{kind=link}

Here are the latest developments in global markets:

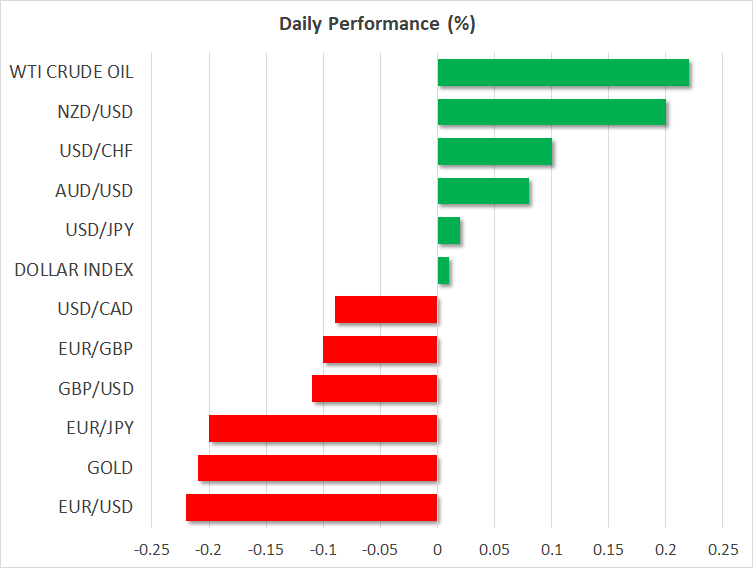

FOREX: The US dollar index, which measures the greenback’s performance against a basket of six major currencies, is trading practically unchanged on Tuesday. It briefly touched its highest levels for 2018 on Monday as trade frictions between the US and China were perceived to be diminishing, though it later gave back all its gains to end the day nearly flat. The euro remains on the back foot overall, as the political situation in Italy continues to cause investors to flee the nation’s bond market.

STOCKS: US markets closed higher on Monday, with risk appetite being supported by news that the US and China have called a truce in their trade war. The Dow Jones led the pack, rising by 1.21%, while the S&P 500 and the Nasdaq Composite climbed by 0.74% and 0.54% respectively. As for today, futures tracking the Dow, S&P, and Nasdaq 100 are all in positive territory, signaling a slightly higher open. In Asia, Japan’s Nikkei 225 and the Topix fell by 0.18% and 0.23% correspondingly. Markets in Hong Kong and South Korea remained closed for public holidays. In Europe, futures tracking the major indices were flashing green, pointing to a higher open today, particularly for the German DAX 30, which also stayed closed yesterday.

COMMODITIES: Oil prices advanced on Monday, with WTI breaking above its recent multi-year highs, while Brent remained slightly below its own peaks. Today, WTI is up by 0.2% while Brent is 0.3% higher. The latest round of gains appears to be owed to diminishing US-China trade tensions, as well as speculation that Venezuela will soon be faced with fresh US sanctions following the re-election of Nicolas Maduro as President. That would further reduce the nation’s already-dwindling oil production. Some comments from US Secretary of State Mike Pompeo on Iran yesterday may have helped the advance in oil too. Pompeo outlined 12 demands for the US sanctions to be lifted, which were quickly rejected by the Iranian President. In precious metals, gold is 0.2% lower today. The safe haven is still trading near the $1290/ounce level, where it has remained stuck for a week now, showing little response to developments on the trade or geopolitical fronts.

Major movers: Dollar index corrects lower after touching fresh highs; Italian politics at the fore

Major movers: Dollar index corrects lower after touching fresh highs; Italian politics at the fore

The dollar index touched another fresh high for 2018 on Monday in the aftermath of the “ceasefire” in the US-China trade war, though it later pared its gains to finish the day nearly unchanged. That said, the greenback did manage to sustain some gains versus the Japanese yen and the British pound. Sterling is set for a very turbulent week, as a raft of crucial economic data and remarks from BoE officials could “make or break” expectations around a potential rate increase at the August meeting, something futures markets currently assign a 40% probability to.

