{kind=link}

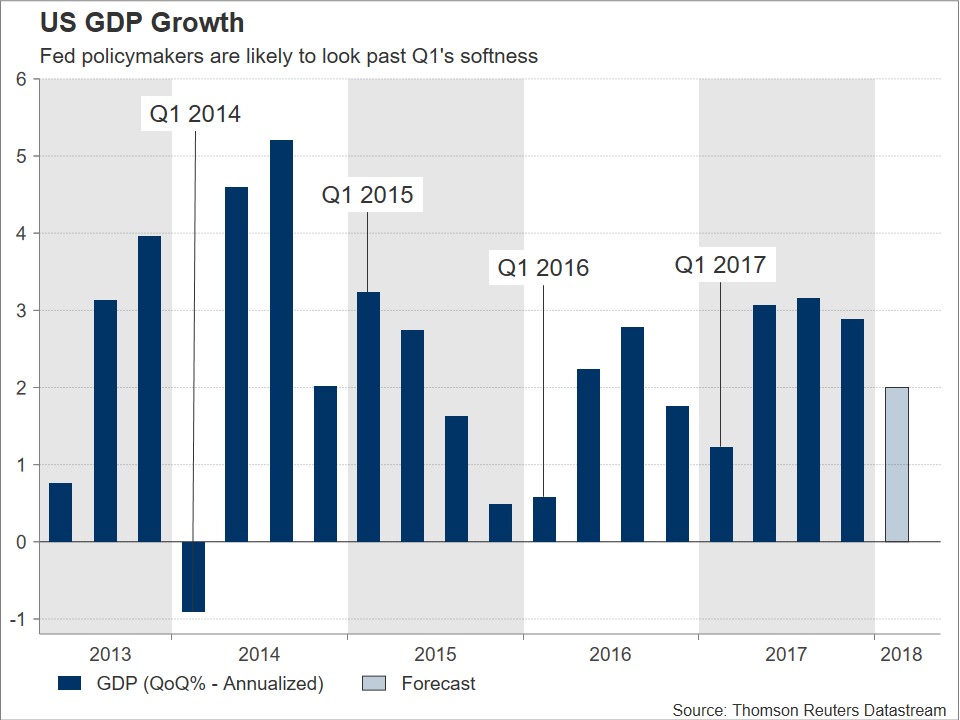

The US will see the release of its advance Q1 2018 GDP growth estimate on Friday at 1230 GMT. Economic activity is projected to have slowed considerably relative to the previous quarter, though the softness is unlikely to trouble Fed policymakers much.

According to analysts’ forecasts, the preliminary GDP growth rate for the first quarter of the year is expected to stand at 2.0% on an annualized basis, significantly below Q4 2017’s respective figure of 2.9%.

The US economy tends to underperform in the beginning of a given year – with the exception of 2015, this can be observed from the chart above as well – and FOMC members are likely to look past first-quarter weakness, focusing on the bigger picture when they gather next week for their two-day monetary policy meeting concluding on May 2.

In terms of the bigger picture, the economy is likely to post stronger growth further ahead on the back of the fiscal stimulus enacted by the Trump administration. April PMI data published on Monday by IHS Markit seem to support the case for stronger expansion in Q2, with Markit’s chief business economist making reference to an economy that is picking up pace at the start of the second quarter. Beyond this though, another factor contributing to FOMC policymakers probably sticking firmly to a path of policy normalization are rising inflation expectations, this also being reflected by the recent jump in Treasury yields. Indicatively, the return on the 10-year Treasury Note rose to its highest since early 2014 on Wednesday, exceeding the widely-touted 3% mark.

In terms of Fed hike expectations, Fed funds futures are projecting that market participants have fully priced in two more percentage-point rate increases by the US central bank, while they currently see a more than 20% chance for a third interest rate hike, something which would bring the total for 2018 to four. For perspective, a few days ago, only one additional hike was fully priced in.

Turning back to tomorrow’s growth figures, the latest forecast of the Atlanta Fed’s GDPNow model puts it at 2.0% on an annualized basis, in line with the previously mentioned GDP estimate, while interestingly, the New York Fed expects it to remain unchanged at 2.9%.

