{kind=link}

Here are the latest developments in global markets:

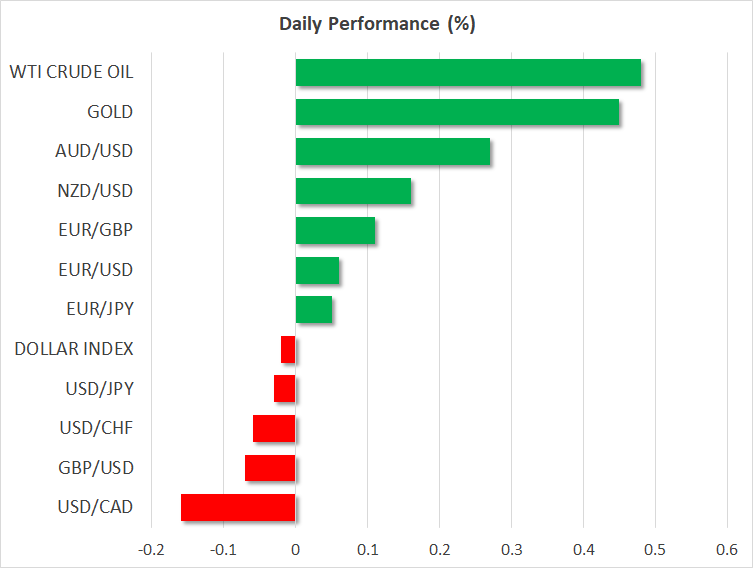

FOREX: The US dollar index continued to advance yesterday, reaching a fresh four-month high ahead of a policy decision by the Fed later today. Meanwhile, sterling came under renewed selling interest as UK data continued to disappoint, while the loonie experienced a very volatile session following some comments by BoC Governor Poloz.

STOCKS: US markets closed mixed yesterday. The tech-heavy Nasdaq Composite climbed 0.91%, the S&P 500 gained 0.25%, while the Dow Jones fell by 0.27%. Futures tracking the Nasdaq 100 are pointing to a higher open today, possibly due to Apple’s Q1 earnings beating analysts’ expectations yesterday after the closing bell. On the other hand, futures tracking the S&P and Dow are currently flashing red. The main event for these indices today will probably be the FOMC policy decision. Meanwhile, it appears that special counsel Robert Mueller would consider subpoenaing the US president should he refuse to participate in a voluntary interview relating to the Russian involvement in 2016’s presidential elections. If the situation escalates, then this could definitely weigh on equity market sentiment. In Asia, the Nikkei 225 and the Topix both declined by roughly 0.15%, while in Hong Kong, the Hang Seng shed 0.29%. In Europe, futures tracking the major indices were mostly in the red, albeit not significantly so.

COMMODITIES: Oil prices are a little higher today, recouping some of the losses posted yesterday. WTI and Brent crude are up by 0.5% and 0.4% respectively, both still hovering near their recent highs. The narrative in the oil market remains one where concerns over rising US supply are offset by speculation the US is set to impose fresh sanctions on Iran, thereby removing a significant chunk of supply from the market. In terms of US production, the weekly EIA crude inventory data today will be closely watched. As for sanctions, May 12 is the date to watch, as that is the self-imposed US deadline on deciding on Iran. In precious metals, gold is 0.45% higher today, recouping some of the losses it posted yesterday as the US dollar climbed. Today, the yellow metal will likely look to the FOMC decision for direction.

Major movers: Dollar firms ahead of Fed decision; sterling extends losses after PMI

The US dollar index continued to surge yesterday, reaching a fresh four-month high and closing above its 200-day moving average. Euro/dollar broke below the psychological barrier of 1.2000, while dollar/yen came just shy of touching the round figure of 110.00. With no clear catalyst behind the move, the greenback’s gains appear to be owed to expectations for a more hawkish tone by the FOMC today.

While no change in policy is expected, investors may be anticipating an upgrade in the language surrounding the inflation outlook, following the recent acceleration in the core PCE price index, the Fed’s preferred inflation measure. Although a rate increase in June is already fully priced in, such a hawkish shift in communication could make investors more confident that the Fed may deliver a total of four rate hikes this year, potentially fueling another round of dollar-buying. Anything less than that, though, could disappoint investors looking for such optimistic signals, leading to profit-taking in the greenback.

The UK was once again on the receiving end of disappointing economic data yesterday. The manufacturing PMI for April unexpectedly dropped to its lowest point since 2016, suggesting that after a weak first quarter, the economy may have entered the second quarter on the back foot as well. The pound plunged in the aftermath, while the implied probability for a rate hike by the Bank of England (BoE) next week dropped even further, to a mere 17%. Investors appear to be taking the view that the recent streak of soft data will keep the BoE sidelined for a while, and that any rate hike will be postponed for the end for the year.

