{kind=link}

Here are the latest developments in global markets:

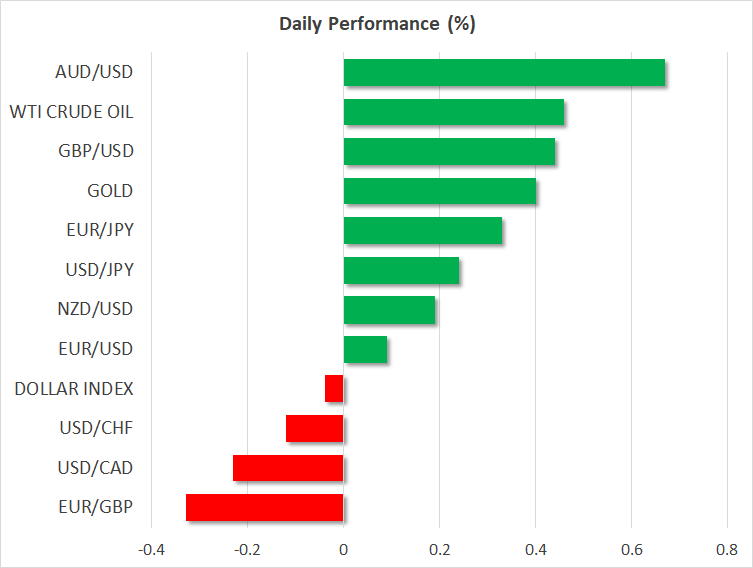

FOREX: While war and trade risks have not fully faded, Trump’s tweets on Thursday showed that the US president is considering to rejoin the Trans-Pacific free trade partnership, which he pulled out in his first months in the role. His remarks also indicated that he wanted to avoid tit-for-tat tariffs with China. In the wake of the comments, investors turned focus to riskier investments, sending safe havens lower, with dollar/yen crawling up to a fresh six-week high of 107.66 (+0.22%) today. The dollar index, though, was struggling to gain ground as the pound was on the forefoot. The pound hit a new 10-week high of 1.4284 (+0.40%) versus the greenback, while against the euro it broke a six-month range, with euro/dollar falling to a 10-month trough of 0.8627 (-0.33%). While optimism on Brexit and expectations of a rate hike in May seemed to support the currency, the rally could be also a technical correction. Note that EU-UK trade negotiations will start next week. Euro/dollar inched up to 1.2331 (+0.06%) after a deep fall yesterday triggered by somewhat dovish ECB meeting minutes, which expressed concerns about trade risks and the euro strength. Aussie/dollar moved rapidly up to 0.7805 (+0.66%), kiwi/dollar climbed to 0.7380 (+0.22%), while dollar/loonie retreated to 1.2554 (-0.25%).

STOCKS: European equities managed to close in the green yesterday and today opened slightly higher after trade and war concerns calmed down. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.14% and 0.05% respectively at 0830 GMT, on track to post gains for the third consecutive week. The German DAX 30 jumped by 0.42% driven by financials and consumer cyclicals, while basic materials and industrials were leading the Spanish IBEX 35 (+0.39%) and the French CAC 40 (+0.22%) after sanctions imposed to the Russian aluminum firm Rusal. On the other hand, the British FTSE 100 moved down by 0.11, weighed by losses in the technology sector arising after the UK’s second largest software company Sage reported worse-than-expected Q1 2018 earnings. Sage shares are now set to post their largest daily decline in 25 years. Asian equities closed mixed, while most of the indices tracking US stock futures were pointing to a positive open ahead of key earnings releases from the banking industry,

COMMODITIES: Oil prices were set to recover losses made the previous two weeks, with WTI crude and Brent surging to fresh three-year highs during the early European afternoon, peaking at $67.69/barrel (+0.92%) and $72.64 (+0.86%) respectively at 0900 GMT. Fears over a war in the Middle-East were still hanging on the background but the rally picked up speed on the release of a monthly report by the Paris-based International Energy Agency which stated that OPEC and its allies look to have accomplished their mission to bring oil stocks into desired levels. Note that recent headlines showed that OPEC is poised to extend supply cuts into 2019. In metals, gold continued to pare yesterday’s losses, climbing to 1340.76 (+0.44%).

Day Ahead: US JOLTs job openings & University of Michigan consumer sentiment awaited

The economic calendar will be thin in the remainder of the day and in the absence of important figures, investors may turn their focus on developments on the geopolitical and trade fronts.

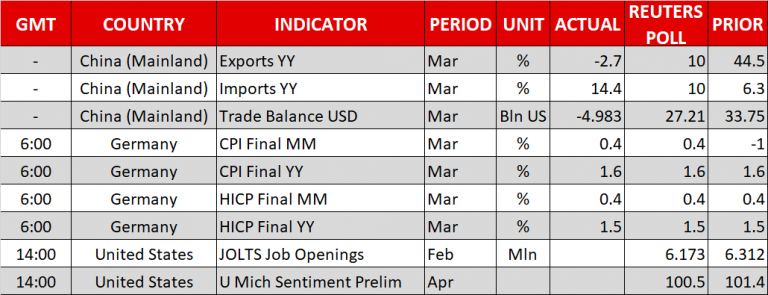

US JOLTs job openings will attract the most interest later today at 1400 GMT. Particularly, the report published by the Bureau of Labor Statistics is expected to show that 6,110 million positions opened in February compared to 6,312mn seen in the previous month.

At the same time, the University of Michigan will be delivering flash estimates on the US consumer sentiment. The index is forecast to inch down to 100.6 in April compared to 101.4 in the preceding month.

Later in the day, at 1700 GMT, Baker Hughes will publish its US oil rig count report, probably adding further volatility to oil prices which peaked at new three-year highs during the European session.

Turning to public appearances, several speeches by Fed members are scheduled later today. At 1130 GMT, Boston’s Fed President Eric Rosengren will be delivering comments ahead of a speech by St. Louis’s Fed President James Bullard at 1330 GMT. Remarks by Dallas Fed President Robert Kaplan will also attract attention at 1700 GMT.

In stock markets, earnings releases will continue to attract attention, with JPMorgan Chase, Citigroup, and Wells Fargo being among companies to reveal Q1 2018 results.