{kind=link}

Eurozone flash inflation readings will be available for review on Thursday at 0900 GMT and forecasts suggest that price growth in the monetary union will continue to lack momentum needed to reach the European Central Bank’s (ECB) inflation target, justifying the central bank’s patience in removing stimulus.

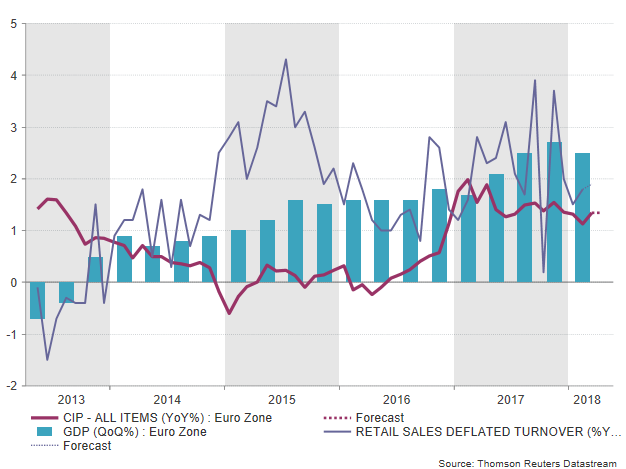

On an annual basis, the headline Harmonized Consumer Price Index (HICP) is said to have increased by 1.3% as in March, while the core equivalent which trims volatility, is seen marginally lower at 1.2% y/y compared to 1.3% in the previous month. This would not be a surprise as preliminary HCPI figures published separately in Germany, France, and Italy a couple of days ago, – the three largest EU economies – failed to pick up speed in April, remaining around March levels. Therefore, with the bloc’s inflation gauges showing no signs of an upward trend towards the ECB’s ideal price growth of 2.0%, policymakers are unlikely to make any changes to their accommodative monetary strategy. Instead, they will probably hold asset purchases to run until their expiration date in September or even beyond if key indicators appear softer in the coming months, with the announcement probably coming in June. The hint could also come in July if the data miss is significant. A rate hike is also expected to come well after the quantitative easing program matures, making markets wondering whether the central bank will be able to catch up with its counterparts before the next recession hits. It is also worth noting that the ECB’s survey of 58 professional forecasters conducted in early April showed that inflation could reach 1.6% in 2017 and 1.7% in 2020; 0.1 percentage points lower than estimates three months ago.

The start of 2018 was a gloomy one for the bloc as business surveys surprisingly moderated and preliminary GDP growth figures for the first quarter of the year slowed down as expected. In the coming months, trade risks could translate into even weaker business confidence if the EU and the US fail to reach an agreement on steel and aluminum import tariffs. This in return could boost prices of imported goods and under softer competition domestic producers could find the opportunity to raise their own prices as well, leading inflation higher as policymakers wish for. However, the ECB will likely refrain from winding down stimulus under this scenario in which economic growth is narrowing on the back of trade inefficiency. Still, this seems not to be the case for now as Trump’s decision to extend temporary tariff exceptions for the EU, Canada, and Mexico showed that the US President is not in the mood to start a global trade war.

The start of 2018 was a gloomy one for the bloc as business surveys surprisingly moderated and preliminary GDP growth figures for the first quarter of the year slowed down as expected. In the coming months, trade risks could translate into even weaker business confidence if the EU and the US fail to reach an agreement on steel and aluminum import tariffs. This in return could boost prices of imported goods and under softer competition domestic producers could find the opportunity to raise their own prices as well, leading inflation higher as policymakers wish for. However, the ECB will likely refrain from winding down stimulus under this scenario in which economic growth is narrowing on the back of trade inefficiency. Still, this seems not to be the case for now as Trump’s decision to extend temporary tariff exceptions for the EU, Canada, and Mexico showed that the US President is not in the mood to start a global trade war.

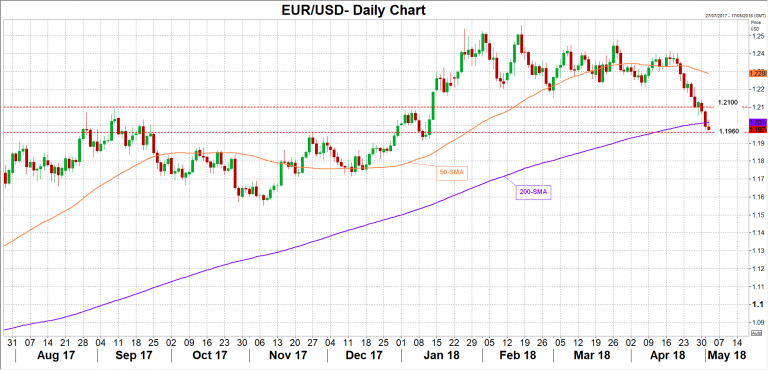

Turning to forex markets, euro/dollar could experience further pressure if Thursday’s CPI readings disappoint, meeting immediate support at the November’s low of 1.1960 before the focus shifts down to the 1.1900 psychological level. On the other hand, if CPI beats expectations, the price could break above the 200-day simple moving average which currently stands 1.2014 to find resistance at the 1.2100 handle.

On Friday, Eurozone retail sales for the month of March could add volatility to euro/dollar as well. Unlike CPI forecasts, projections for retail sales are optimistic, with analysts predicting an expansion of 0.5% m/m compared to 0.1% seen in February, the highest since January. On a yearly basis, the measure is said to rise by 0.1 percentage points to 1.9%.