{kind=link}

Here are the latest developments in global markets:

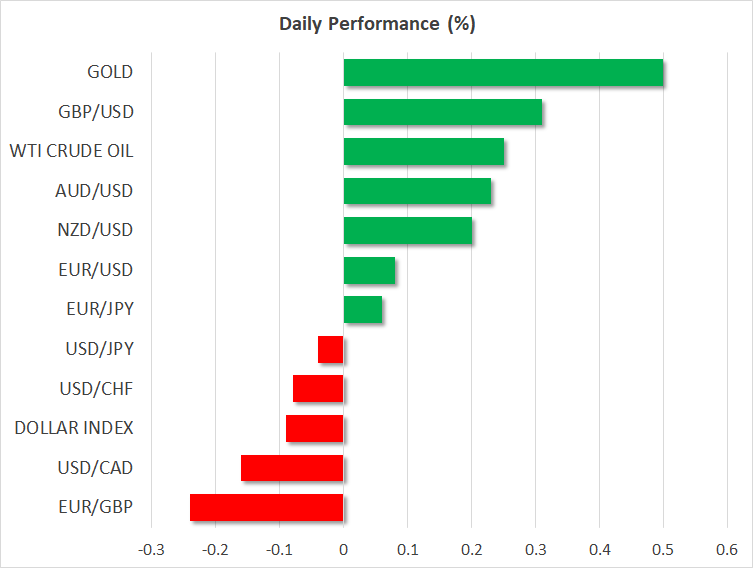

FOREX: The US dollar managed to pare some losses against the Japanese yen made after it touched a 3-month high of 109.91 earlier in the day, rising to 109.83 (-0.02%). The dollar index, which gauges the greenback’s strength versus six major currencies, managed to hit a 4-month high of 92.56 on Tuesday, peaking above the 200-day moving average for the first time in a year but today the index was slightly lower at 92.36 (-0.09%). Pound/dollar rose by 0.28% on Wednesday snapping five straight negative daily sessions, as better-than-expected UK construction PMI data calmed investors concerned about a sharp economic slowdown. Eurozone’s GDP flash reading for the first quarter eased to 2.5% y/y as expected, while the bloc’s final Markit manufacturing PMI was surprisingly revised higher, with euro/dollar moving marginally higher by 0.09% to touch 1.2000. In antipodean currencies, aussie/dollar and kiwi/dollar were in a bullish mode, both rising by 0.29%, recovering some of the extraordinary losses they posted in recent days. Dollar/loonie was down by 0.18% but within the range developed last week.

STOCKS: European stocks gained in Europe as many investors returned from holidays in contrast to their Asian counterparts which were on the back foot. The benchmark European STOXX 600 rose by 0.69% at 0944 GMT led by tech stocks and basic materials, while the blue-chip Euro STOXX 50 was up by 0.53%, being in the green for the fifth day in a row. The German DAX 30 surged by 1.30% hitting a fresh three-month high and the French CAC 40 moved higher by 0.25%. Also, the British FTSE 100 jumped by 0.66%. In the US, even though the S&P, Dow Jones were mixed on Tuesday, futures tracking these indices are currently in the green, pointing to a higher open today.

COMMODITIES: Oil prices were mixed, with WTI crude trading higher by 0.25% at $67.43 per barrel and Brent trading lower by 0.26% at $72.94. Fears on whether the US will reimpose sanctions to Iran continued to support oil prices, while worries over rising US production continued to limit gains. In precious metals, silver surged by 1.51% and gold gained 0.58%.

Day ahead: Eyes on FOMC rate decision; ADP employment report in focus

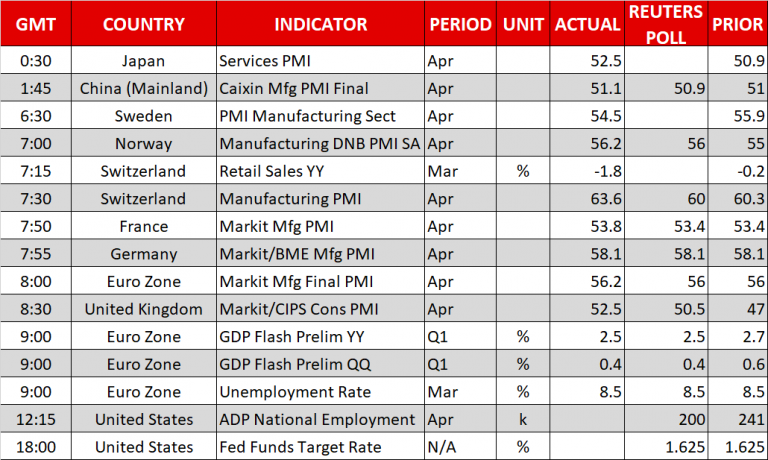

The FOMC rate decision will be the highlight event later in the day. Analysts are currently fully pricing in two more rate hikes this year and have started to bet on a third one, but this time they are widely expecting rates to remain unchanged at 1.75% as no press conference is scheduled to follow the rate announcement. However, analysts will be focused to identify any hawkish tweaks to the language expressed in the FOMC monetary statement as a series of data published recently proved that the US economy is gaining momentum. Should policymakers acknowledge encouraging economic trends, the dollar could stretch higher. Still, comments underlying the uncertainties in the trade front could limit greenback’s gains. Yet, Trump’s decision to extend negotiations on steel and aluminum import tariffs on Tuesday after temporary exceptions expired on May 1 showed that the US President is not currently in the mood to start a global trade war. The rate announcement and the FOMC rate statement are due at 1800 GMT.

Before the FOMC reveals its decision, investors will take a close eye on the ADP nonfarm employment report (1215 GMT) to finalize their projections for the more comprehensive nonfarm payrolls report delivered by the government on Friday. According to forecasts, the ADP numbers which track employment changes in the private sector are anticipated to show that job positions increased by 200,000 in April compared to a rise of 241,000 in the preceding month. An upward surprise in the data could hint that Friday’s NFP job numbers could also beat analyst forecasts.

Meanwhile, in oil markets, investors will be waiting for the EIA weekly update on US crude oil stocks to come into view at 1430 GMT.

In equities, Tesla is among companies releasing quarterly results on Wednesday; the carmaker will be reporting after the US market close.

Any headlines on the Brexit front are likely to attract attention as well, as the Cabinet Brexit sub-committee of senior ministers is gathering today to discuss the UK’s future customs partnership with the EU.