{kind=link}

Here are the latest developments in global markets:

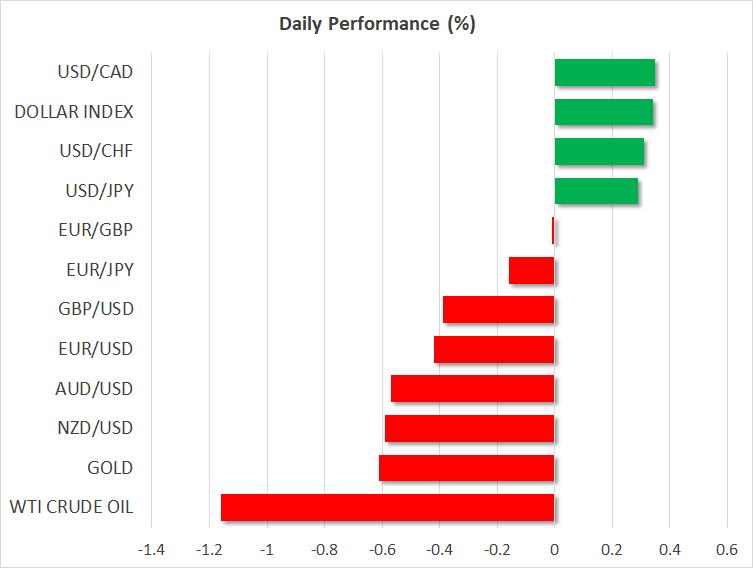

FOREX: The dollar index, which gauges the greenback’s strength versus six major currencies, edged up to 91.76 (+0.25%) during the early European afternoon, heading towards the 3 ½ -month high of 91.90 reached on Friday. Dollar/yen also climbed higher to touch an intra-day high of 109.29 ahead of the release of the core PCE index later today. On Wednesday, the Fed will announce its rate decision, while the famous Nonfarm payrolls will bring further volatility to the greenback on Friday. Pound/dollar stretched lower to a two-month low of 1.3716 (-0.41%), extending last week’s losses made after the UK GDP growth missed forecasts, casting even more doubt on whether the BoE will finally pick up rates in May. Euro/dollar was on the back foot as well, declining to 1.2081 (-0.40%). In antipodean currencies, aussie/dollar and kiwi/dollar were in a bearish mode with the former slipping by 0.37% ahead of the RBA’s interest rate decision early on Tuesday, and the latter falling by 0.40%. Dollar/loonie continued to recover, crawling up to 1.2868 (+0.32%).

STOCKS: European stocks traded higher on Monday. The benchmark European STOXX 600 rose marginally by 0.11% at 0900 GMT, being in the green for the third day in a row. The blue-chip Euro STOXX 50 was up by 0.16%, while the German DAX 30 and the French CAC 40 were moving higher by 0.18%. Also, the British FTSE 100 jumped by 0.38%. In Asia, markets in Japan and China will be closed for holidays today. In the US, even though the S&P, Dow Jones were mixed on Friday, futures tracking these indices are currently in the green, pointing to a higher open today.

COMMODITIES: Oil prices dived on Monday after Friday’s Baker Hughes indicated that the US oil rig count rose for the fourth consecutive week, pointing to higher production in the US. Despite the pullback, oil prices held near 3-year highs and are on track to post gains for the second straight month. WTI plummeted by 1.07%, to $67.37 per barrel, while Brent declined by 1.09% to $73.83 per barrel. In precious metals, silver fell by 0.64% and gold dipped by 0.41%.

