{kind=link}

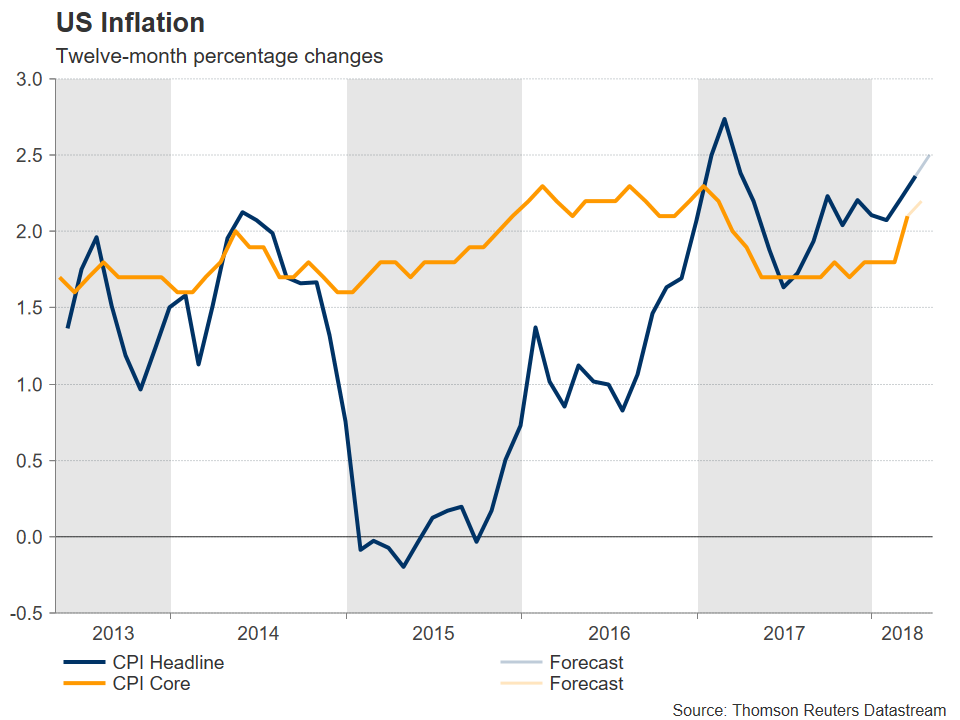

The US will see the release of inflation figures on Thursday at 1230 GMT. Price pressures are forecast to have accelerated in April, with headline CPI projected to touch its highest since February 2017 on an annual basis. The numbers do not pertain to the Federal Reserve’s preferred inflation measure, but still they will be closely watched by market participants; a beat could stoke market expectations for the delivery of four interest rate increases in total by the US central bank in 2018, providing support to the greenback.

Headline inflation is expected to expand by 0.3% m/m, after contracting by 0.1% in March, and grow by 2.5% y/y, above March’s 2.4% and at its highest in fourteen months. Rising oil prices are anticipated to be a factor contributing to the uptick in headline CPI. Meanwhile, core CPI, the measure that excludes volatile food and energy items, is projected to grow by 2.2% – a feat last achieved in February of last year – following March’s 2.1%.

FOMC policymakers might be willing to accept inflation overshooting past their annual target without steepening their interest rate outlook, or at least this was the market’s interpretation upon completion of last week’s meeting by the Fed; something which was also echoed by Atlanta Fed President Raphael Bostic (a voting member within the FOMC in 2018) in remarks made on Monday. This development led market participants to scale down their expectations for three additional 25bps interest rate increases during the year, something which would put the total number of moves in 2018 at four. However, the odds for a third additional increase are back on the rise according to Fed fund futures, currently standing at 30%. Stronger-than-forecasted readings out on Thursday could well push that probability even higher, consequently boosting the US currency.

