{kind=link}

Here are the latest developments in global markets:

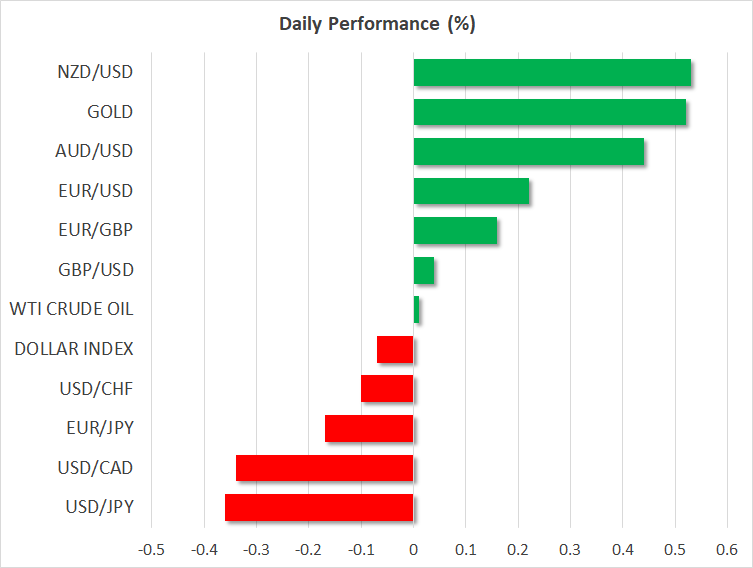

FOREX: The US dollar continued to move lower during the early European session, deviating further below the 3-month high of 110.02 versus the yen reached during Wednesday’s European trading. Specifically, dollar/yen retreated to 109.49 (-0.32%), a day after the FOMC left interest rates unchanged. The accompanying statement acknowledged that inflation is close to target, signaling that policymakers would accept inflation surpassing the 2.0% target. However, a drop of a statement highlighting the continued expansion of the economy made the statement look somewhat dovish, pushing the dollar lower. With the Fed’s meeting out of the way now, the focus is shifting to US jobs data due on Friday for further indication of the strength of the economy and inflationary pressures. The dollar index, which gauges the greenback’s strength versus six major currencies, eased by 0.04% to 92.47 after hitting a 4-month high of 92.63 on Wednesday. Pound/dollar edged down from 1.3628 to 1.3593 in the wake of worse-than-expected UK Services PMI, remaining 0.03% up on the day. Euro/dollar pared some of its earlier gains after Eurozone’s CPI figures appeared slightly weaker than expected, slipping from 1.2000 to 1.1980 (+0.25%). The antipodean currencies erased yesterday’s losses, with aussie/dollar and kiwi/dollar advancing by 0.53% and 0.59% respectively. Dollar/loonie was on the back foot today but remained within a narrow range over the last daily sessions, trading at 1.2929 (-0.40%). The Norwegian krone surged against the dollar and the euro after Norway’s central bank kept rates steady as expected, reiterating that the first rate hike would come after the summer.

STOCKS: European stocks were in the red at 1000 GMT on Thursday as the euro managed to bounce up. Disappointing earnings releases weighed on equities as well. The benchmark European STOXX 600 dived by 0.27%, while the blue-chip Euro STOXX 50 was down by 0.32%. The German DAX 30 fell by 0.29% after a strong bullish day. The French CAC 40 and the Spanish IBEX 35 were down by 0.27%, while the British FTSE 100 declined by 0.07%. In Asia, Japan’s Nikkei 225 and Topix closed marginally lower by 0.16% and 0.15% respectively. In the US, even though the S&P, Dow Jones, and the Nasdaq all retreated yesterday, futures tracking these indices are currently in the green, pointing to a higher open today.

