{kind=link}

U.S. Highlights

- Financial markets bounced back from the selloff last week as trade tensions between China and U.S. eased somewhat.

- Both headline and core CPI inflation ticked up in March on a year-on-year basis.

- FOMC March meeting minutes indicate that some members contemplated a faster pace of rate hikes this year. Overall, we believe the balance of risks remains consistent with a total of three rate hikes in 2018.

Canadian Highlights

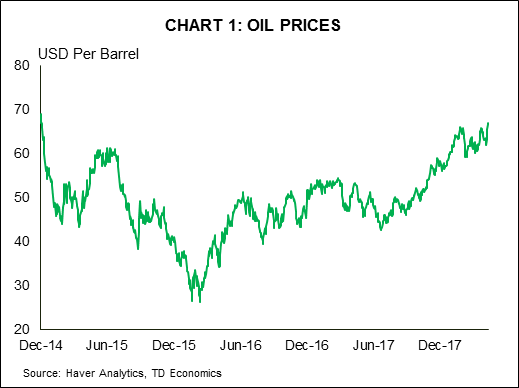

- The WTI benchmark jumped 8% this week to a 3-year high of US$67 per barrel as geopolitical tensions trumped a bearish US storage report.

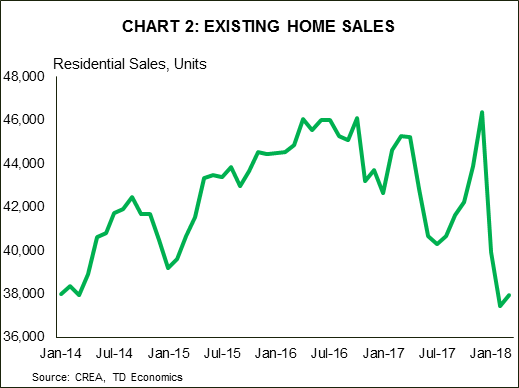

- Housing starts remained strong in March, bringing the 6-month average to 227k units. Existing home sales stabilized during the month, after falling sharply in the prior two. Meanwhile, quality-adjusted home prices rose at the slowest pace in nearly 5 years.

- The Bank of Canada is expected to remain on the sidelines next week, with the Monetary Policy Report providing the Bank’s updated outlook for the Canadian economy.

U.S. – Trade Deals (Not Wars) Back on the Agenda

Politics dominated headlines this week. Financial markets recovered from last week’s selloff, as the fear of a full blown trade war between the U.S. and China receded for at least a few days. However, geopolitical tensions remain elevated as more economic sanctions against Russia took effect and the U.S. administration considers military action against Syria, providing a strong bid on gold and oil.

Although there has been more bark than bite on trade protectionism from the U.S. administration thus far, a hot trade war could do a lot of damage. However, events this week provide some hope that a trade war can be averted. Speaking at the Boao forum for Asia, Chinese President Xi repeated past promises to expand intellectual property protections and open various sectors of China’s economy to foreign investment. Later in the week, word spread that President Trump was directing officials to explore returning to the Trans Pacific Partnership, an agreement that he withdrew from shortly after coming to office.

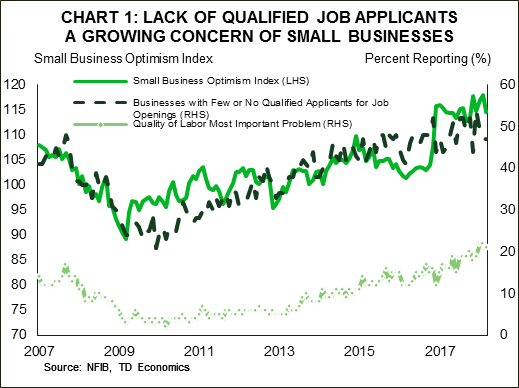

With heightened uncertainty about the future trading relationship between the world’s economic heavyweights, business confidence could start to wane. Small business optimism pulled back in March, but the decline comes after the index reached a 35 year high in February. While a pullback was expected, one cannot rule out that rising trade tensions contributed to the greater-than-anticipated decline. What’s more, the report reinforced the labor market themes we’ve seen from the ISM surveys: rising labor shortages driving up wages as firms act to attract and retain workers (Chart 1).