Elsewhere, the loonie experienced a very volatile session yesterday, with wild price swings in both directions, amid some comments from BoC Governor Poloz. While the BoC chief largely reiterated remarks he had been making for days now, his comments were seen as having a more hawkish tilt. He noted the Bank is becoming more confident that less stimulus will be needed over time, and that policymakers are concerned interest rates are too low compared to their neutral level.

Day ahead: FOMC rate decision and eurozone growth numbers due

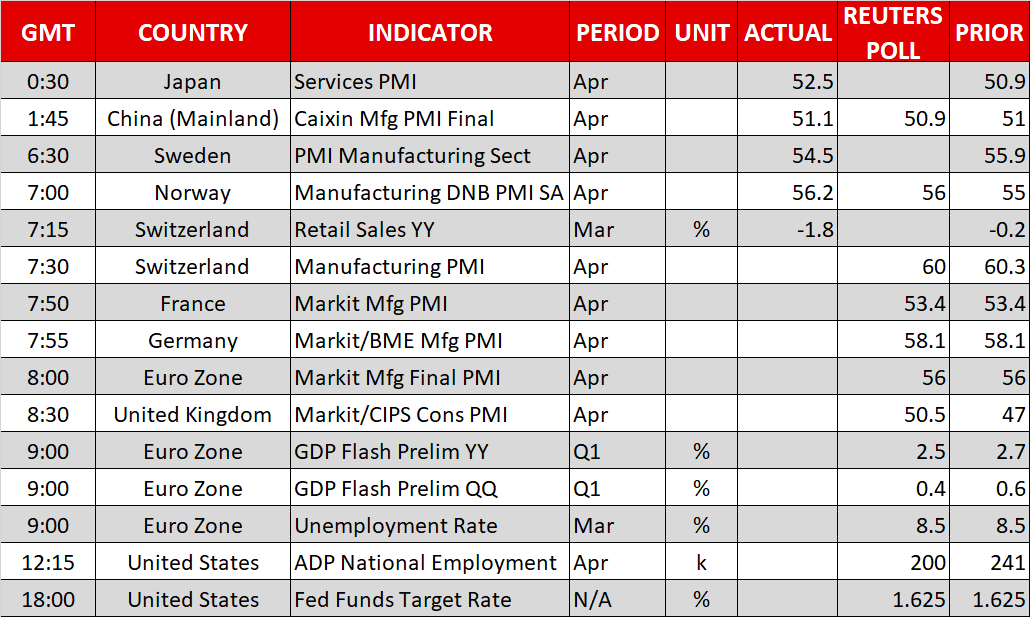

A Federal Reserve decision on interest rates, as well as GDP figures out of the eurozone are the releases expected to generate most attention out of Wednesday’s economic calendar.

At 0800 GMT, the eurozone will see the release of the final reading of Markit’s manufacturing PMI for April. The figure is projected to be confirmed at 56.0, its lowest since September of last year. Germany and France will be on the receiving end of their corresponding PMI prints a little earlier (at 0755 and 0750 respectively).

The UK’s construction PMI for April will be made public at 0830 GMT, with analysts expecting the measure to return to expansion territory above 50.

The attention will next again turn to the eurozone, as flash GDP growth estimates for Q1 are due at 0900 GMT. Projections point to a slowdown in economic activity, with the economy anticipated to have grown by 0.4% on a quarterly basis – a much slower pace relative to the 0.6% posted in Q4 2017 – and by 2.5% in yearly terms, an easing compared to the 2.7% in Q4. Meanwhile, the bloc’s unemployment rate for March, which will be released at the same time, is forecast to remain steady at 8.5%, its lowest in more than eight years.

Turning to the US, the FOMC decision on monetary policy due at 1800 GMT is the event generating most attention. No change in rates is expected. It is noteworthy that the recent patch of data out of the worlds’ largest economy seems to justify the case for the delivery of a “hawkish hold” of interest rates at current levels. Should this materialize, to the extent it signals a more aggressive tightening cycle by the Fed than currently priced in, then the greenback could extend its recent gains relative to other major currencies. At the moment, Fed fund futures project that markets have fully discounted two more 25 bps hikes this year and have begun pricing in a third rate increase as well; the odds for a third currently run at 25%. No press conference by Fed chief J. Powell will take place following the completion of today’s meeting and thus, price action will come solely from the statement accompanying the decision.

Earlier in the day (1215 GMT), the ADP report on the number of jobs positions added to the US economy by the private sector in April will be attracting interest. This is seen by some as a preamble to the more comprehensive nonfarm payrolls report due on Friday.

In energy markets, the EIA’s report (1430 GMT) on crude oil inventories for the week ending April 27 will be of interest.

In equities, Tesla is among companies releasing quarterly results on Wednesday; the carmaker will be reporting after the US market close.