COMMODITIES: Oil prices were moving higher as speculation that the US could reimpose sanctions to Iran overshadowed fears over a rising US production. West Texas Intermediate crude rose by 0.29% to $68.18 a barrel and Brent jumped by 0.20% to $73.59 a barrel. Gold price gained for the second session in a row, last seen at $1,311.80 per ounce (+0.56%) ahead of US-China trade talks.

Day ahead: US trade balance & ISM Services PMI feature on the calendar

Investors will keep a close eye on the dollar and the loonie later in the day as the US and Canada are scheduled to update a number of economic measures.

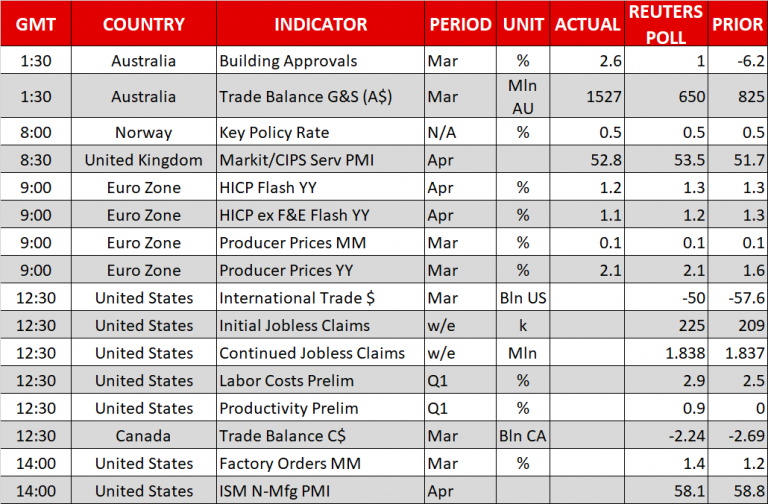

At 1230 GMT, the US international trade deficit for the month of March is expected to narrow to $50.0 billion after reaching a 9 ½-year high of $57.6bn in the previous month. Investors will also monitor the bilateral trade figures given Trump’s dissatisfaction on trade deals particularly with the EU, Japan, and China. Canada and Mexico, on the other hand, are said to be within reach of an agreement with the US on NAFTA, with the deal probably coming before the Mexican presidential elections in July and the US mid-term elections in November. Recall that Trump decided to extend import tariff negotiations on steel and aluminum until June 1 after temporary exceptions expired on May 1, signaling that maybe a global trade war is not a desirable option. Moreover, the US trade delegation led by the Treasury Secretary Steven Mnuchin has arrived in China on Thursday for two days to start two-day tariff negotiation with the Chinese team.

At the same time, the US Department of Labor will issue its weekly report on initial jobless claims, with analysts anticipating the number of people applying for unemployment benefits for the first time to rise to 225k in the week ending April 27 compared to 209k seen in the preceding week. Labor costs and productivity for the first quarter will be published along with the above data, while Canadian trade numbers will be also under review at 1230 GMT.

Later, at 1400 GMT, the US will see the release of factory orders for the month of March and April’s ISM services PMI, with the former anticipated to rise by 1.4% m/m, faster than the 1.2% expansion in February, and the latter projected to slow down by 0.7 points to 58 but remain above the growth threshold of 50.

In politics, local government elections are taking place in the UK today. The outcome could work against the UK Prime Minister, Theresa May, as the markets believe that the opposition parties could see their council seats increasing, especially in London, given May’s controversial Brexit plans. A defeat for May could shed a dark light on her leadership and her efforts to achieve a clear exit from the EU’s customs union. The first results will arrive by midnight. No local votes will take place in Scotland, Wales and Northern Ireland.

In equity markets, the earnings season continues, with Activision Blizzard and Xerox being among companies releasing quarterly results on Thursday; both corporations will be reporting after today’s US market close.

Turning to public appearances, ECB Vice President Vitor Constancio and ECB Executive Board member Benoit Coeure will be talking about fostering a banking and capital markets union within the eurozone at 1200 GMT and 1230 GMT respectively.