{kind=link}

Here are the latest developments in global markets:

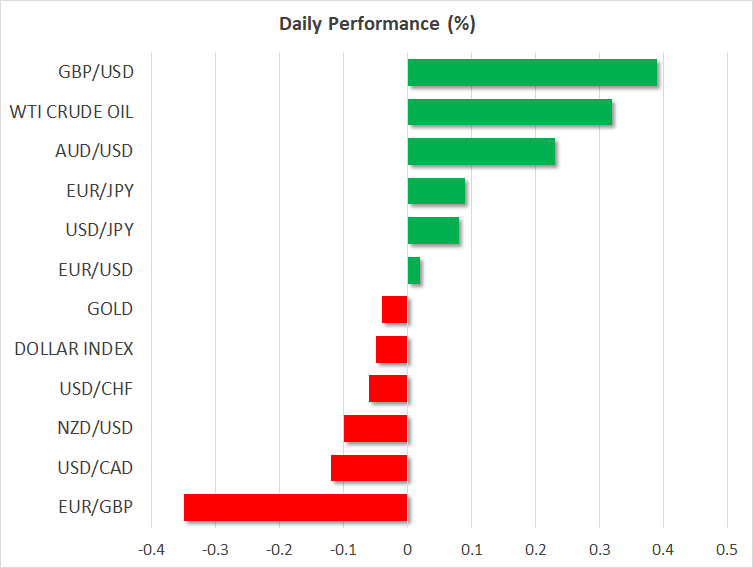

FOREX: The US dollar index is lower on Thursday, albeit by less than 0.1%, still hovering near the five-month highs reached earlier in the week. The US currency barely rose yesterday even though the yields on longer-term US Treasuries continued to climb, reaching fresh multi-year highs. Elsewhere, sterling jumped today after a media report on Brexit suggested the UK is willing to make concessions to avoid a hard border in Ireland.

STOCKS: Wall Street closed higher yesterday, even despite a continued climb in US Treasury yields, a factor that has been limiting advances in stocks recently. The Nasdaq Composite climbed 0.63%, while the S&P 500 and the Dow Jones rose by 0.41% and 0.25% respectively. The gains come ahead of a meeting today between China’s Vice Premier Liu He and key US officials including Treasury Secretary Mnuchin in Washington. The topic will be trade issues, and any relevant comments could well impact US equities today. Futures tracking the Dow, S&P, and Nasdaq 100 are all flashing red, pointing to a lower open. In Asia, Japan’s Nikkei 225 and the Topix rose by 0.53% and 0.45% correspondingly, though in Hong Kong the Hang Seng fell by 0.44%, even though tech giant Tencent (+5.2%) reported strong earnings. In Europe, futures tracking the major indices were all close to neutral levels, with the exception being Italy’s FTSE MIB, which is expected to open much higher.

COMMODITIES: Oil prices were higher on Thursday, extending gains from yesterday. WTI and Brent crude are up by 0.3% and 0.2% respectively, both hovering near multi-year highs. The trigger for the latest leg higher was a surprisingly large drawdown in the weekly EIA crude inventory data released yesterday. More broadly, recent media reports suggest that Saudi Arabia believes the spike in prices is driven by speculation and that this is not ground for producers to boost output, playing down expectations the Kingdom may raise its production to offset any shortage left by Iran. In precious metals, gold is lower today but by less than 0.1%, currently trading near the $1,289/ounce mark.

Major movers: Pound bounces on Brexit news; euro under pressure; dollar stalls

The British pound rebounded overnight, gaining 0.4% versus the dollar, following a media report suggesting the UK government has agreed on a fallback position as a last-ditch effort to avoid a “hard” Irish border. The UK is prepared to remain in the EU customs union beyond 2021 to ensure frictionless trade on the Irish border. This has been one of the main issues that have been hindering progress in the Brexit negotiations and hence, signals that the worse case scenario of a hard border may be avoided likely reignited speculation the talks may finally move forward.

With little in the way of UK data releases until next week, pound crosses may continue to be driven by updates on the Brexit front. Any fresh signs that the UK administration is willing to make some concessions for the talks to progress may provide some much-needed support to the pound, which is still licking its wounds following the BoE’s cautious stance last week.