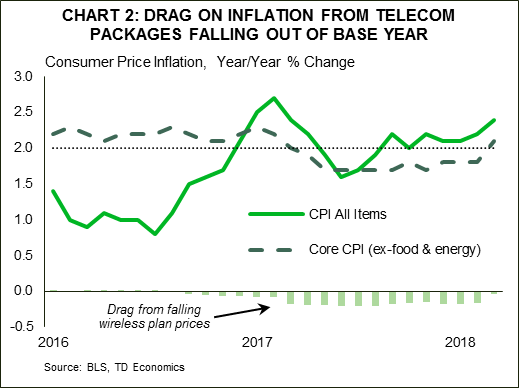

Rising wages and input costs will eventually drive consumer prices higher. For the month of March, consumer prices rose 2.4% (year-on-year), but a more meagre 0.1% monthly change owing to decline in gas prices. Most importantly, core inflation (CPI ex-food and energy) ticked up to 2.1% y/y from 1.8% in the previous month, largely on the back of base-year effects (Chart 2). Still, core inflation rose a healthy 0.2% on the month, suggesting that a hot economy is leading to a broad build-up in price pressures.

Labor shortages, solid wage growth, and rising prices should reassure the Federal Reserve that higher interest rates are warranted. Although there was little new information in the March FOMC meeting minutes released this week, there were still some discussions worth noting. Strong economic growth along with rising price pressures are evidence that the economy is coping well with past rate hikes and can absorb more. In fact, some participants think that a total of four rate hikes may be warranted this year, while also suggesting that the language in the monetary policy statement be changed to reflect a view that interest rates are exerting a more neutral rather than accommodating impact on economic activity. Still, uncertainty about the ultimate impact of fiscal stimulus on output and the downside risks posed by trade protectionism is more consistent with a total of three rate hikes this year.

Canada – BoC Likely To Sit On The Sidelines Next Week

Canada – BoC Likely To Sit On The Sidelines Next Week

Canadian financial markets were up this week, led by an 8% jump in oil prices that reached a three-year high. This helped to push the loonie above 79 US cents, while the S&P TSX finished the week in slightly positive territory.

The WTI crude oil benchmark surged to over US$67 per barrel, as geopolitical tensions trumped a bearish US storage report. Indeed, comments from President Trump suggesting that Russia should get ready for US missiles to be fired at Syria was the key catalyst driving oil prices higher. Meanwhile, an unexpected build in US inventories and rising oil production stateside was brushed off amid the these threats. While inventories are closing in on OPEC’s target (the 5-year average), current prices still appear to be higher than fundamentals would suggest, with some reversal likely once geopolitical tensions abate. However, should tensions intensify further, or sanctions against Iran be reinstated, prices could gain further ground. Headlines this week suggested that Saudi Arabia is targeting an oil price of US$80 per barrel; that would be a tall order considering the market is not quite balanced and prices at current levels or higher would trigger further growth in output, particularly in the US.

On the data front, housing starts remained strong in March, bringing the six-month average to 227 thousand units – a solid pace of activity, particularly in light of the cooling seen in existing home sales and prices. Data out this morning revealed that existing home sales stabilized in March (+1.3%), follow a steep decline in the prior two months. Meanwhile, quality-adjusted home prices were up 4.6% year-on-year – the slowest pace in over four years. Hence, despite strong homebuilding activity, the drop in sales suggests that residential investment will weigh on growth in the first quarter.

Indeed, at 1.4% (annualized), Q1 economic growth is tracking well below the Bank of Canada’s forecast of 2.5%. The Bank’s outlook is likely to be downgraded in its Monetary Policy Report on the 18th alongside its interest rate decision. Economic growth seems to have gotten off to a slow start this year, but there are many positives for the data-dependent Bank to consider as it sets interest rates. The unemployment rate is sitting at a record low and inflation pressures have begun to materialize, with the core rates reaching the Bank’s 2% target level. Moreover, the Bank of Canada’s Business Outlook Survey released this week showed a high level of optimism among firms with respect to both sales and investment.

At the same time, however, there are still a number of uncertainties clouding the outlook for the Canadian economy. NAFTA renegotiations and the threat of a global trade war top the list of external threats, while the impact of higher interest rates and policy changes on the housing market and minimum wage hikes loom on the domestic front.

All told, the Bank of Canada will have to balance the positive data points against these downside risks. We suspect that the Bank will remain on hold next week, with the next hike unlikely to come before the summer. The MPR could, however, shed some light on where the Bank sees the balance of risks and what it would take to push rates higher.