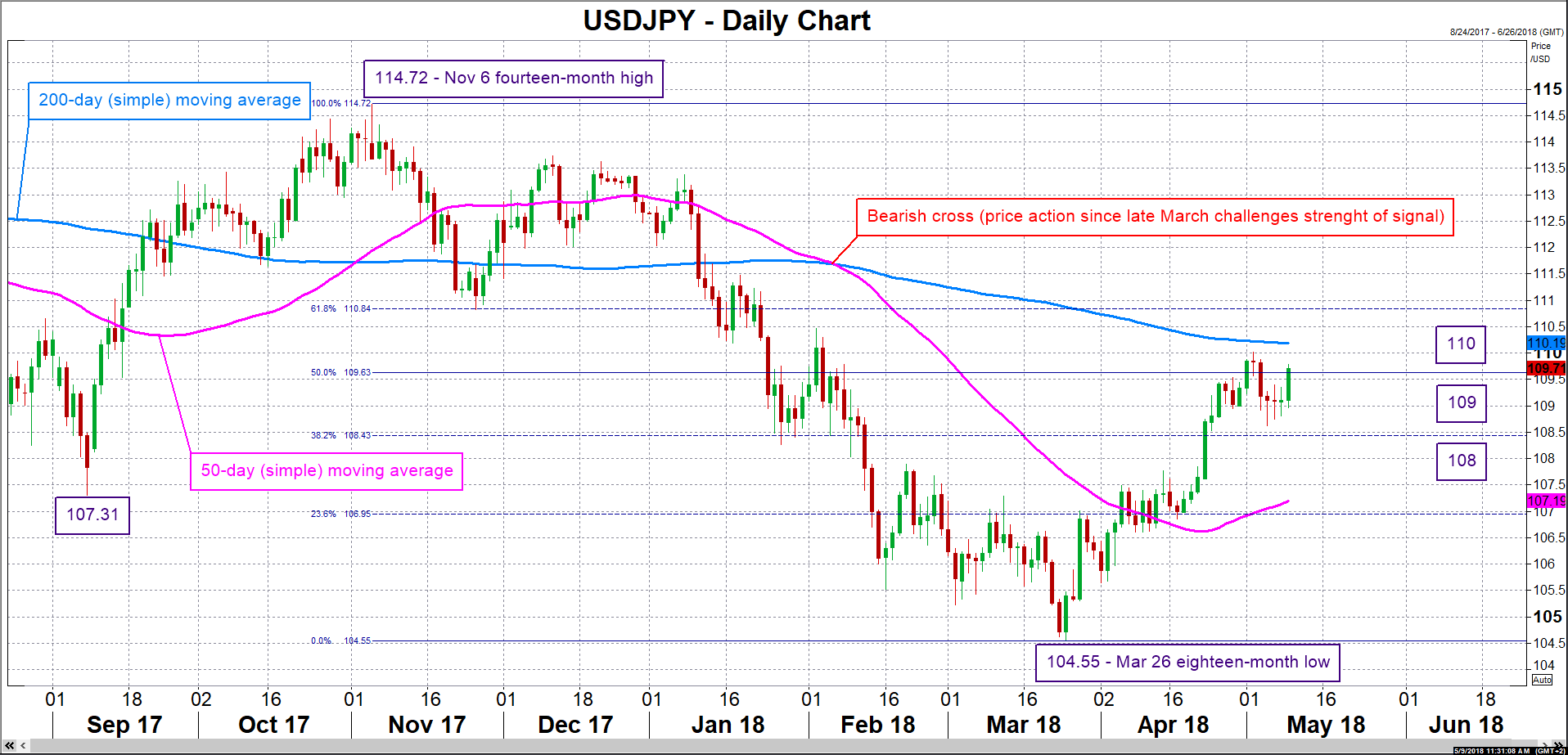

Focusing on dollar/yen, resistance to advances in the event of a positive surprise in the numbers might come around the 110 handle, given that first the area around the 50% Fibonacci retracement level of the November 6 to March 26 downleg at 109.63 is more conclusively broken. The region around 110 includes the current level of the 200-day moving average at 110.19, as well as last week’s three-month high of 110.02. Further above, the range around the 61.8% Fibonacci mark at 110.84 would be eyed next. Conversely, a data miss would likely exert selling pressure in USDJPY. Support to declines could come around the 109 round figure and, in case of sharper losses, from the area around the 38.2% Fibonacci level at 108.43.

Prints on April factory price inflation, as gauged by the producer price index (PPI), will be made public on Wednesday (1230 GMT). These too can spur positioning on dollar pairs, including of course the aforementioned (USDJPY). Important data out of Japan, will include March’s current account balance due during Thursday’s Asian session. However, it should be kept in mind that developments on the geopolitical front might turn out to be another driver of movements in the dollar/yen pair this week, especially in light of the Japanese currency’s safe-haven status. In this respect, yesterday, President Trump decided to withdraw the US from the 2015 nuclear deal with Iran.