{kind=link}

The US dollar rally continues to gather steam as it appreciated against major pairs for a third week. The U.S. non farm payrolls (NFP) provided little support with a miss in both the headline job number and the much anticipated wage growth component. The main takeaway from the jobs report was the drop in the employment rate from 4.1 percent last month to 3.9 percent. The greenback keeps plowing forward as monetary policy divergence is expected to be wider between the Fed and other central banks. The Reserve Bank of New Zealand (RBNZ) and the Bank of England (BoE) will feature this week and both are expected to keep rates unchanged. Although there are some economists that are still holding on to a possible rate hike in May by the BoE.

- BoE to host Super Thursday with a potential rate hike in the cards

- US inflation expected to rise by 0.3 percent

- Canada to add 20,000 jobs

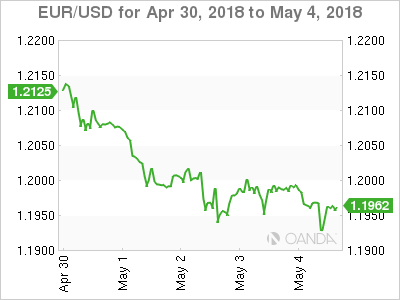

Dollar Soldiers On Despite US Jobs Miss

The EUR/USD lost 1.37 percent in the last week. The single currency is trading at 1.1960 after a week heavy with economic released and the release of the U.S. Federal Reserve’s rate statement. European data continues to disappoint with German retail sales shrinking by 0.6 percent and the flash inflation estimate coming short of the forecast at 1.2 percent the biggest drags on the euro. Indicators in the US were not as solid as the previous week with a disappointing ISM non manufacturing PMI and less jobs added in April that was expected.

Growth expectations in the United States remain strong, while concerns are rapidly rising in Europe given the string of soft data. The U.S. Federal Reserve is expected to hike rates 2 or 3 more times this year and with inflationary pressures the third rate hike becomes more tangible. The Fed did hold, and gave little hints of what comes next, but the market has already priced in a 25 basis points in June. In contrast the European Central Bank (ECB) has given few details on what it will do when its quantitative easing program ends in September. The gap between growth and interest rates between the US and the Europe will continue to pressure the EUR next week as several prominent members of the Federal Open Market Committee (FOMC) are scheduled to speak.

The USD continues its impressive run and is defying investor expectations. While shorting the USD became a popular trade at the beginning of the year the unwinding of those positions have also helped the USD appreciate further. The Fed under Powell has kept on the same course set by previous Fed Chair Janet Yellen. The two inflation gauges to be released during the week: Producer Price Index (PPI) on Wednesday, May 9 at 8:30 am EDT and Consumer Price Index (CPI) on Thursday, May 10 at 8:30 am EDT are expected to keep inflationary pressures going and be a positive for USD bulls.

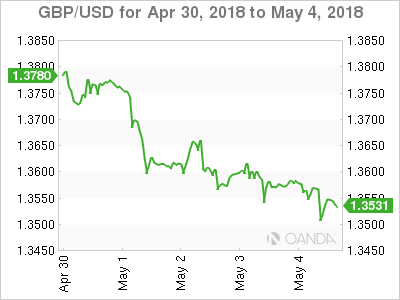

Pound Lower Ahead of BoE Rate Statement

The GBP/USD lost 1.67 percent in the last five days. The currency pair is trading at 1.3545 awaiting the BoE’s Super Thursday. The market was pricing in a rate hike in May after the March monetary policy meeting given that there were two dissenters in the final vote to keep rates unchanged. Economic indicators have soured since then and even Bank of England (BoE) Governor has tried to lessen expectations ahead of the the release of the rate statement, the quarterly inflation forecast, the rate vote count, so called Super Thursday for the amount of information hitting markets at the same time.

GDP data in late April was a heavy blow for rate hikes expectations with a paltry 0.1 percent gain, but hope was still alive given the role weather had to play in curtailing growth in the quarter. A leading indicator such as the Purchasing Manager Indices for construction, manufacturing and services almost took the rate hike off the table as only construction was able to beat the forecast.

The massive data releases out of the BoE will be preceded by the release of manufacturing production data and the Goods trade balance at 4:30 am EDT. The economic slowdown in the UK has reduced rate hike expectations as the central bank awaits more positive data before lifting borrowing costs.

Investors will be focusing on what previous dissenters do. If the two votes remain to hike rates with the possibility of more members joining them, or if the central bank shows a unanimous vote to keep rates unchanged.

Market events to watch this week:

Monday, May 7

- 9:30pm AUD Retail Sales m/m

- 11:00pm NZD Inflation Expectations q/q

Tuesday, May 8

- 3:15am USD Fed Chair Powell Speaks

- 5:30am AUD Annual Budget Release

Wednesday, May 9

- 8:30am USD PPI m/m

- 10:30am USD Crude Oil Inventories

- 5:00pm NZD Official Cash Rate

- 5:00pm NZD RBNZ Monetary Policy Statement

- 6:00pm NZD RBNZ Press Conference

- 9:10pm NZD RBNZ Gov Orr Speaks

Thursday, May 10

- 4:30am GBP Manufacturing Production m/m

- 7:00am GBP BOE Inflation Report

- 7:00am GBP MPC Official Bank Rate Votes

- 7:00am GBP Monetary Policy Summary

- 7:00am GBP Official Bank Rate

- 8:30am USD CPI m/m

Friday, May 11

- 8:30am CAD Employment Change

- 9:15am EUR ECB President Draghi Speaks

*All times EDT