{kind=link}

Here are the latest developments in global markets:

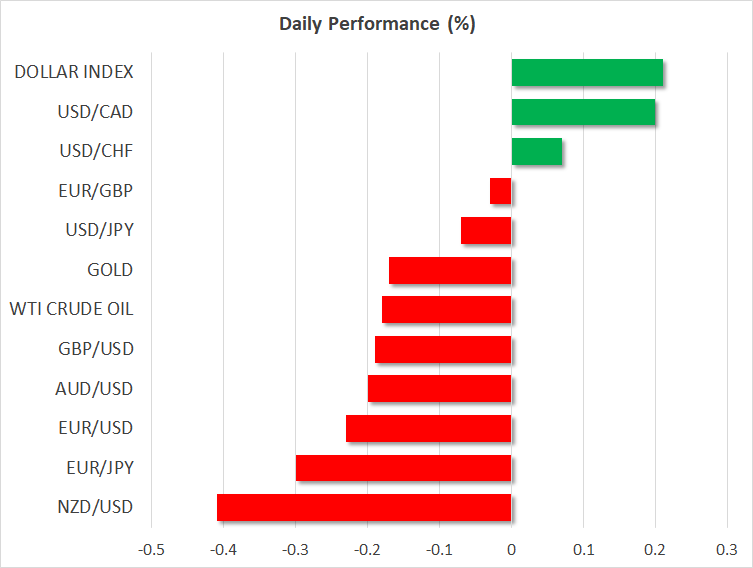

FOREX: The dollar index, which gauges the greenback’s strength versus six major currencies, edged higher by 0.20% during the European session to 92.55, approaching the four-month high of 92.63 reached on Wednesday. Euro/dollar remained under selling pressure after Eurozone’s retail sales and final services PMI figures were weaker than expected, slipping by 0.23%. Meanwhile, dollar/yen retreated to 109.05 (-0.08%), with the focus remaining on whether US jobs data will provide the spark for another push higher. Pound/dollar touched an almost four-month low on Thursday at 1.3537 and was still trading negative today by 0.15% as traders remained skeptical of whether the BoE will deliver a rate hike in May. The antipodean currencies headed lower, with aussie/dollar erasing earlier gains and kiwi/dollar falling, towards 0.7516 (-0.19%) and 0.7010 (-0.41%) respectively. Dollar/loonie was moving sideways around 1.2872. Elsewhere, the Turkish lira weakened to a fresh record low versus the greenback. Dollar/lira advanced by 1.74% to 4.2852, after briefly touching a new high of 4.2894.

STOCKS: European stocks gained some ground overall despite a decline in Asian markets as investors assessed trade talks between the US and China. The benchmark European STOXX 600 rose by 0.25%, while the blue-chip Euro STOXX 50 was down by 0.03%. The German DAX 30 moved higher by 0.30%, the French CAC 40 dived by 0.20%, the Spanish IBEX 35 edged up by 0.15% and the British FTSE 100 advanced by 0.51%. In the US, futures tracking the S&P 500, Dow Jones, and Nasdaq 100 are currently in the red – pointing to a lower open today – albeit only marginally so.

COMMODITIES: Oil prices eased today as the market awaited news from Washington on possible new US sanctions against Iran. West Texas Intermediate crude fell by 0.20% to $68.29 a barrel and Brent declined by 0.22% to $73.46 a barrel. Gold turned negative on a firmer dollar, dropping by 0.14%, while investors turned their focus on the US jobs data later in the day.

