{kind=link}

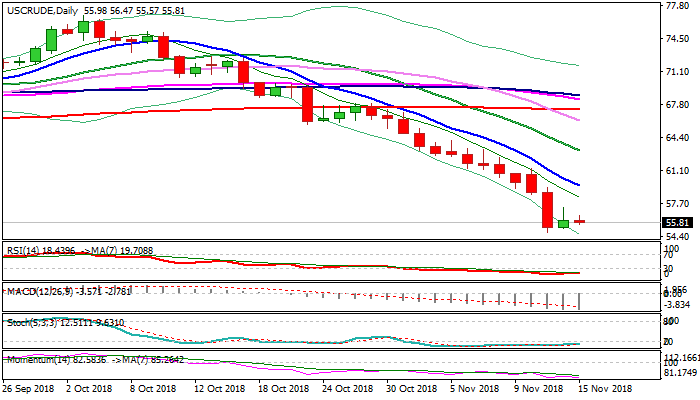

WTI contract registered the first positive daily close in twelve day on Wednesday, signaling that larger bears are taking a breather after steep fall, but recovery looks so far very limited.

Thursday’s daily candle is green but with long upper shadow marked strong upside rejection and weighs on oil price, suggesting that consolidation would be short-lived and dominating bears are likely to re-take full control.

Signs of oversupply in the oil market as the US became the world’s biggest oil producer with record 11.6 million barrels per day, followed by top producers Russia and Saudi Arabia, with no significant impact on global supply from new sanctions on Iran, keep oil prices under strong pressure.

Also, there was no impact from comments that OPEC has a consensus to support the decision to start balancing oil market by cutting production by 1.4 million barrels per day.

Oil needs a catalyst to spark recovery, as the price so far showed no reaction on strongly oversold daily techs, as bears generated another signal on violation of important $55.35 support (Fibo 61.8% of $42.04/$76.88 rally, but weekly close below is needed to confirm signal.

Bears also cracked next significant support at $54.80 (14 Nov 2017 trough), clear break of which would add to negative outlook.

Bearish scenario sees extension of larger downtrend from $76.88 (2018 high) on sustained break below $55.35/$54.80 pivots towards targets at $52.84 (28 Sep 2017 high) and $50.26 / 00 (Fibo 76.4% / psychological support).

On the other side, stronger recovery signal could be expected on bounce through falling 10SMA ($59.52).

Res: 56.47, 57.35, 59.52, 61.27

Sup: 55.57, 55.35, 54.80, 54.00