{kind=link}

The US dollar is lower against major pairs on Thursday, but still holds considerable gains in weekly measures. The Fed held rates unchanged on Wednesday and its statement hinted at gradual tightening. The usually steady U.S. non farm payrolls (NFP) report has been inconsistent throwing strong wage growth alongside weak numbers. The April NFP report will be published on Friday, May 4 at 8:30 am EDT. Forecasters expect a rebound in the number of positions added, but a lower wage gain as well.

- NFP expected to show 190,000 job gain

- US wages to slow down with 0.2% rise

- Inflation key in Fed deciding between 2 or 3 additional rate lifts

Fed Holds Rate with Minimal Changes in Language

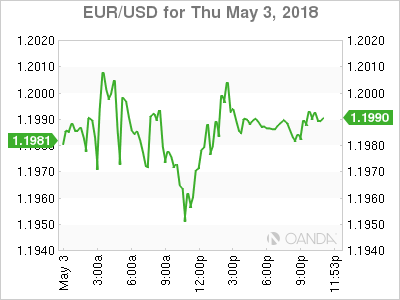

The EUR/USD rose 0.40 percent on Thursday. The single currency is trading at 1.1999 after investors booked their USD gains after the Fed wrapped up its two day meeting on Wednesday. The central bank held rates at 1.50–1.75 percent but according to the CME’s FedWatch tool is close to a 100 percent probability of a 25 basis points hike in June.

Economists forecast the NFP to have strong headline numbers recovering from weather factors that impacted March’s report, but the devil will be in the inflation details. Employment has been a strong pillar of the US recovery, but wages have lagged behind. The more dovish members of the Fed make a point to cite the lack of inflationary pressure when they point to their more hawkish colleagues. Higher wages would validate the Fed’s plans for 3 or 4 rate hikes this year.

The Fed has hinted through rhetoric that if growth keeps up 3 more rate lifts would be needed. The market had already priced in 3 this year, so the fourth bump in borrowing costs has given the US dollar a boost in April.

The US central bank stands alone amongst major monetary policy bodies. The European Central Bank (ECB) is due to end its QE program but it has delayed as much as possible discussing the exact measures it will take when the program runs down in September. In May the ECB opted to leave its benchmark rate intact and made no announcements regarding the end of the quantitative easing program. ECB President Mario Draghi was neither hawkish nor dovish, which resulted in little support for the euro. The eyes of the market will now be fixed in the June and July meetings for some insights into the plans of the central bank.

Inflation data out of Europe released today will make matters tougher on the ECB. Missing the forecast at 1.2 percent in an annual basis (the expectations were for a 1.3 percent gain) is another disappointing economic indicator for the EU.

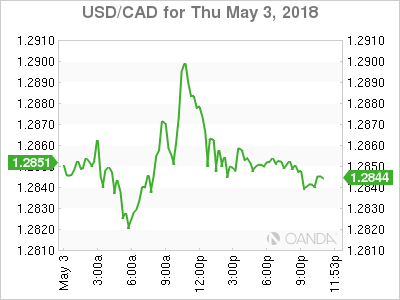

Loonie Rises Despite Record Trade Deficit

The USD/CAD lost 0.21 percent in the last 24 hours. The currency pair is trading at 1.2856 as the loonie gets some traction against the USD despite Canada’s trade deficit surging to a $4.14 billion record. US jobs will be the main focus for investors on Friday as the Canadian employment report will be released 7 days from tomorrow.

The Bank of Canada (BoC) governor Stephen Poloz said earlier this week that Canadian households are $2 trillion in debt with 50 percent of that in mortgages. The high level of debt has the central bank concerns about the impact hiking interest rates to combat higher inflation or to keep up with the U.S. Federal Reserve could end up costing Canadians.

The fate of the NAFTA renegotiations is still up in the air with a new potential deadline announced by U.S. Trade Representative Robert Lighthizer who expects a deal to be reached in mid May. Next week will be crucial for the deal as Canadian, Mexican and US negotiators will meet to try to fast track an agreement.

Market events to watch this week:

Friday, May 4

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change