News flow was relatively light yesterday. The most noteworthy developments were seen on the Italian front, where Giuseppe Conte was proposed to become Prime Minister of the Five-Star/League coalition government. Regardless, investors continue to pour out of the Italian bond market, with the yield on the Italian 10-year benchmark having surged nearly 60bps this month to touch its highest level since March 2017 yesterday.

This likely reflects anxiety around the new government’s proposed spending policies, and the increasing possibility of a standoff with Brussels over EU fiscal rules. Indeed, ratings agency Fitch warned yesterday that the coalition poses risks to Italy’s credit profile. Euro/dollar touched a fresh low for 2018, as the heightened political uncertainty in Italy pressured the euro, while the dollar continued to draw support from elevated US bond yields.

Turning to the commodity currencies, dollar/loonie plunged to give back all the gains it posted on Friday. While there was no clear catalyst behind the loonie’s rebound, it may have been aided by the surge in oil prices – Canada being a major oil exporter. Meanwhile, kiwi/dollar and aussie/dollar are up by 0.2% and 0.1% respectively today, both pairs trying to stage modest comebacks following severe declines over the past month.

Day ahead: BoE Governor Carney to testify on inflation

Early in the European session, Bank of England’s Governor, Mark Carney, as well as the Deputy Governor of Markets and Banking Dave Ramsden and the members of the Monetary Policy Committee, Gertjan Vlieghe and Michael Saunders, are scheduled to testify on inflation and economic outlook before the Treasury Select Committee at 0900 GMT. A flow of disappointing economic releases in the past couple of weeks persuaded policymakers to keep interest rates unchanged at their policy meeting on May 10, with markets currently pricing in a 40% chance of a rate hike coming in August. Should policymakers use a cautious tone, spurring fresh doubts on whether or when the central bank will move on with its stimulus reduction plans, the pound could lose more ground against its major peers.

An hour later, at 1000 GMT, British industrial trends for the month of May as measured by the Confederation of British Industry (CBI) are expected to bring further volatility to the pound. The currency could find support on the data should the numbers surprise to the upside, indicating a better outlook for the UK manufacturing sector at times when the government is pushing efforts to achieve a better Brexit deal to avoid disruptions in business activities.

Meanwhile, in Canada, wholesale sales for March will be under review at 1230 GMT, with analysts anticipating the measure to rebound by 0.8% m/m after falling by an equivalent percentage in February.

In oil markets, the American Petroleum Institute is due to publish its weekly report on US crude oil stocks at 2130 GMT and it would be interesting to see whether oil prices could reach fresh peaks today in case the numbers show a decline in crude stocks in the week ending May 18.

On the trade front, any updates regarding US-China relations could attract attention as both countries have recently decided to keep trade war “on hold” and continue negotiations. Ongoing Brexit talks could be in focus as well.

