confident at the recent press conference that inflation will continue to fall this year, more rapidly in the second half of 2023, but current evidence is not optimistic. Questions have been raised in government corridors about the BoE strategy going forward, particularly compared to the ECB. The latter is seen by the market hiking more than 100bps by September 2023 while the BoE is expected to make just two more rate hikes, despite the divergence seen in inflation rates lately. The BoE appears to fret about the growth outlook, and thus potentially overlooking its mandate on maintaining monetary stability. Maybe the PPI data, published also on Tuesday, could offer some solace to the bruised BoE. The market tends to ignore this release. However, this seems to have changed lately as the PPI is traditionally seen leading the headline CPI by 4-7 months. Assuming this trend is confirmed again, inflation could potentially surprise on the downside on Tuesday, despite market expectations to the opposite.

Retail sales supported by strong earnings?

Despite the BRC retail sales indicator easing last week, the market is looking for a small improvement at the January retail sales. The gap in the year-on-year figures in the two datasets is expected to be gradually reduced despite the GfK consumer confidence index remaining at record low levels. And this could happen on the back of the increasing average earnings figures. At a year-on-year increase of 6.5%, the average earnings excluding bonuses seem to offer some support to the household facing the strongest inflationary pressures for decades.

Sterling fans look for evidence before another rally

Sterling lovers are trying to find sufficient evidence to stage another rally, potentially continuing on the move recorded since October 2022, despite the recent news flow not supporting their cause. However, the technical picture is showing some early bullish signs. In particular, the stochastic oscillator appears to be suggesting that a bullish divergence is currently developing, as the higher low in the sterling/dollar pair has been met with a lower low in the stochastic. Should this result in a sterling rally, the bulls would love a move up to the 1.2446 area, which twice in the past 60 days has acted as a significant resistance point.