{kind=link}

Here are the latest developments in global markets:

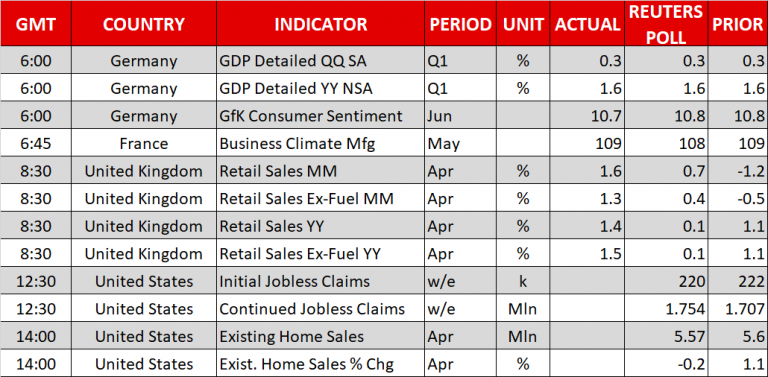

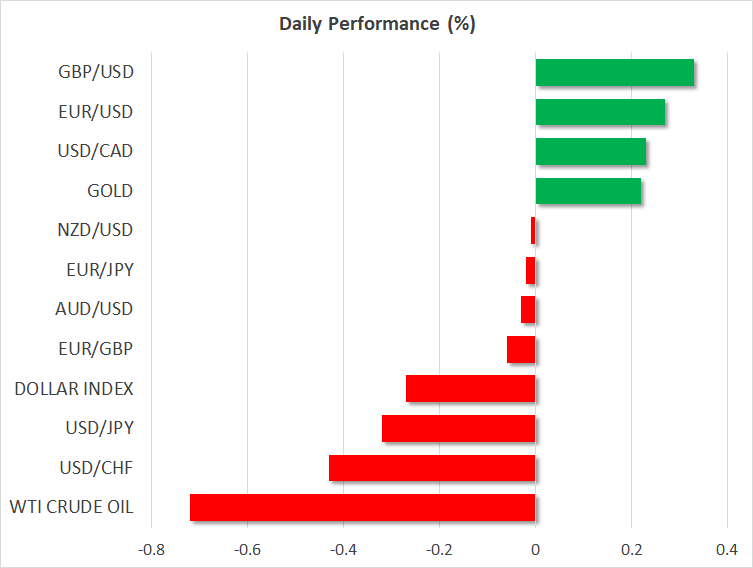

FOREX: The US dollar lost more momentum after the minutes of the Federal Reserve’s last policy meeting were seen as dovish and the US President Donald Trump raised the prospect of new tariffs on imported cars similar to those introduced on steel and aluminum in March. Dollar/yen traded lower by 0.31% on Thursday, posting a 10-day low of 109.32. The US dollar index stepped back to 93.72 from its five-month high (-0.29%). Euro/dollar edged higher by 0.26%, following the pullback on the 6-month low as China signaled its confidence in the euro, ahead of the European Central bank (ECB) minutes later in the day. Pound/dollar advanced by 0.38% to 1.3400 after the bigger-than-expected increase in retail sales by 1.6% m/m in April from 1.1% in March, jumping its most in 1½-years. The Turkish lira plummeted by 2.48% against the greenback today, reversing the strong bullish rally which came after the central bank raised interest rates by 300 basis points on Wednesday. The Antipodeans were again losing some ground versus the greenback. Aussie/dollar was down by 0.05%, while kiwi/dollar moved lower by 0.01%. Moreover, dollar/loonie rose by 0.25% to 1.2858 and continued to move sideways.

STOCKS: In Europe, the majority of the indices had a green day with the British FTSE 100 and the German DAX 30 being the only exceptions. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were both higher by 0.29% at 1100 GMT. In Germany, the DAX eased by 0.05%, while the French CAC 40 rose by 0.39%. In Italy, the FTSE MIB 100 was up by 0.34%, while the British FTSE 100 was weaker by 0.06%. The Spanish IBEX 35 traded higher by 0.48%. Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in positive territory, pointing to a higher open today, continuing the upward movement from last week.

COMMODITIES: Both WTI and Brent crude oil were down by 0.70% and 0.91% respectively on expectations that OPEC members will step up production on supply worries from Venezuela and Iran. West Texas Intermediate crude dived to $71.34, while Brent dropped to $79.07. In precious metals, dollar-denominated gold rose nearly 0.26%, last trading near $1,296.3 per ounce, with the move likely being driven by the tumble in the greenback.

Day ahead: ECB meeting accounts next in focus

After the FOMC meeting minutes emphasized on Wednesday that inflation above 2.0% will not necessarily imply faster rate hikes, ECB meeting accounts will come next under the spotlight on Thursday at 1130 GMT. Recalling that ECB policymakers decided to leave monetary policy unchanged at their last policy meeting on April, acknowledging the slowdown in the EU’s economic performance, investors will be closely watching for clues on how the central bank plans to react to this weakness. Any remarks stating that the softness in data is temporary – as the ECB Chief Mario Draghi recently characterized – and/or the quantitative easing program is set to be phased out by the end of this year, could push the euro higher. However, if the accounts express concerns about the Eurozone’s economic outlook, pointing that the weakness could have stretched into the second quarter, the common currency could face a further sell-off. This could also increase speculation the QE program might extend beyond 2018.

Meanwhile, political developments in Italy are expected to continue to limit gains in the euro. Yesterday, the Italian President, Sergio Mattarella, approved the law professor Giuseppe Conte as the next Prime Minister of the new coalition government as the two Eurosceptic populist parties had proposed. Risks, though, remain on the political agenda and whether the new government will push forward potential fiscal reforms that could breach the EU’s spending rules program.

In the US, the economic calendar features initial jobless claims (1230 GMT) and figures on existing home sales (1400 GMT). Updates on the trade front, though, are likely to attract a greater attention as latest headlines have tempered hopes of progress in US-China trade relations as well as the optimism of a smooth US-North Korea summit on June 12. Particularly, risk-off sentiment strengthened even further after the US President, Donald Trump, admitted yesterday that talks with China need a different structure, twitting “Our trade deal with China is moving along nicely, but in the end we will probably have to use a different structure in that this will be too hard to get done and to verify results after completion”. Moreover, US trade relations with the EU remain in limbo as well, with Washington warning Brussels that exemption from the steel and aluminum import tariffs granted to the EU would not be extended. Trump’s order to probe the US automobile industry yesterday raised fears of new import tariffs. Note that the US is one of the biggest destinations for EU car exports.

In terms of public appearances, at 1235 GMT, comments by Atlanta Fed President Raphael Bostic and Dallas Fed President Robert Kaplan will be in focus. A few minutes later, at 1245 GMT, the Canadian Prime Minister, Justin Trudeau will be speaking on the role of the G7 and the future of the North American Free Trade Agreement, while at 1910 GMT the BoE Governor, Mark Carney will be appearing before the London’s Society of Professional Economists.

In other news, China, the UK, France, Germany, Russia, and Iran are set to meet on Friday to discuss the Iranian nuclear deal.