In euro land, the common currency remained under selling pressure yesterday amid reports that an incoming anti-establishment coalition government in Italy would seek to write-off as much as €250 billion of Italian debt. This sent shivers through the Italian debt market, triggering a flight out of Italian bonds and pressuring the euro. That said, these reports were subsequently denied by one of the two political parties, helping the euro to recover some of its losses.

Over in the US, the dollar index stalled yesterday, ending the day only marginally higher even though the yields on 10-year US Treasuries continued to climb, reaching a fresh seven-year high of 3.12% today. The continued advance in US bond yields has been one of the major factors supporting the greenback lately.

In Canada, the loonie surged following some comments from the nation’s Finance Minister Bill Morneau. He stoked expectations that a severely-delayed oil pipeline may be completed sooner rather than later, making it easier to export Canadian oil.

Day ahead: Light calendar day with US jobless claims due; updates on Brexit, Italian political situation eyed

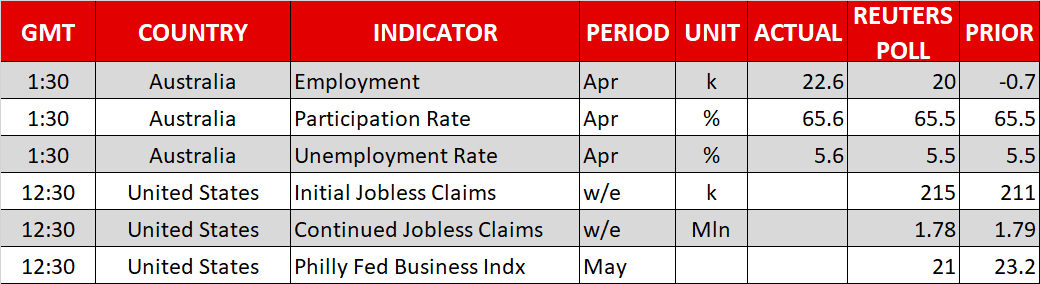

Thursday’s calendar doesn’t feature much in terms of releases to get traders excited. In the absence of important data, the attention is expected to fall on developments revolving around Brexit and Italian politics.

At 1230 GMT, weekly jobless claims data will be made public out of the US, while the Philly Fed Business index pertaining to the month of May will also be hitting the markets at the same time.

A report by the Telegraph saying that Britain will tell Brussels it is prepared to stay in the EU’s customs union beyond 2021 boosted sterling. In this respect, a meeting between UK PM Theresa May and European Council President Donald Tusk taking place today will be of interest.

The euro is coming under pressure on the back of Italian political uncertainty and the implications an anti-establishment government by the 5-Star Movement and (Northern) League parties will have for the euro area. The story will be closely watched as it is expected to be the major driver in euro pairs, at least in the short term.

Retail giant Walmart will be releasing its quarterly results before today’s opening bell on Wall Street. The direction in Treasury yields will also be eyed as it has implications for equity markets; higher yields render bonds relatively more attractive compared to stocks.

Outgoing ECB Vice President Vitor Constancio will be delivering the opening address at the third annual ECB macroprudential policy and research conference at 1200 GMT – Cleveland Fed President Loretta Mester will be speaking on monetary policy at the same venue. Regional Fed Presidents Neel Kashkari and Robert Kaplan will also be making appearances at 1445 GMT and 1730 GMT respectively; neither holds voting rights within the FOMC in 2018.

Another meeting that could generate attention on Thursday is the one between US President Donald Trump and NATO Secretary General Jens Stoltenberg, while one should also keep in mind that US-China trade talks and deliberations for a North Korea-US summit remain on the background.