Day ahead: US core PCE to head higher; RBA to stand pat on rates on Tuesday

Day ahead: US core PCE to head higher; RBA to stand pat on rates on Tuesday

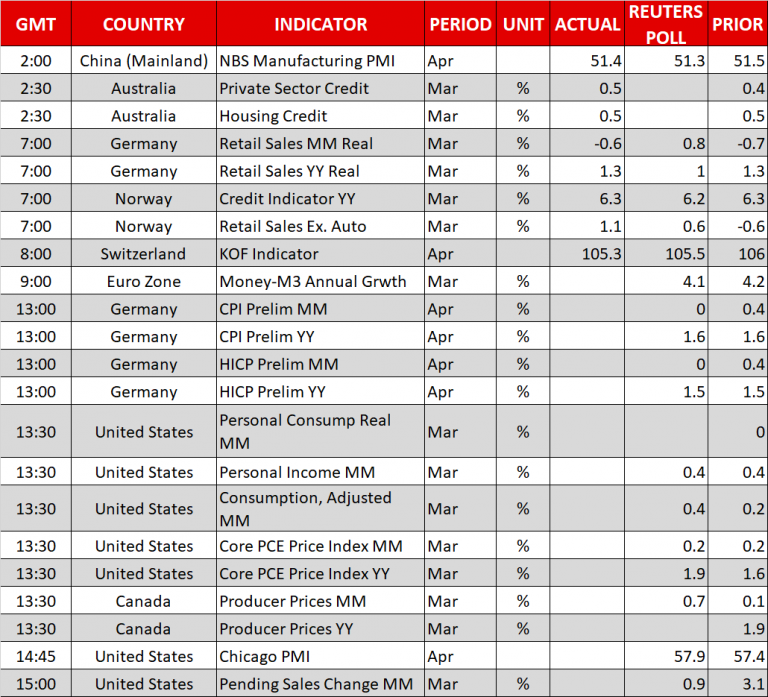

Economic releases will continue to attract attention in the remainder of the day, with inflation numbers out of Germany, the US and Canada being in the spotlight.

At 1200 GMT, Germany will publish initial CPI estimates for the month of April and in the absence of other major releases out of the Eurozone, the numbers could spark some volatility to the euro if they significantly deviate from forecasts. According to analysts, German consumer prices are expected to grow at the March pace of 1.6% year-on-year, while on a monthly basis, the measure is projected to slow down from 0.4% in March to 0.0%. Harmonized CPI readings (HICP), which are comparable to CPI data in other EU countries, are anticipated to follow the same pattern.

Meanwhile in the US, investors will be eagerly waiting for the core PCE as well as for the personal income and consumption figures to come into view at 1230 GMT. The Fed’s favorite inflation measure is expected to advance for the second consecutive month, rising from 1.6% to 1.9% y/y in March. Should the gauge surprise to the upside, the dollar could extend today’s rally on the back of prospects that the Fed could appear more confident to tighten monetary policy even further at the conclusion of its two-day policy meeting on Wednesday. Markets are currently pricing in two more rate hikes this year and an upbeat inflation report later today could lift the odds for a third one which stand at 20.0% at the moment. Note that on Wednesday, FOMC policymakers are said to stand pat on interest rates, though, they might turn more hawkish on the view of higher inflation numbers.

Other US data due later in the day include April’s Chicago PMI (1345 GMT) and pending home sales for March (1400 GMT).

Canadian producer prices for March will be made public at the same time the US sees the release of core PCE price data (1230 GMT).

Fast-food chain McDonald’s is among companies releasing quarterly results today; the company’s report is scheduled for release before the opening bell on Wall Street.

On Tuesday, many parts of the world will be on holiday to celebrate Labor day. The calendar, however, will be relatively busy in some major economies.

At 0430 GMT, the focus will turn to Australia and the RBA’s decision on interest rates. Unlike its US counterpart, the RBA is in no rush to raise its borrowing costs from record lows probably not until mid-2019 as households are still struggling to repay their mounting debts according to the central bank’s latest financial stability statement delivered a few weeks ago. Last week’s data were not encouraging either, as inflation fell short of expectations of meeting the RBA’s target of 2.0%.

UK manufacturing PMIs will follow up at 0830 GMT, while the US will see its ISM manufacturing PMIs as well later at 1400 GMT. Forecasts are for both indicators to ease on April.

Elsewhere, GDP growth readings will be of greater interest in Canada (1230 GMT) as analysts wait to see whether the Canadian economy will turn back to growth in February after contracting by 0.1% m/m in the previous month. Particularly, projections are for the Canadian GDP growth to reach 0.3% m/m. In case, the numbers undershoot forecasts, the loonie could follow a downtrend.

In New Zealand, global dairy prices delivered at a tentative time will have the potential to move the kiwi to the upside if they rise for the third consecutive time.

In oil markets, the American Petroleum Institute will issue its weekly report on US crude oil inventories at 2030 GMT. It will be interesting to see whether the results will back fears of rising US production that could harm OPEC’s efforts to curb supply. Recall that on Friday Baker Hughes indicated an increase in the number of US oil drillings.