{kind=link}

Here are the latest developments in global markets:

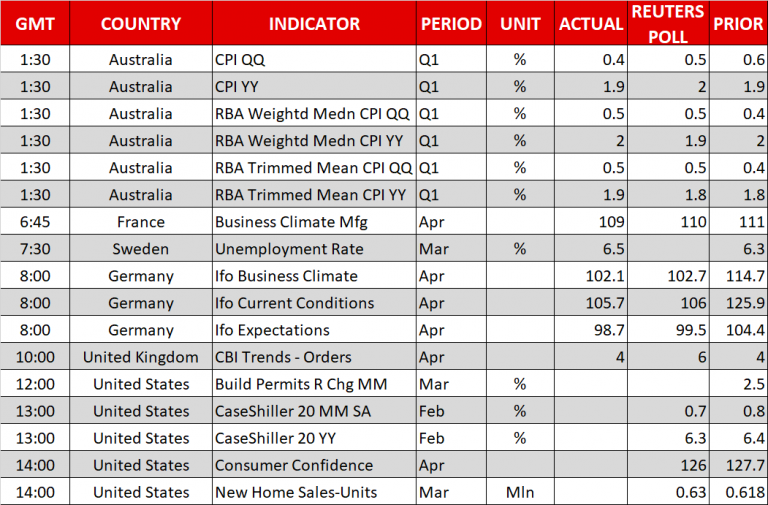

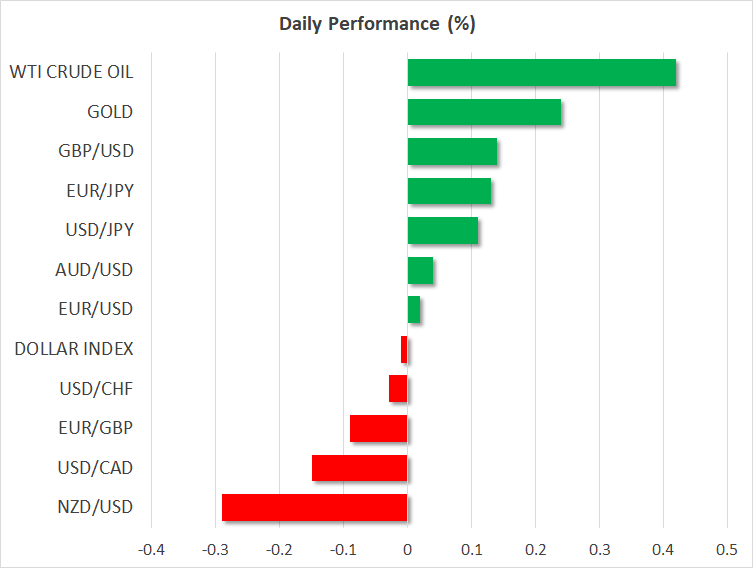

FOREX: The dollar index was consolidating around 91.00 in the early European afternoon, its highest level reached since mid of January despite 10-year US Treasury yields retreating further below the 3.0%. Easing geopolitical and trade tensions were also supportive to the greenback as safe-havens continued to lose attractiveness, with dollar/yen crawling slightly up to a fresh 2 ½-month high of 108.90. On the other hand, euro/dollar was struggling at two-month lows, last seen at 1.2200 (-0.03%), amid expectations that ECB policymakers could hold a cautious stance at the end of their two-day policy meeting on Thursday given recent disappointing PMI and inflation readings. The German Ifo business climate index missed expectations today as well, but the euro did not react much to the figures. Pound/dollar was moving sideways around 1.3945 (+0.01%), unable to deviate above 1½ -month troughs as the Brexit legislation has so far received 3 defeats in the House of Lords, adding further pressure to the UK Prime Minister who wants a clear exit from the EU ahead of a final Brexit bill consideration in May by Parliament members. In antipodean currencies, aussie/dollar was flat at 0.7606 despite CPI figures falling short of expectations earlier in the day, while kiwi/dollar remained the worst performer among major currencies, changing hands at 0.7121 (-0.35%). Dollar/loonie was slightly weaker at 1.2838 (-0.10%) but near three-week highs reached on Monday after the Bank of Canada’s governor signaled no rush to raise interest rates even if inflation is ticking higher.

STOCKS: European stocks were moving upwards at 0800 GMT, strengthening on the back of a weaker euro, with the pan-European STOXX 600 rising by 0.16% above the 10-week highs reached yesterday. The blue-chip Euro STOXX 50 was up by 0.35% driven by gains in the technology sector. The German DAX 30 increased by 0.30%, supported by news that Germany’s SAP – Europe’s largest tech company – was gaining ground against competitors such as Oracle. Britain’s FTSE 100 climbed by 0.30%, the French CAC 40 inched up by 0.09%, while the Spanish IBEX 35 edged down by 0.04%. Indices tracking US stock futures were flashing green, signaling to a positive open.

COMMODITIES: Oil prices were on the rise on Tuesday, underpinned by OPEC-led supply cuts and increasing tensions between the US and Iran which could force the US to impose additional sanctions on Iran. WTI crude was up at $69.06 (+0.61%) and Brent was last seen at 74.99 (+0.37%), its highest since November 2014. In precious metals, gold was gaining ground, rising to $1,327.10 (+0.24%) per ounce.

Day Ahead: US consumer confidence & new home sales pending

Tuesday’s calendar is a light one, with the focus possibly remaining on the ECB interest rate decision on Thursday and the GDP flash estimates out of the US and the UK on Friday. Companies releasing earnings will also be attracting interest.

Out of the US, at 1300 GMT, the Case-Shiller indices gauging house prices during the month of February will be made public, while data on consumer confidence for the month of April will be available at 1400 GMT. On a monthly basis, the consumer confidence index is expected to fall to 126.0 versus 127.7 in the prior month. Also, at the same time, new home sales for the month of March are anticipated to edge up by 1.9% m/m following a decline of 0.6% in the preceding month.

In energy markets, investors will be waiting for the API weekly report to indicate the change in US crude oil stocks.

Turning to today’s public appearances, at 1800 GMT Federal Reserve Bank of Philadelphia President Patrick Harker will be participating in a conference, while Bank of England Governor Mark Carney will be giving a speech at the same time.