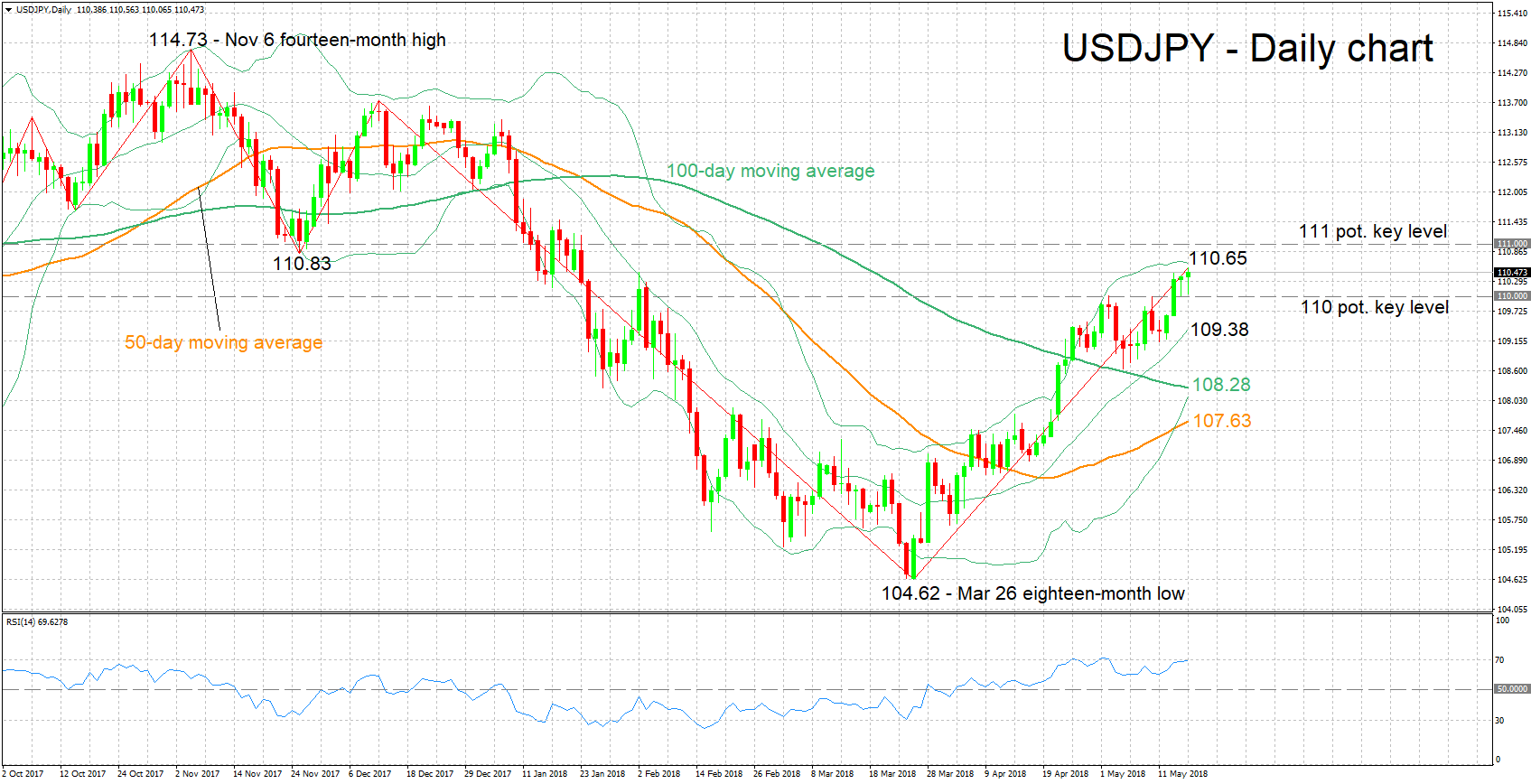

Technical Analysis: USDJPY touches 4-month high, short-term bullish

USDJPY has advanced considerably after touching an 18-month low of 104.62 in late March. Earlier on Thursday, it reached a four-month high of 110.56. The rising RSI is serving as a testament to the bullish short-term momentum that is in place. Notice though as well that the indicator is close to the 70 overbought level.

Should the US-Japanese yield differential continue to climb in the US’ favor, then the pair is likely to add to gains. The upper Bollinger band at 110.65 may be offering immediate resistance, with the 111 round figure being eyed next in case of stronger gains.

On the downside and in case of falling US Treasury yields, USDJPY may ease a bit. Support to declines may come around the 110 handle, and further below from the middle Bollinger line – a 20-day moving average line – at 109.38.

Although today’s US releases are not typically major market movers, the pair may still some positioning upon the release of the numbers.