{kind=link}

Is a Rate Hold Nailed On Or Are Markets Positioned For a Shock?

The Bank of England meets on Thursday and, despite spending months preparing markets for a rate hike, the central bank is widely expected to leave them on hold at 0.5%.

While markets don’t always get fully on board with central bank efforts to prepare markets for a tightening of monetary policy – as the US Federal Reserve found in the early days of its cycle – I think the two are actually closely aligned on this particular occasion.

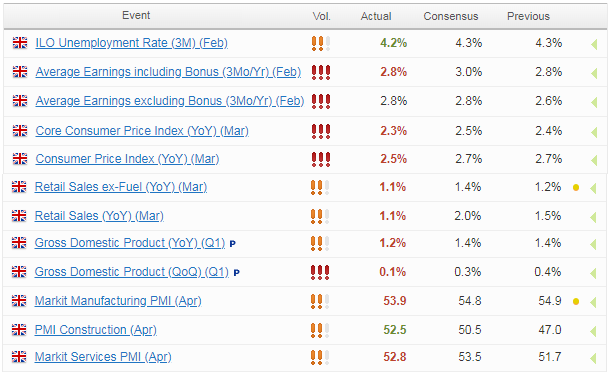

UK data casts doubt over a rate hike

Carney’s change of tune prompts significant drop in expectations

Market reaction could be huge if BoE follows through on previous warnings

The economic data from the UK over the last month or so has been underwhelming at best and another drop off in the inflation readings has afforded the Monetary Policy Committee the space to take a little more time rather than rush into raising rates.

While much of the weak data could be attributed to the “Beast from the East”, the weaker PMI surveys and the fact that inflation is now only just above target after peaking above 3% in November gives the central bank little reason to raise interest rates, particularly against such an uncertain backdrop.

Brexit poses many risks for the UK economy and with less than a year to go until the country leaves the EU – meaning we should have more clarity on the outlook later this year – there seems little to be gained in rushing to raise interest rates when it may have to be reversed shortly after.

It’s not just the data that has cast doubt on a rate hike on Thursday – the implied probability has fallen from around 70% a few weeks ago to only 13% now – Governor Mark Carney didn’t want to get drawn on the timing of the next rate hike on 19 April, stressing he’s conscious that there are other meetings over the course of the year, an apparent hint that May is no longer the certainty it was.

GBP/USD – British Pound Steady, Markets Expect BoE to Stand Pat

What is clear is that there is no real unanimous view on the correct timing for rate hikes on the MPC which should make the votes very interesting on Thursday. Ian McCafferty and Michael Saunders will likely stick with their gut in voting for a hike – especially if the latter’s recent comments are anything to go by – but the question is whether the new forecasts will be enough to persuade others to follow.

The new economic forecasts will also be key in shaping the view on future rates hikes, as will the comments of Carney and his colleagues in the press conference shortly after which should make for a very interesting day for sterling, UK bonds and the FTSE. The pound has fallen more than 5% against the dollar over the last weeks as expectations of a hike have collapsed.

While Thursday looks a foregone conclusion, the BoE could still spring a surprise on the markets having previously laid the groundwork for such a move. If they do, the market reaction would likely be quite huge.