{kind=link}

Here are the latest developments in global markets:

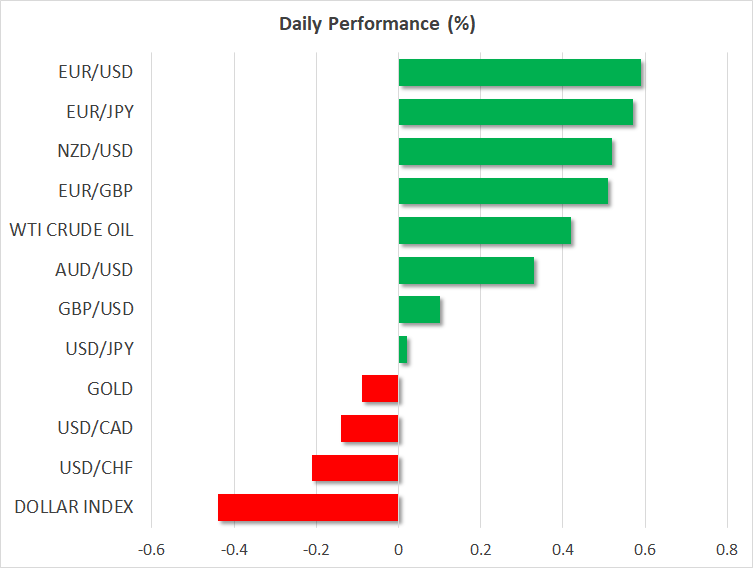

FOREX: The single currency rebounded on Tuesday’s 10-month low near 1.1500 against the greenback (+0.67%) as concerns about Italy’s political crisis remains in focus and there is a chance of new elections taking place on July 29. In data, economic sentiment in the Euro area came in slightly higher than expected in May at 112.5 but below the April’s mark of 112.7. Pound/dollar traded higher by 0.14% to 1.3269 following the 6-month low of 1.3203 that it posted on Tuesday. Dollar/yen rose above its intraday low of 108.34 and entered positive ground (+0.05%) before the announcement of the second estimate of Q1 GDP. The dollar index against a basket of six major currencies headed down by 0.42% following three consecutive green days. The antipodean currencies traded higher, with aussie/dollar up at 0.7534 (+0.40%) and kiwi/dollar climbing to 0.6938 (+0.49%). Dollar/loonie moved lower by 0.19% near 1.3000 ahead of the BOC interest rate decision later in the day. Meanwhile, dollar/Turkish lira plunged by 1.39% to 4.4871.

STOCKS: European equities were in the green at 1130 GMT except the French CAC 40 which eased by 0.09%, set to complete the six straight bearish day. The benchmark European STOXX 600 rose by 0.22% following five red days. The blue-chip Euro STOXX 50 was up by 0.23%, while the German DAX 30 increased by 0.71%. The Spanish IBEX 35 gained 0.93%, while the British FTSE 100 advanced by 0.33%. In the US, even though the S&P, Dow Jones, and the Nasdaq all plunged yesterday, futures tracking these indices are currently in the green, pointing to a higher open today.

COMMODITIES: Oil prices edged up during the European trading session on Wednesday, paring the previous week’s losses but remaining elevated from the six-week low reached on Monday. WTI was up by 0.31% near the $67 handle, while Brent crude jumped by 0.54% to $75.81. In precious metals, gold edged marginally lower by 0.03% as concerns about the political turmoil in Italy and an escalation in the China-US trade conflict failed to lift prices.

