{kind=link}

Here are the latest developments in global markets:

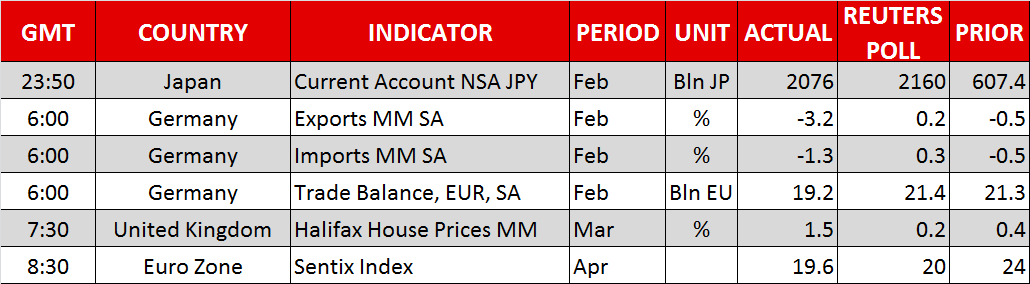

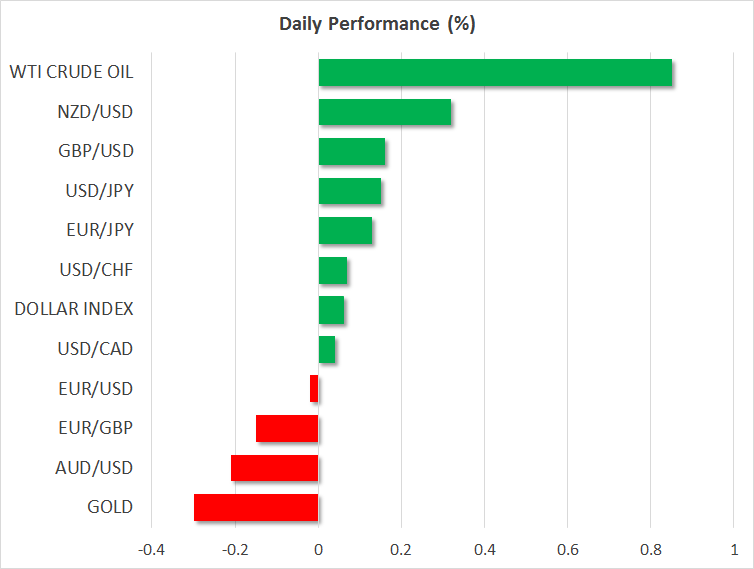

FOREX: Trade tensions continued to dominate the market theme as the US open approached. A tweet by President Trump on Sunday about the trade dispute with China went some way in lifting risk appetite in Asian trading on Monday. However, a report by Bloomberg that China is considering a gradual depreciation of the yuan knocked back the Australian dollar in European trading, as well as the Chinese currency. The aussie was hit hard, as Australian exports to China could suffer significantly from a weaker yuan, and slid to a one-week low of $0.7649. The yuan meanwhile tumbled to a 2-week low of 6.3168 per dollar from around 6.2950 in onshore trading. The euro also lost some ground, slipping to $1.2267 after the Eurozone sentix index decline sharply in April, missing expectations. Sterling was flat around $1.41, showing little reaction to a surprise monthly jump in UK house prices in March, according to figures from Halifax. The US dollar remained unfazed however by the China devaluation story, as the greenback extended its overnight gains. Dollar/yen was last trading higher 0.2% at 107.14 and the dollar index was up a similar amount to 90.24.

STOCKS: European stocks gave back some of their earlier advances as the risk of another currency devaluation by China hurt sentiment for risk assets. However, major indices in the region remained in positive territory, with the Euro Stoxx 50 index last trading 0.5% higher. UK shares were the exception though as the FTSE 100 was flat on the day. In the US, expectations of strong corporate earnings results for the first quarter, as well as some easing of trade tensions since Friday led the e-mini futures for the Dow Jones, S&P500 and the Nasdaq Composite between 0.7% and 1% higher.

COMMODITIES: Major commodities enjoyed a bounce on Monday along with equities. A heated war of words between the US and China on Friday had driven oil prices to closer lower by 2%. Another rise in the Baker Hughes oil rig count in the US last week also weighed on the commodity. But prices turned higher today, with WTI oil holding on to 0.2% gains at $62.21 a barrel, and Brent crude up 0.5% at $67.41 ahead of the US open. Gold retreated however, finding little safe-haven support from reports that Israel had allegedly carried out missile strikes on a Syrian airbase. The US had earlier been suspected of carrying out the strikes, which was denied by the Pentagon. The yellow metal was last down 0.4% at $1328 an ounce.

Day Ahead: Quiet start but Xi speech, US inflation and earnings season coming up later this week

While there seemed to be no let-up in the trade stand-off between the US and China, many investors remained hopeful that a full-blown trade war can still be averted and chose instead to focus on the week’s upcoming risk events. The first of which comes on Tuesday when President Xi of China makes a keynote address at the Boao Forum for Asia. The speech could be significant if President Xi uses the event to deescalate the trade dispute between the two nations. The Chinese leader will likely announce economic reforms and offer the US more market access, appeasing the US side. But if the proposals don’t go far enough, the US may continue to play hardball.

On Wednesday, all eyes will be on the US CPI figures for March, and on Friday, US corporate giants, including JP Morgan, Well Fargo and Citigroup will report their latest quarterly earnings.

Ahead of all that though, speeches by European Central Bank policymakers will be eyed. ECB Vice President Vitor Constancio will present the Bank’s annual report at the European Parliament at 13:00 CET, while Governing Council member Peter Praet will participate in the European Finance Forum in Germany at 16:45 GMT.

The euro has come under negative pressure recently following disappointing business confidence gauges for the Eurozone. A deep slowdown could hamper the ECB’s efforts to pull the plug on its stimulus program. Investors will therefore be paying special attention to policymakers’ views on the economic outlook. Hawkish comments could spur the euro above immediate resistance at $1.2290 handle, but any signs of a more cautious tone could push the single currency below $1.22.