{kind=link}

Commodity prices enjoyed quite the run up in the latter part of 2017 and early-2018, with most gaining significant ground underpinned by an uptick in global economic growth and depreciation in the U.S. dollar. And after bouncing back from February’s sharp sell-off alongside equity markets, commodity prices took another hit in March after the Trump Administration announced tariffs on steel and aluminum imports. While a number of countries have obtained an exemption from these tariffs – at least temporarily – ongoing protectionist rhetoric from the White House and retaliatory measures taken against the U.S. continue to generate uncertainty in global markets and risk-off sentiment.

Going forward, commodity prices will continue to be vulnerable to developments on the trade front and associated market reaction. Aside from sentiment, supply side factors will be key in determining the direction of prices. In general, commodity prices are expected to be flat with some upside risk. So long as the recently announced tariffs don’t have a significant impact on global economic growth, base metals prices have the most upside potential given tight markets. Meanwhile, oil and agriculture markets still have abundant supplies that will keep a lid on prices.

Oil Prices anchored at $60 per barrel

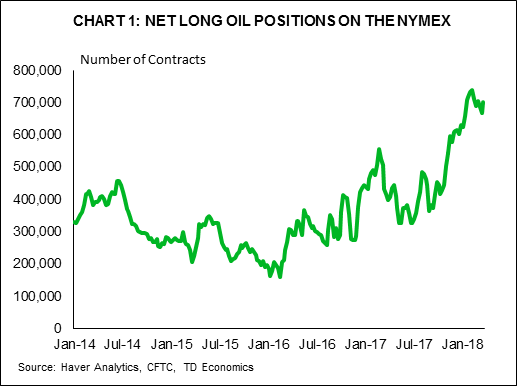

An uptick in global demand, continued supply restraint by OPEC and select non-OPEC countries, a falling U.S. dollar and geopolitical tensions in the Middle East have allowed crude oil prices to sit above the US$60 per barrel mark since the start of the year. But, looking ahead, the risks are tilted to the downside. While forecasts for global growth and oil demand have risen, supply is expected to keep up with or possibly outpace demand.

In addition to new capacity coming online in Canada, Brazil and the North Sea, U.S. output is forecast to increase by over a million barrels per day this year, reaching a record high and surpassing Russia to be the world’s top producer. Any disappointment in demand or even higher output could prolong the rebalancing process and put prices under pressure. Moreover, with speculative activity sitting at record levels this year, a change in sentiment could send prices tumbling. All told, prices should remain anchored close to US$60 per barrel through 2019.

Natural Gas Prices Fizzle

Natural gas prices kicked off the year on a roller coaster ride, rising and falling sharply in response to blasts of cold weather in key consuming regions in North America. Increased consumption has driven inventories to the low side of the 5-year range, but supplies are adequate nonetheless. Going forward, production in the U.S. is set to rise to a new record this year, and continue growing in 2019. Hence, while colder than normal temperatures could lead to additional bouts of price pressures, natural gas prices should remain contained at just over US$3.00 per MMBtu this year and next.

Base Metals Prices to Firm

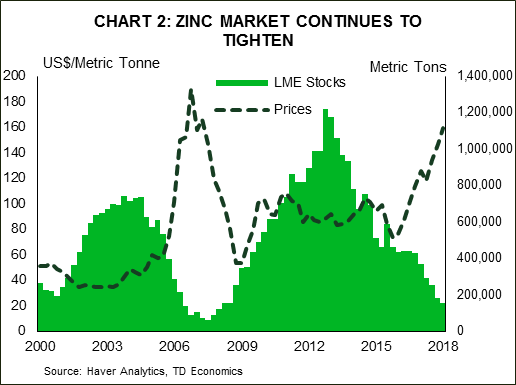

After coming into the year on an upswing, base metals prices have since been hit by the steel and aluminum tariffs announced by the U.S. government, on expectations that less American imports of the metals would increase global supply and lower non-US prices. With many countries gaining exemptions – at least until the end of April – the impact is likely to be smaller than originally anticipated. Aside from the tariffs, the outlook for base metals remains bright. Demand is expected to remain strong, while the lack of investment in new projects in recent years will push most base metals markets into deficit this year. Zinc is the tightest market, with the most upside potential for prices, although all base metals are poised to record annual gains. In 2019, zinc and copper prices are expected to continue rising, while aluminum and nickel pull back in line with higher production. Clearly aluminum prices face the most risk given that the tariff situation is fluid. However, should a trade war break out or global growth lose some steam, demand for other base metals would also falter, taking prices of these metals down as well.

Gold benefiting from trade uncertainty

Precious metals prices have benefited from the softer U.S. dollar this year, but also geopolitical tensions and a loss of risk appetite sparked by U.S. protectionist rhetoric. Going forward, there will be push and pull factors influencing gold prices. Further depreciation in the greenback, rising potential for higher inflation and ongoing geopolitical risks should bode well for prices, while rising interest rates will provide some offset. As such, we expect gold prices to remain fairly rangebound over the forecast horizon, hovering between US$1300 and US$1400/oz. Silver should outperform, helped along by strong physical demand stemming from a healthy pace of economic growth globally.

Lumber prices to remain elevated

Following a 19% jump in 2017, lumber prices have kicked off the year with a bang, reaching a new record high of over US$500 per thousand board feet. The strength has stemmed from wildfire induced supply constraints on the West coast of Canada and the U.S., increased demand following the hurricanes and tariffs imposed by the U.S. government on Canadian imports. As production normalizes and supply improves, prices should lose some steam. However, strong demand in the U.S. and tariffs on Canadian lumber will keep a floor under prices. All told, we expect prices to hover in the US$450-500 per thousand BdFt range over the forecast horizon.

Agricultural prices to hold

Agricultural prices have held up well in recent weeks, with both crop and livestock prices up slightly so far this year. Barring any weather disruptions, prices are likely hold around current levels going forward. Abundant supplies will keep a lid on crop prices, although barley prices have the most upside, given that its market is tightest. For livestock, demand is expected to be robust, but supplies are also set to grow this year, putting a cap on how high prices can move. As such, agriculture prices are largely expected to move sideways throughout this year and next.