{kind=link}

The European Central Bank (ECB) will release the minutes from its March policy gathering on Thursday, at 1130 GMT. As always, investors will look for fresh clues regarding when policymakers plan to start winding down their asset purchase program, though the conversation regarding trade risks could also attract attention considering recent events.

Even though the ECB took no action in March, keeping its benchmark interest rates and asset purchase program untouched, it did tweak its forward guidance in a more hawkish direction. The Bank removed from its statement the so-called QE easing bias, the commitment that it stands ready to increase the size and/or duration of its purchases if the economic outlook becomes less favorable. This move was seen as laying the groundwork for policymakers to end their asset purchases completely later this year, triggering a spike higher in the euro.

The gains were short-lived though, with the common currency plunging to trade much lower once President Draghi started to explain the decision. The ECB chief downplayed the importance of that development, noting the Governing Council simply dropped a redundant sentence from its guidance, and that the removal does not send a signal about future decisions.

Draghi has been quite successful in “managing” market expectations, avoiding fueling too much speculation that a QE-tapering announcement is looming. Indeed, the ECB has been very careful in trying to avoid the Fed’s “taper tantrum” experience, as it heads for its own stimulus-exit door. That said, the minutes will provide an insight into the views of the entire Governing Council, not just Draghi’s. In this context, several officials have expressed their desire to end QE sooner rather than later, and the minutes could add some more color on that discussion. In particular, is the “hawkish camp” within the ECB growing larger in light of the strong growth momentum the Eurozone enjoyed recently? If so, that could work in favor of the euro.

Another area of interest will be the discussion around trade risks. Back then, only the US tariffs on steel and aluminum had been announced, so tensions had not really escalated. Still, when asked about tariffs at the press conference, Draghi said the economic impact will depend primarily on whether there is retaliation, and whether business confidence is affected, which could spill over into lower growth and inflation. Overall, his remarks suggest a conversation on the matter did take place, and investors will probably look for signals on how the Bank would respond to a further escalation in such risks.

Another area of interest will be the discussion around trade risks. Back then, only the US tariffs on steel and aluminum had been announced, so tensions had not really escalated. Still, when asked about tariffs at the press conference, Draghi said the economic impact will depend primarily on whether there is retaliation, and whether business confidence is affected, which could spill over into lower growth and inflation. Overall, his remarks suggest a conversation on the matter did take place, and investors will probably look for signals on how the Bank would respond to a further escalation in such risks.

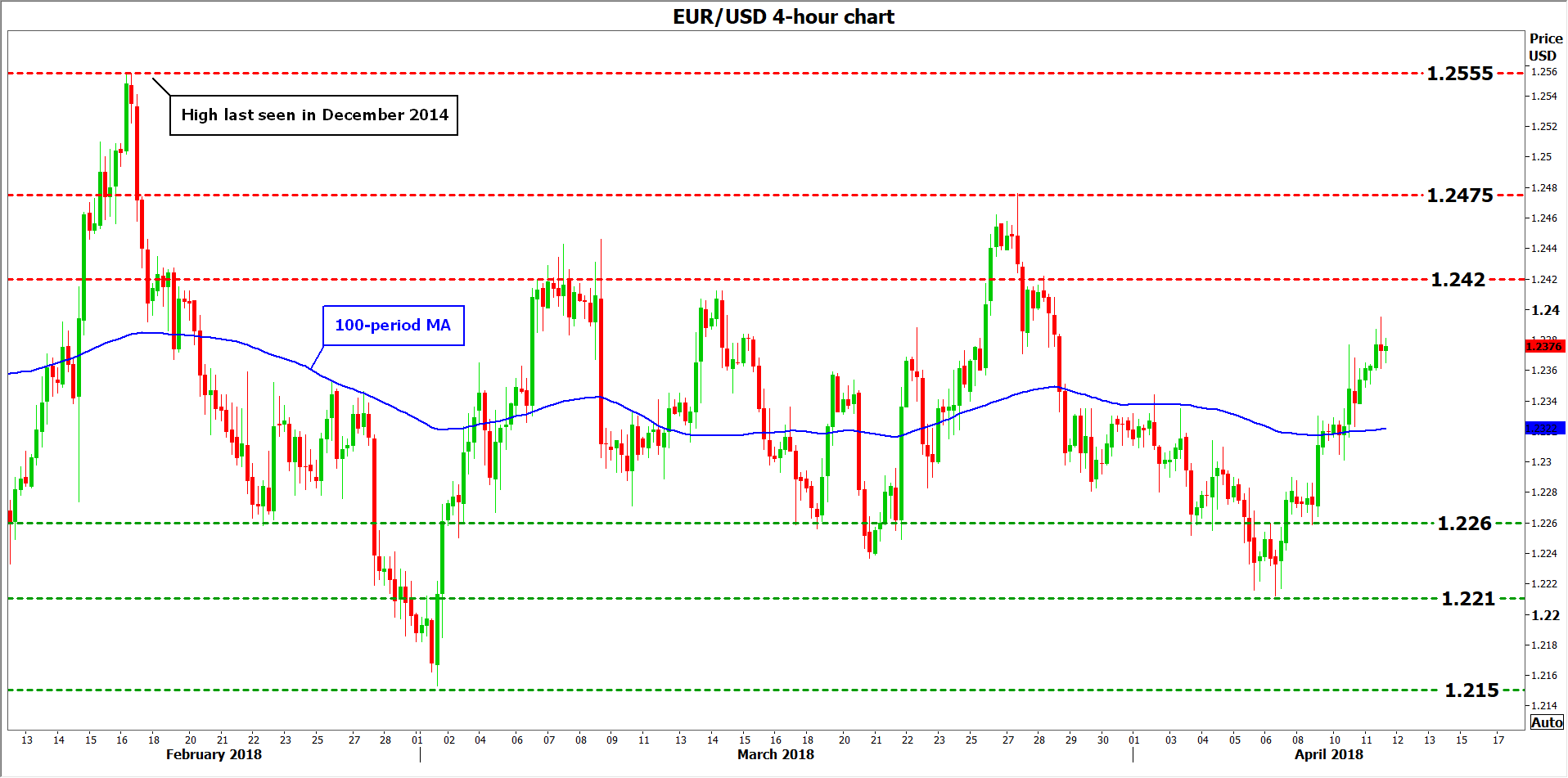

If the minutes reflect an increasing sense of optimism among officials, speculation that the Bank will begin tapering its asset purchases sooner rather than later could bring the euro under renewed buying interest. Euro/dollar could edge up and challenge the 1.2420 zone, marked by the highs of March 28, with an upside break bringing into focus the March 27 top at 1.2475. Even further advances could open the way for the pair’s three-year highs, at 1.2555.

On the flipside, if minutes paint a picture of a cautious ECB, the euro could edge lower. In this case, euro/dollar could encounter some support near the 100-period moving average on the 4-hour chart, at 1.2322. Steeper declines could initially target the 1.2260 line, defined by the lows of April 9, and subsequently the 1.2210 hurdle, marked by the trough of April 6. Even lower, support may be found at the low of March 1, at 1.2150.