{kind=link}

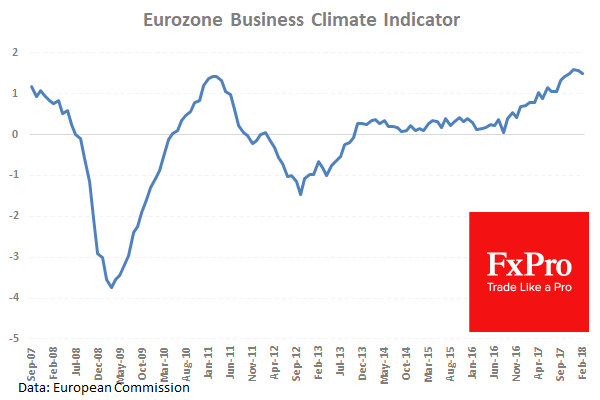

At 10:00 GMT, Business Climate (Mar), released by the European Commission, is based on monthly surveys and is designed to deliver a clear and timely assessment of the cyclical situation within the euro area. It may be interpreted as a survey result: a high reading indicates that, overall, the surveys point to a healthy cyclical situation. Conversely, a low reading points to an adverse business climate. A rise in the indicator will point to an upswing in activity and an improvement in the business climate. Alternatively, a fall will point to a deterioration in the business climate. Its movement is clearly linked to the industrial production of the euro area and, as such, it significantly impacts volatility in European Equities and also EUR FX crosses. Market consensus for today’s figure is for a reading of 1.40, from 1.48 previously.

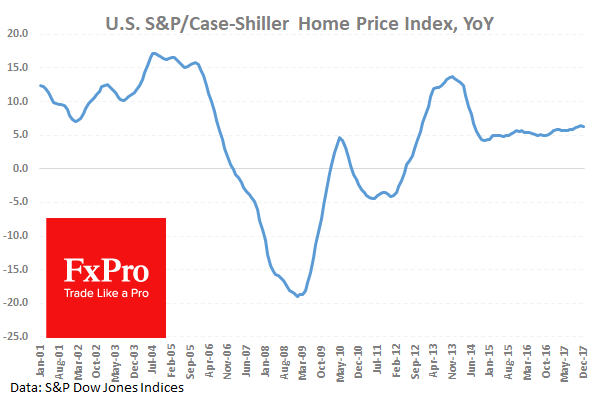

At 14:00 GMT, S&P/Case-Shiller Home Price Indices (YoY) (Jan), released by Standard & Poor, examines changes in the value of the residential real estate market in 20 regions across the US. This report serves as an indicator for the health of the US housing market. Generally speaking, a high reading is seen as positive or bullish for the USD, while a low reading is seen as negative, or bearish. Market expectations for today’s YoY figure for January is for a reading of 6.2%, from a previous value of 6.3%. Significant divergence from the expected number could likely increase volatility in US Dollar FX Crosses and possibly impact US Equities as well.

At 21:30 GMT, API Weekly Crude Oil Stocks are due to be released. API’s Weekly Statistical Bulletin (WSB) reports total U.S. and regional data relating to refinery operations and the production of the four major petroleum products: motor gasoline, kerosene jet fuel, distillate and residual fuel oil. These products represent more than 85% of the total petroleum industry. Published numbers normally impact volatility in WTI Crude futures and are closely watched by energy commodities traders. If the published number varies significantly from the expectations and forecasts then traders use it as a forecasting mechanism for the EIA Crude Oil weekly inventories report, which normally gets published a day later. Previously published API Stocks showed a drawdown of -2.739M barrels, which supported a bullish reaction in WTI Crude futures.