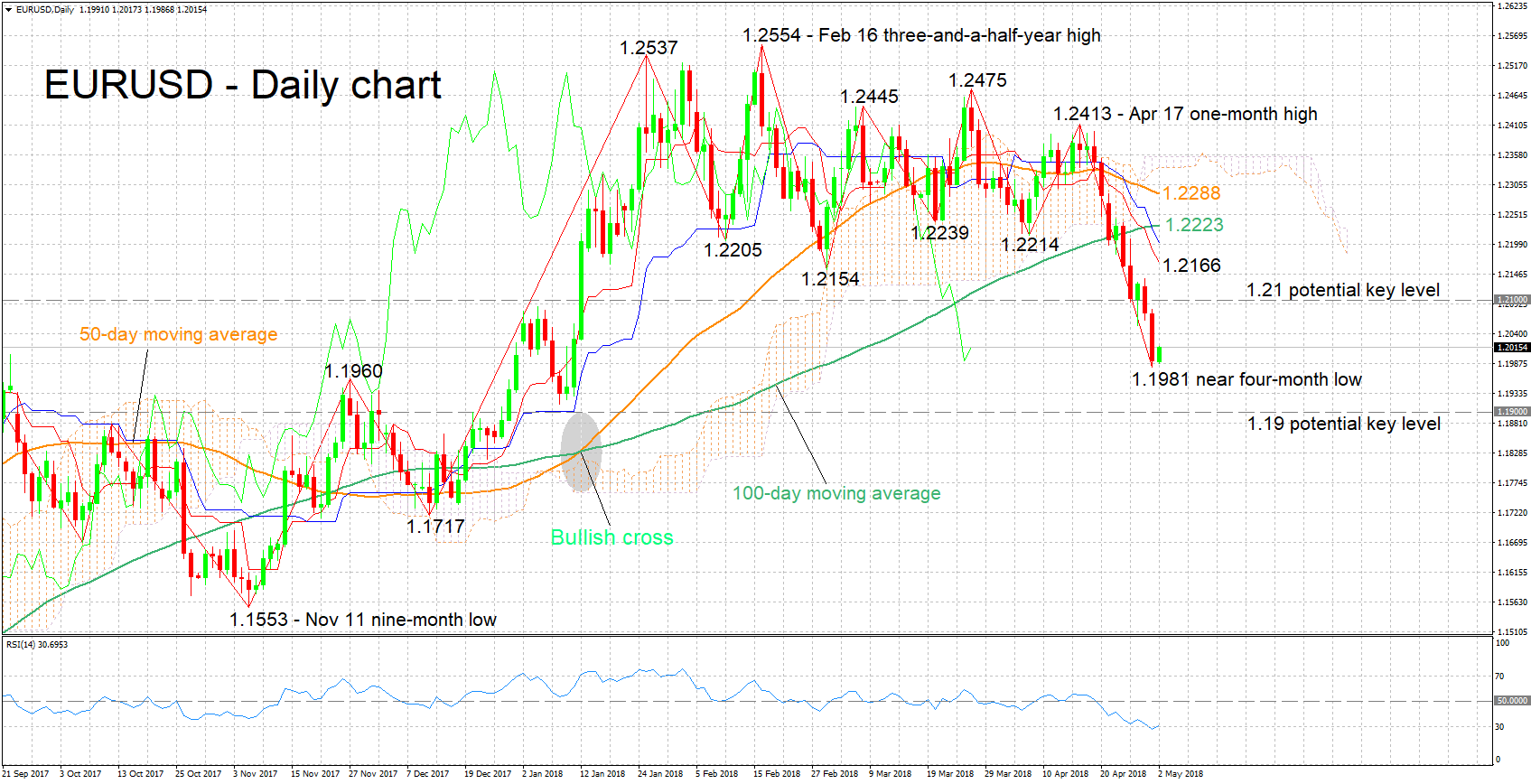

Technical Analysis: EURUSD short-term bearish; RSI close to oversold

EURUSD is trading roughly 25 pips above Tuesday’s near four-month low of 1.1981. The negatively aligned Tenkan- and Kijun-sen lines are projecting a bearish picture in the short-term. The declining RSI supports this view, notice though that the indicator is close to oversold levels.

Upbeat growth figures out of the eurozone are anticipated to support EURUSD, with resistance to advances potentially coming around the 1.21 round figure.

Conversely, disappointing numbers are likely to push the pair further down. Support could be taking place at the moment around yesterday’s low of 1.1981, including the 1.20 handle. A downside violation will start to increasingly turn the attention to 1.19, while support could also come around 1.1960, this being a top recorded in late 2017.

The pair is likely to face volatility in the aftermath of the FOMC decision as well, while ADP employment figures out of the US also have the capacity to move EURUSD.