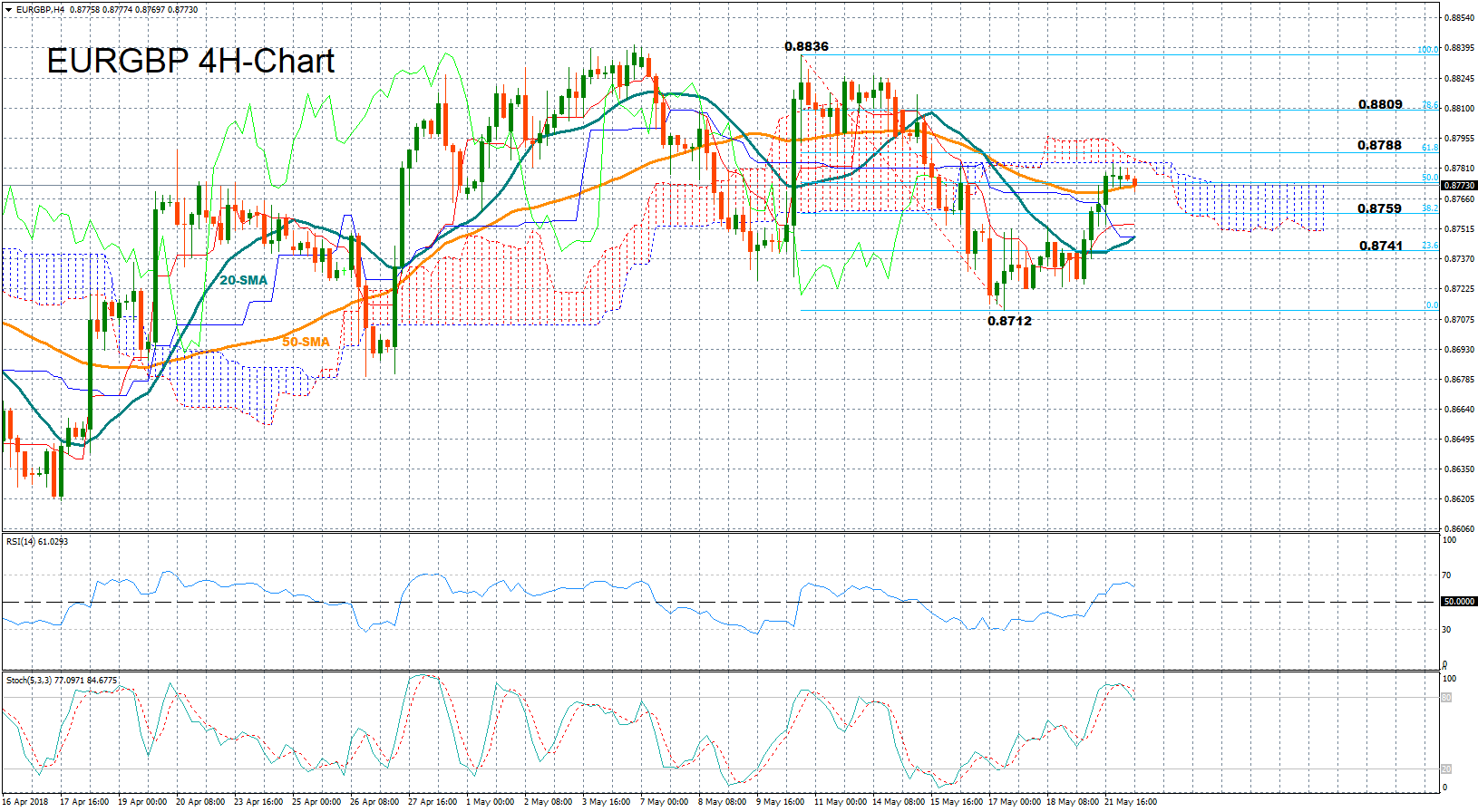

Technical Analysis: EURGBP positive momentum could slow down in short-term

EURGBP has paused its pickup from three-week lows slightly above the 50% Fibonacci of the downleg from 0.8836 to 0.8712, with the RSI and Stochastics supporting that positive momentum could slow down in the short-term as the former is currently changing direction to the downside and the latter is moving downwards to exit overbought territory.

Should the price decline in the wake of the BoE policymakers’ testimonies before the UK Treasury Committee, immediate support could be found at the 38.2% Fibonacci of 0.8759 of the downleg from 0.8836 to 0.8712. Steeper declines could also test the area around the 23.6% Fibonacci of 0.8741 where the 20-period simple moving average is currently placed. If this level fails to hold as well, then the door could open for the three-week low of 0.8712.

Alternatively, disappointing views on the UK economy could strengthen the pair, with resistance probably coming first at the 61.8% Fibonacci of 0.8788 before the focus shifts to the 78.6% fibo of 0.8809.