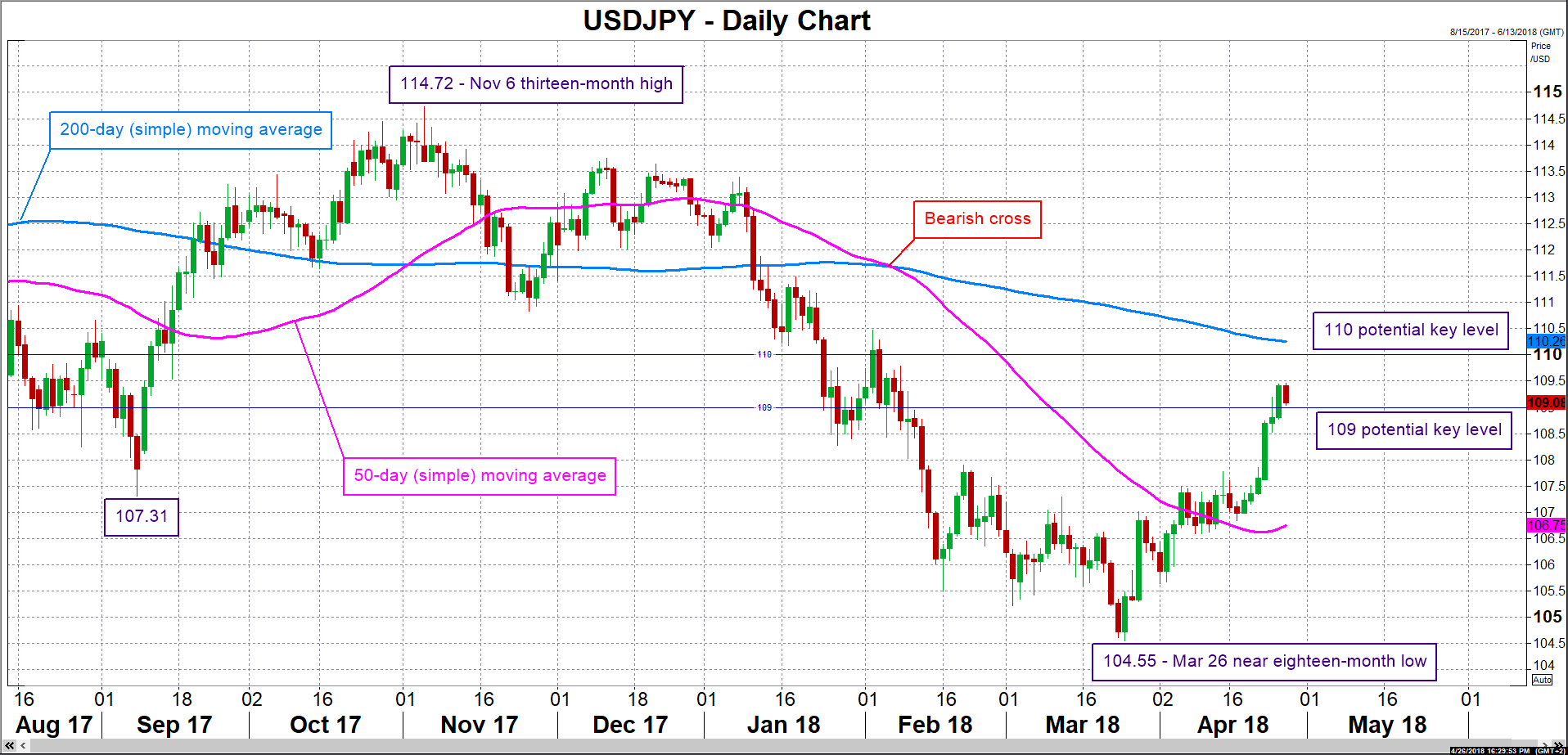

Should an upbeat release be delivered, then such an outcome is likely to spur buying interest for dollar/yen, pushing it to fresh highs; the pair reached a two-and-a-half-month high of 109.46 earlier on Thursday. Resistance to advances might come around the 110 handle which may act as a psychological hurdle. Notice that the current level of the 200-day moving average lies not far above at 110.26. On the downside and in case of weaker-than-anticipated growth numbers, support could be met around the 109 round figure – price action is close to this level at the moment. Further below and if the data disappoint by a large margin, pushing investors to take additional profits after the recent surge in the pair, then the 108 handle would be eyed next.

Other releases that will be made public alongside numbers on the pace of economic activity are Q1 employment costs, as well as the advance estimate of core PCE prices for the same quarter. In terms of reaction in the dollar/yen pair, one should take into account that ahead of the US releases, Japan will also be on receiving end of important data on employment, industrial production and retail sales, while a Bank of Japan decision on monetary policy is due on Friday as well.