Day ahead: US employment report to dominate attention

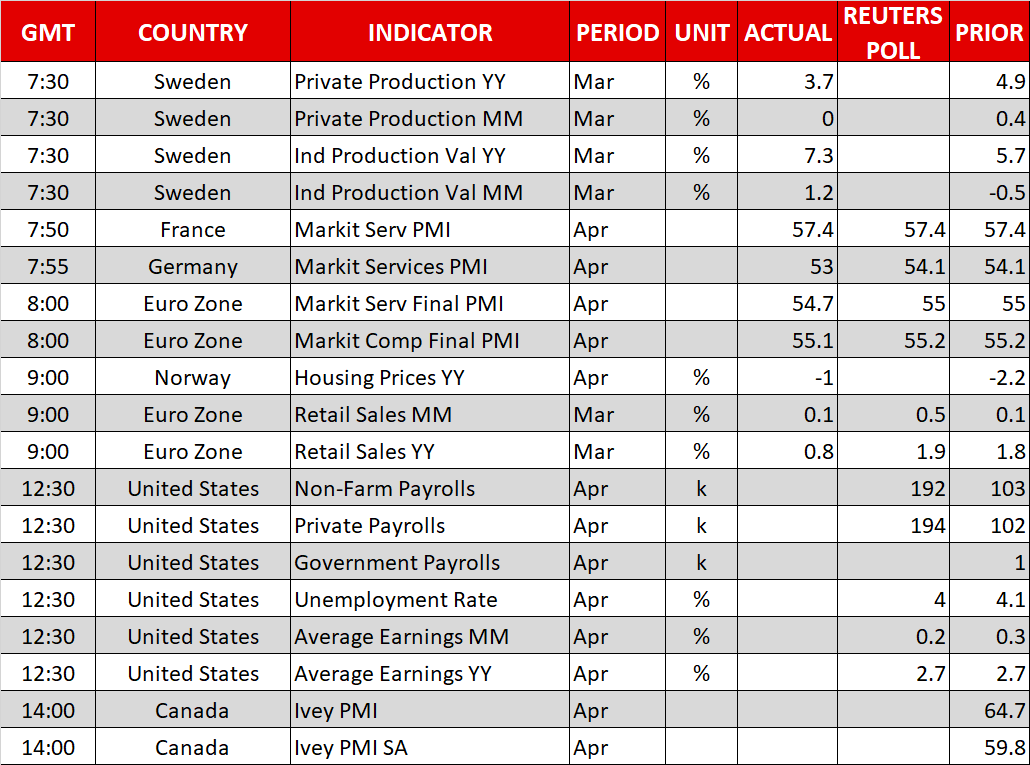

The main event today will be the release of the US employment report for April, at 1230 GMT. Nonfarm payrolls are expected to have risen by 192k, much higher than the 103k recorded in March. Meanwhile, the unemployment rate is projected to tick down to 4.0%, from 4.1% in the previous month. As for the all-important average hourly earnings, the forecast is for the monthly rate to have slipped to 0.2%, from 0.3% previously, which would keep the yearly rate unchanged at 2.7%.

As has been the case with recent jobs reports, attention is likely to fall mainly on earnings. Payrolls and the unemployment are of course very important, but a strong set of numbers on that front would simply confirm what investors already know; that employment growth remains strong. On the other hand, wage growth is the missing piece of the puzzle for the Fed. It has not picked up in a meaningful way despite a tight labor market, confounding policymakers that expect rising wages to push up inflation. Accelerating wages would signal higher inflation down the road, sparking bets for a more hawkish Fed, and vice versa. Therefore, the dollar is likely to move in tandem with any surprise in earnings today; higher in case of a beat, and lower should they disappoint.

US stock markets are likely to be affected by the jobs data as well. Expectations for higher interest rates typically spell bad news for equity indices, while anything that suggests rates may stay low for longer is usually positive. Thus, should strong data spark bets for a more hawkish Fed, then equities are likely to experience declines, whereas a disappointment in the figures could lead to a move higher.

Elsewhere, Canada’s Ivey PMI for April will be in focus at 1400 GMT.

In energy markets, the Baker Hughes oil rig count at 1700 GMT should provide a fresh indication of whether US production continues to soar.

As for the speakers, the New York and San Francisco Fed Presidents, William Dudley and John Williams, will deliver remarks at 1445 and 1730 GMT respectively. A few hours later at 2130 GMT, Fed Board Governor Randal Quarles will step up to the rostrum. All these officials are voting members of the FOMC this year, so their comments will be closely watched. This may be especially true in the case of John Williams, who will be replacing Dudley as the influential head of the New York Fed soon.