Day ahead: Bank of Canada to stand pat on rates; German inflation in focus

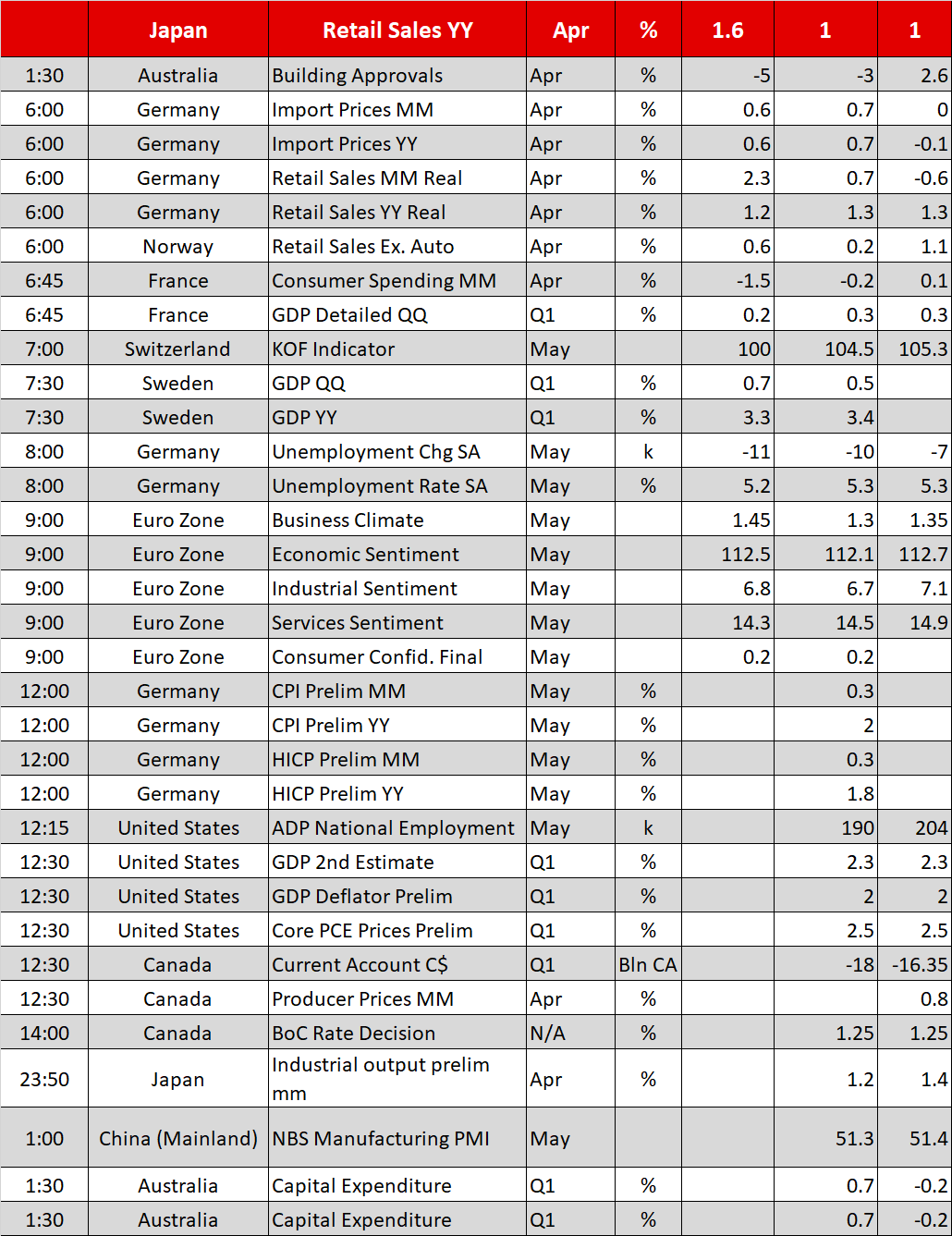

The economic calendar will be busy in terms of data releases later in the day, while a rate decision in Canada and political conditions in Italy will be in the spotlight as well.

At 1200 GMT, Germany, the EU’s largest economy, will publish preliminary readings on inflation for the month of May and forecasts are for the numbers to show an improvement after remaining steady in the past two months. Particularly the headline consumer price index (CPI) is expected to climb from 1.6% to 2.0% y/y, reaching the highest level since February. The harmonized CPI, which is comparable to other EU countries, is seen higher as well, at 1.8% y/y compared to 1.4% in April. In case the data surprise to the upside, investors could turn more optimistic that Thursday’s Eurozone flash inflation figures could also rise, helping the euro to recover.

Yet the political turmoil in Italy could limit any potential gains in the common currency on fears the Italian President Sergio Mattarella could dissolve parliament and call for fresh elections as soon as July 29 in the next couple of days according to sources with knowledge. Recall that over the weekend, Mattarella rejected the choice for the minister of economy proposed by the populists parties, but it is being reported today that these anti-establishment parties, the Five-Star Movement and the League party, were pushing efforts again to form a government.

A few minutes later, at 1215 GMT, the ADP research institute in the US will release its national employment report for the month of May, two days before the government’s famous nonfarm payrolls come into light. The report regarding the US nonfarm private sector is expected to indicate a slowdown in the number of people being employed, with analysts projecting a rise of 190k jobs, less than the 204k increase seen in the previous month. The data could be a good indication of what investors could expect from the government’s nonfarm payrolls,which measures employment changes both in the private and public nonfarm sectors.

Staying in the US, the second estimates on Q1 GDP growth and PCE prices will attract attention at 1230 GMT, with analysts waiting for both measures to confirm their initial estimates: GDP growth to stand at 2.3% on an annualized basis and PCE prices to rise by 2.5% y/y. Traders will also keep a close eye at the Fed’s Beige book which states current economic conditions in 12 Fed districts at 1800 GMT.

Meanwhile in Canada, stats on producer prices and the current account will be available at 1230 GMT, but the Bank of Canada’s monetary policy meeting due at 1400 GMT will be the main headline of the day. Analysts anticipate the central bank to hold interest rates unchanged at 1.25% for the fifth time despite a strong labor market and inflation around the target. Factors such as uncertainties around NAFTA and US trade protectionism in general are likely to keep policymakers cautious, while households’ overloaded debt obligations could also remain a concern. Still, any hawkish messages out of the rate statement following the decision could increase chances for stimulus reduction later this year. Note that the markets are currently pricing in two rate hikes coming in July and December. No press conference or financial projections are scheduled for this meeting.

In oil markets, the American Petroleum Institute will give an insight on US crude stocks for the week ending May 25 at 2030 GMT.

Elsewhere, industrial production figures out of Japan will come under review at 2350 GMT, while early on Thursday, Chinese manufacturing PMI (0100 GMT), New Zealand’s ANZ business confidence (0100 GMT) and Australia’s capital expenditure readings (0130 GMT) will be released.

Any developments on the trade front will be closely watched during the day after China warned the US today it would retaliate if the US was looking to start a trade war. This followed yesterday’s announcements that Washington’s threats of imposing import tariffs on $50 billion Chinese products were still open. Note that the US Commerce Secretary, Wilbur Ross will fly to Beijing this week in an effort to increase US exports to China.

In other economic events, G7 finance and development ministers, as well as central bank governors will meet today on the theme of “investing in growth that works for everyone”. The meeting will end on June 2.