U.S.: Upcoming Key Economic Releases

U.S.: Upcoming Key Economic Releases

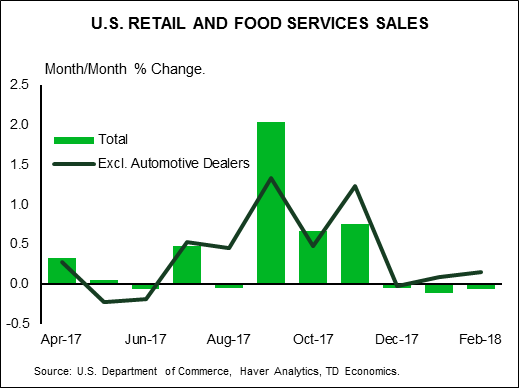

U.S. Retail Sales – March

Release Date: April 16, 2018

Previous Result: -0.1%, ex-auto: 0.2%

TD Forecast: 0.4%, ex-auto: 0.0%

Consensus: 0.4%, ex-auto: 0.2%

We expect retail sales to advance 0.4%, with the control group up 0.3%. Boosting spending will be auto sales. Tax refunds, which were pushed into March, also imply a pickup in spending. However, offsetting declines from gasoline station receipts, building materials and food services (the latter two likely weather related) should temper the increase.

Canada: Upcoming Key Economic Releases

Canada: Upcoming Key Economic Releases

Canadian Manufacturing Sales – February

Release Date: April 17, 2018

Previous Result: -1.0% m/m

TD Forecast: 1.2% m/m

Consensus: N/A

Manufacturing sales are forecast to rebound by 1.2% m/m in February on a recovery in motor vehicles. Motor vehicle exports posted a sharp rebound in February after plant shutdowns constrained output the prior month. Their recovery should also bode well for auto part shipments, which shaved 0.2% from headline manufacturing sales growth in January off reduced demand. However, energy products should provide an offset. Outside of these two product groups we expect a relatively broad increase in sales, consistent with strong survey data. Real manufacturing sales should post a gain of roughly 1.0%, slightly below the nominal print, which should help support industry-level growth for February.

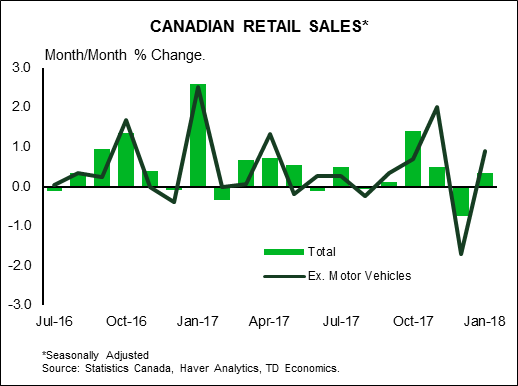

Canadian Retail Sales – March

Release Date: April 20, 2018

Previous Result: 0.3%, ex-auto: 0.9%

TD Forecast: 0.3%, ex-auto: 0.2%

Consensus: N/A

Retail sales are forecast to rise 0.3% in February, matching their performance from the prior month. We look for auto sales to make a positive contribution to the headline print but expect weaker growth in core retail sales, as a slowdown in the housing market and more modest labour market performance weigh on consumer sentiment. Gasoline station receipts should also make a muted contribution with prices little changed on the month. Real retail sales will come in slightly below the nominal print; even though an upside surprise in February CPI pushed inflation to a three-year high, prices were only up 0.15% on a SA basis. This would leave volumes relatively stable near 3% y/y, though Q1 is shaping up to be weaker after a soft 0.1% increase in January.

Canadian CPI – March

Canadian CPI – March

Release Date: April 20, 2018

Previous Result: 0.6% m/m

TD Forecast: 0.5% m/m

Consensus: N/A

We expect headline CPI to rise further above target to 2.5% y/y, reflecting a 0.5% m/m gain on the month. The latter should translate to a seasonally adjusted increase of 0.3% m/m. Energy prices should be a net positive on higher gasoline prices. We also see a boost from food prices, helped by CAD depreciation over February and March, while the food away from home category may see continued upward pressure after the Ontario minimum wage hike. Outside of food and energy, we expect shelter prices (rents and owned accommodation) to see some moderation as the tailwind from higher mortgage interest costs fades while new home price increases remains weak on the back of the pullback in the Ontario market. But outside of that, risks are generally to the upside. Currency pass-through is a net positive this month given the 4% cumulative depreciation in CAD since January, boosting categories such as apparel and vehicle prices. We also eye another one-off this month in the communications category, which could reflect another jump in internet services prices. After one telecom company ended bundled discounts in January, other telecom companies have begun hiking internet prices beginning March. The lift to headline prices could amount to a non-trivial 10bps.

In light of these upside risks, we expect exclusion-based core measures (ex food and energy, CPIX) to move higher in March while we cannot rule out firmer trend measures given lagged effects of falling economic slack. Looking ahead, we expect headline inflation to remain in the mid-2% range largely on energy prices, whereas core inflation measures should hover closer to 2.0%. That is, inflation remains largely in check.